The beginning inventory at Midnight Supplies and data on purchases and sales for a three month period ending March 31 are as follows. Complete the instructions. Instructions 1. Record the inventory, purchases, and cost of goods sold data in a perpetual inventory record similar to the one illustrated in Exhibit 3, using the first-in, first-out method. 2. Determine the total sales and the total cost of goods sold for the period. Journalize the entries in the sales and cost of goods sold accounts. Assume that all sales were on account and date your journal entry March 31. Refer to the Chart of Accounts for exact wording of account titles. 3. Determine the gross profit from sales for the period.

The beginning inventory at Midnight Supplies and data on purchases and sales for a three month period ending March 31 are as follows. Complete the instructions. Instructions 1. Record the inventory, purchases, and cost of goods sold data in a perpetual inventory record similar to the one illustrated in Exhibit 3, using the first-in, first-out method. 2. Determine the total sales and the total cost of goods sold for the period. Journalize the entries in the sales and cost of goods sold accounts. Assume that all sales were on account and date your journal entry March 31. Refer to the Chart of Accounts for exact wording of account titles. 3. Determine the gross profit from sales for the period.

Financial And Managerial Accounting

15th Edition

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:WARREN, Carl S.

Chapter6: Inventories

Section: Chapter Questions

Problem 1PB: FIFO perpetual inventory The beginning inventory at Dunne Co. and data on purchases and sales for a...

Related questions

Topic Video

Question

The beginning inventory at Midnight Supplies and data on purchases and sales for a three month period ending March 31 are as follows. Complete the instructions.

| Instructions | |

| 1. | Record the inventory, purchases, and cost of goods sold data in a perpetual inventory record similar to the one illustrated in Exhibit 3, using the first-in, first-out method. |

| 2. | Determine the total sales and the total cost of goods sold for the period. Journalize the entries in the sales and cost of goods sold accounts. Assume that all sales were on account and date your |

| 3. | Determine the gross profit from sales for the period. |

| 4. | Determine the ending inventory cost as of March 31. |

| 5. | Based upon the preceding data, would you expect the ending inventory using the last-in, first-out method to be higher or lower? |

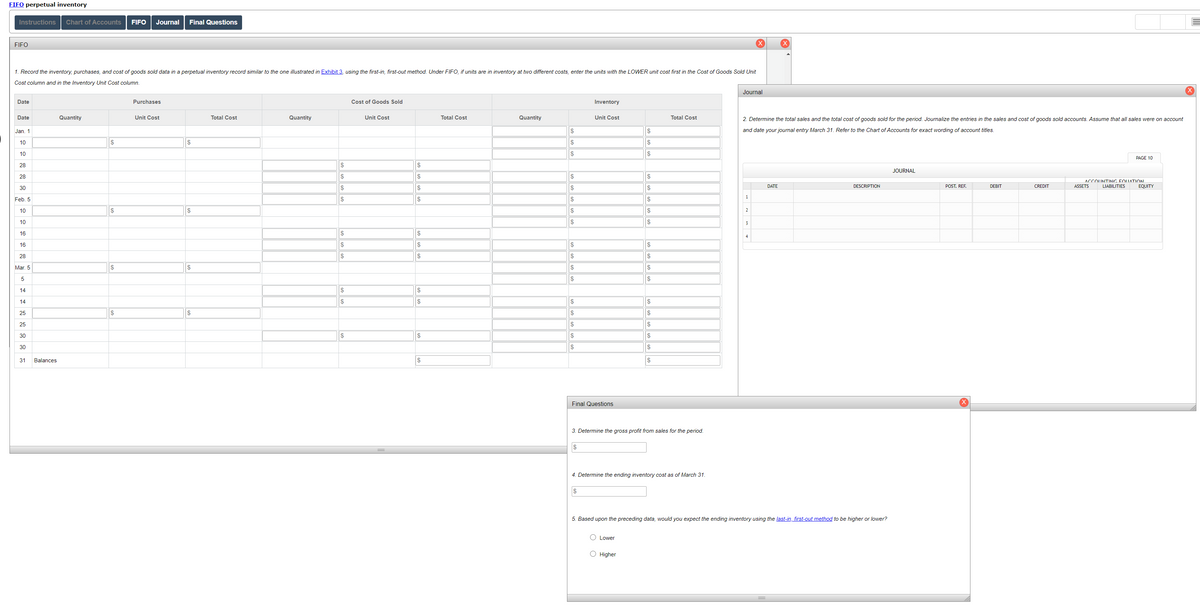

Transcribed Image Text:FIFO perpetual inventory

Instructions

Chart of Accounts

FIFO

Journal

Final Questions

FIFO

1. Record the inventory, purchases, and cost of goods sold data in a perpetual inventory record similar to the one illustrated in Exhibit 3, using the first-in, first-out method. Under FIFO, if units are in inventory at two different costs, enter the units with the LOWER unit cost first in the Cost of Goods Sold Unit

Cost column and in the Inventory Unit Cost column.

