You have run two regressions of ADIDAS "AD" returns. In the first, you regressed ADIDAS monthly returns against returns on the DAX – both in DM terms: Ret "AD" = 0.04% + 1.7 (Returns dax ) R2 = 58% %3D You also regressed the returns on ADIDAS against the Morgan Stanley Capital Index "ms"that includes global equities – both returns are dollar returns: Ret "ad" = -0.02% + 0.9 (Returns "ms") R2 = 14% Assume that the seven of the top ten investors in ADIDAS are international mutual funds. (The German long term bond rate is 0.05 , the US long term bond rate is 0.062 and the equity risk premium in both markets is 6% Estimate ADIDAS cost of equity in DM terms

You have run two regressions of ADIDAS "AD" returns. In the first, you regressed ADIDAS monthly returns against returns on the DAX – both in DM terms: Ret "AD" = 0.04% + 1.7 (Returns dax ) R2 = 58% %3D You also regressed the returns on ADIDAS against the Morgan Stanley Capital Index "ms"that includes global equities – both returns are dollar returns: Ret "ad" = -0.02% + 0.9 (Returns "ms") R2 = 14% Assume that the seven of the top ten investors in ADIDAS are international mutual funds. (The German long term bond rate is 0.05 , the US long term bond rate is 0.062 and the equity risk premium in both markets is 6% Estimate ADIDAS cost of equity in DM terms

Chapter13: Direct Foreign Investment

Section: Chapter Questions

Problem 1IEE

Related questions

Question

i need the answer quickly

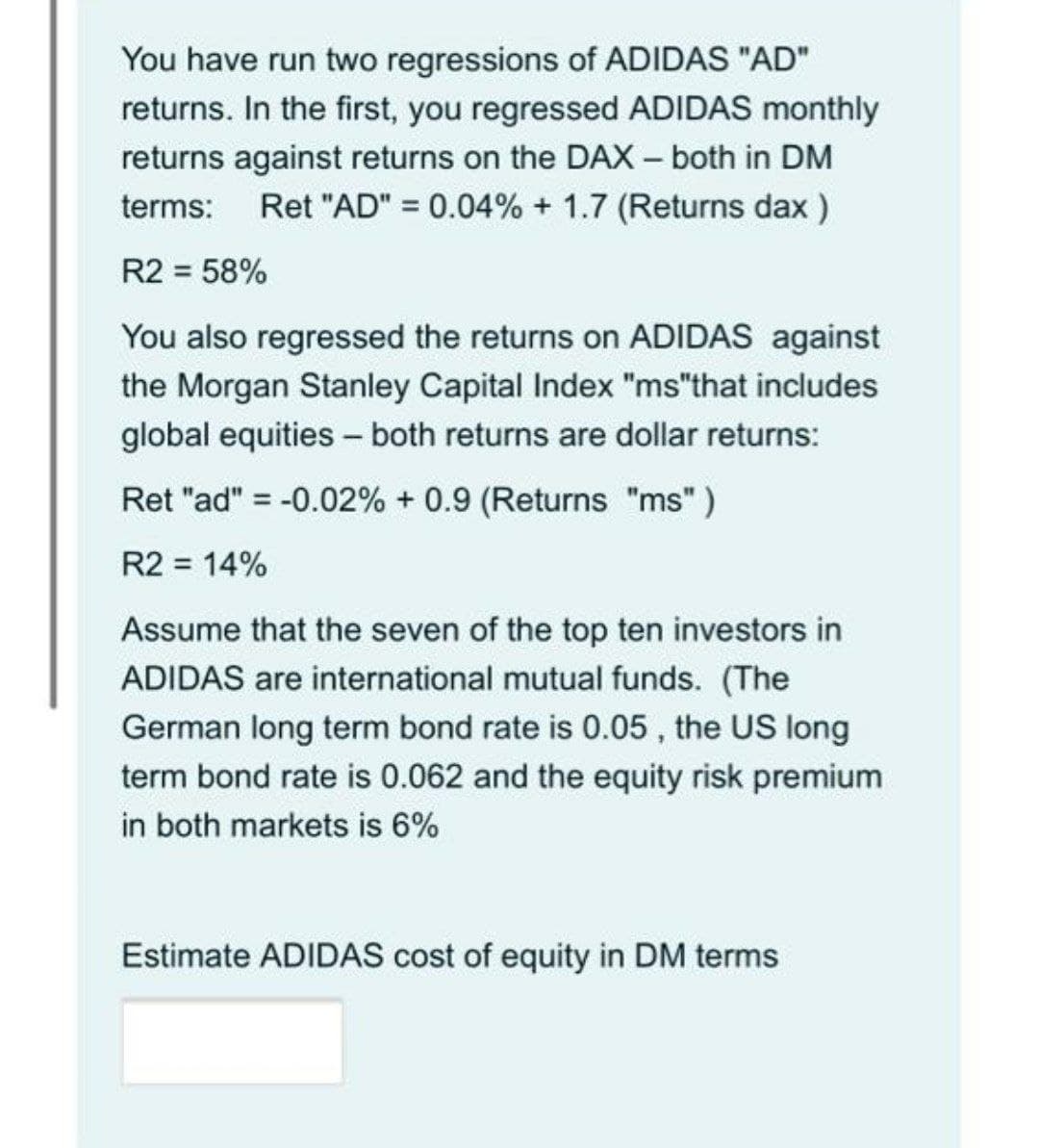

Transcribed Image Text:You have run two regressions of ADIDAS "AD"

returns. In the first, you regressed ADIDAS monthly

returns against returns on the DAX – both in DM

terms: Ret "AD" = 0.04% + 1.7 (Returns dax )

R2 = 58%

You also regressed the returns on ADIDAS against

the Morgan Stanley Capital Index "ms"that includes

global equities - both returns are dollar returns:

Ret "ad" = -0.02% + 0.9 (Returns "ms" )

R2 = 14%

Assume that the seven of the top ten investors in

ADIDAS are international mutual funds. (The

German long term bond rate is 0.05 , the US long

term bond rate is 0.062 and the equity risk premium

in both markets is 6%

Estimate ADIDAS cost of equity in DM terms

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you