You estimate the following model. Dependent Variable: DRATE Method: ARMA Conditional Least Squares (Gauss-Newton / Marquardt steps) Date: 02/24/20 Time: 20:21 Sample (adjusted): 1962M02 2019M07 Included observations: 690 after adjustments Failure to Improve likelihood (non-zero gradients) after 11 iterations Coefficient covariance computed using outer product of gradients MA Backcast: 1962M01 Variable C MA(1) R-squared Adjusted R-squared S.E. of regression Sum squared resid Log likelihood F-statistic Prob(F-statistic) Inverted MA Roots O-0.002872 O-0.002933 O.0.439867 Coefficient Std. Error O 0.261752 -0.002872 0.439867 0.133801 0.132542 0.261752 47.13757 -53.21823 106.2748 0.000000 -44 t-Statistic 0.014344 -0.200229 0.034251 12.84247 Mean dependent var S.D. dependent var Akaike Info criterion Schwarz criterion Hannan-Quinn criter. Durbin-Watson stat Prob. 0.8414 0.0000 The unconditional mean of the above process (from Eviews output above) is -0.002933 0.281038 0.160053 0.173203 0.165139 2.088358

You estimate the following model. Dependent Variable: DRATE Method: ARMA Conditional Least Squares (Gauss-Newton / Marquardt steps) Date: 02/24/20 Time: 20:21 Sample (adjusted): 1962M02 2019M07 Included observations: 690 after adjustments Failure to Improve likelihood (non-zero gradients) after 11 iterations Coefficient covariance computed using outer product of gradients MA Backcast: 1962M01 Variable C MA(1) R-squared Adjusted R-squared S.E. of regression Sum squared resid Log likelihood F-statistic Prob(F-statistic) Inverted MA Roots O-0.002872 O-0.002933 O.0.439867 Coefficient Std. Error O 0.261752 -0.002872 0.439867 0.133801 0.132542 0.261752 47.13757 -53.21823 106.2748 0.000000 -44 t-Statistic 0.014344 -0.200229 0.034251 12.84247 Mean dependent var S.D. dependent var Akaike Info criterion Schwarz criterion Hannan-Quinn criter. Durbin-Watson stat Prob. 0.8414 0.0000 The unconditional mean of the above process (from Eviews output above) is -0.002933 0.281038 0.160053 0.173203 0.165139 2.088358

College Algebra

7th Edition

ISBN:9781305115545

Author:James Stewart, Lothar Redlin, Saleem Watson

Publisher:James Stewart, Lothar Redlin, Saleem Watson

Chapter1: Equations And Graphs

Section: Chapter Questions

Problem 10T: Olympic Pole Vault The graph in Figure 7 indicates that in recent years the winning Olympic men’s...

Related questions

Question

Kk5.

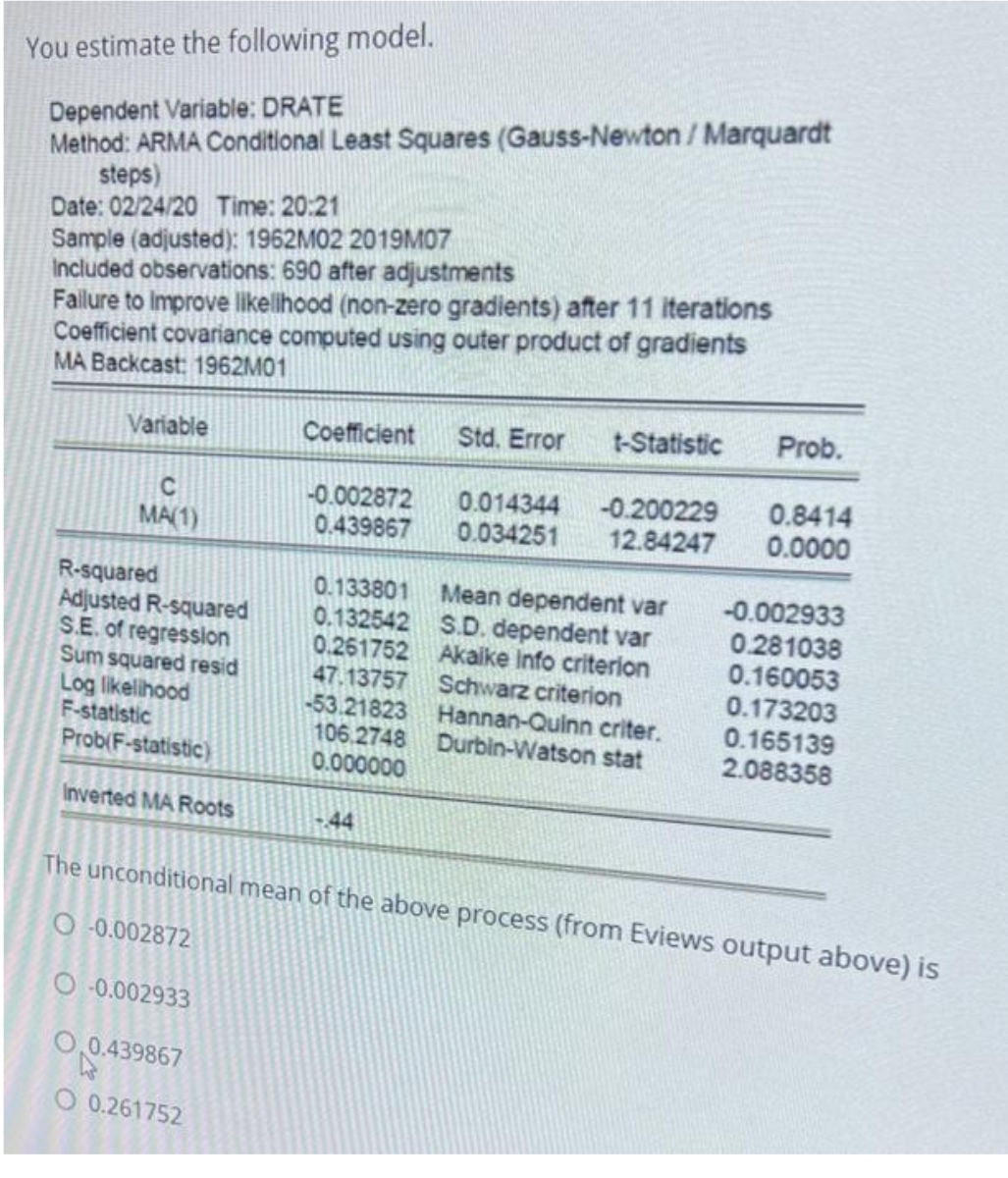

Transcribed Image Text:You estimate the following model.

Dependent Variable: DRATE

Method: ARMA Conditional Least Squares (Gauss-Newton / Marquardt

steps)

Date: 02/24/20 Time: 20:21

Sample (adjusted): 1962M02 2019M07

Included observations: 690 after adjustments

Failure to Improve likelihood (non-zero gradients) after 11 iterations

Coefficient covariance computed using outer product of gradients

MA Backcast: 1962M01

Variable

C

MA(1)

R-squared

Adjusted R-squared

S.E. of regression

Sum squared resid

Log likelihood

F-statistic

Prob(F-statistic)

Inverted MA Roots

O-0.002872

O-0.002933

O.0.439867

Coefficient Std. Error t-Statistic

O 0.261752

-0.002872

0.439867

0.133801

0.132542

0.261752

47.13757

-53.21823

106.2748

0.000000

-44

0.014344

-0.200229

0.034251 12.84247

Mean dependent var

S.D. dependent var

Akaike Info criterion

Schwarz criterion

Hannan-Quinn criter.

Durbin-Watson stat

Prob.

0.8414

0.0000

The unconditional mean of the above process (from Eviews output above) is

-0.002933

0.281038

0.160053

0.173203

0.165139

2.088358

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Recommended textbooks for you

College Algebra

Algebra

ISBN:

9781305115545

Author:

James Stewart, Lothar Redlin, Saleem Watson

Publisher:

Cengage Learning

Linear Algebra: A Modern Introduction

Algebra

ISBN:

9781285463247

Author:

David Poole

Publisher:

Cengage Learning

College Algebra

Algebra

ISBN:

9781305115545

Author:

James Stewart, Lothar Redlin, Saleem Watson

Publisher:

Cengage Learning

Linear Algebra: A Modern Introduction

Algebra

ISBN:

9781285463247

Author:

David Poole

Publisher:

Cengage Learning