Journal

Date

Purchases

Cost of Goods Sold

Inventory

Date

Quantity

Unit Cost

Total Cost

Quantity

Unit Cost

Total Cost

Quantity

Unit Cost

Total Cost

2. Determine the total sales and the total cost of goods sold for the period. Journalize the entries in the sales and cost of goods sold accounts. Assume that all sales were on account

Jan. 1

$

$

and date your journal entry March 31. Refer to the Chart of Accounts for exact wording of account titles.

10

$

2$

$

$

10

$

$

PAGE 10

28

JOURNAL

28

$

$

$

ACCOUNTING FOUATION

30

$

$

$

$

DATE

DESCRIPTION

POST. REF.

DEBIT

CREDIT

ASSETS

LIABILITIES

EQUITY

1

Feb. 5

$

$

$

$

10

$

$

2

10

$

3

16

2$

4

16

$

2$

$

$

28

$

$

$

Mar. 5

2$

2$

$

$

$

$

14

$

2$

14

$

$

$

$

25

2$

2$

$

25

$

$

30

$

$

$

$

30

$

$

31

Balances

$

Final Questions

3. Determine the gross profit from sales for the period.

24

4. Determine the ending inventory cost as of March 31.

5. Based upon the preceding data, would you expect the ending inventory using the last-in, first-out method to be higher or lower?

O Lower

O Higher

%24

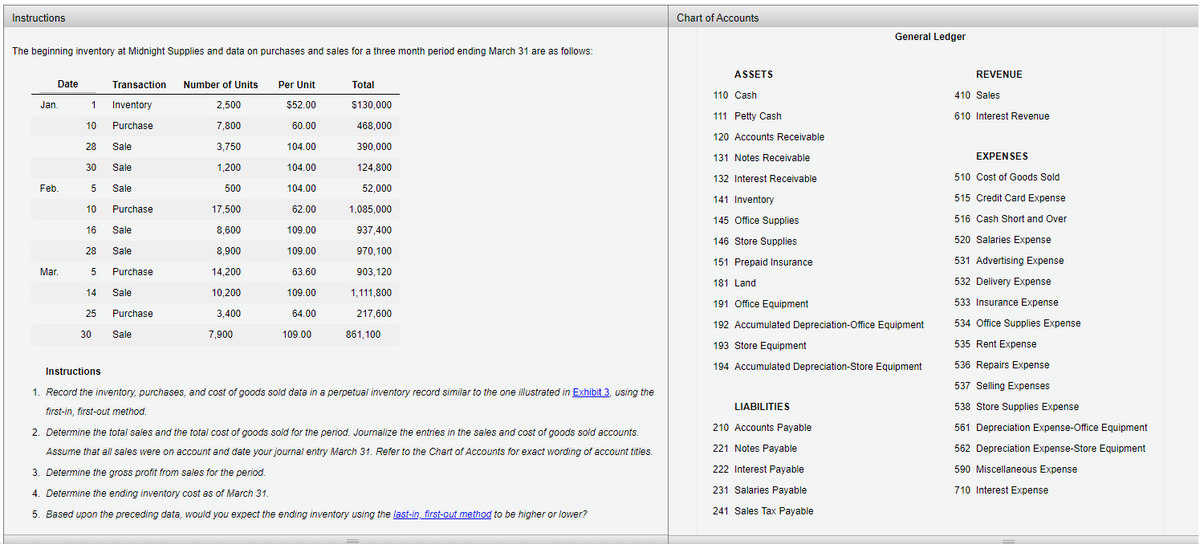

Transcribed Image Text:Instructions

Chart of Accounts

General Ledger

The beginning inventory at Midnight Supplies and data on purchases and sales for a three month period ending March 31 are as follows:

ASSETS

REVENUE

Date

Transaction Number of Units

Per Unit

Total

110 Cash

410 Sales

1 Inventory

$130,000

Jan.

2,500

$52.00

111 Petty Cash

610 Interest Revenue

10

Purchase

7,800

60.00

468,000

120 Accounts Receivable

28

Sale

3,750

104.00

390,000

131 Notes Receivable

EXPENSES

30

Sale

1,200

104.00

124,800

132 Interest Receivable

510 Cost of Goods Sold

Feb.

Sale

500

104.00

52,000

141 Inventory

515 Credit Card Expense

10

Purchase

17,500

62.00

1,085,000

145 Office Supplies

516 Cash Short and Over

16

Sale

8,600

109.00

937,400

146 Store Supplies

520 Salaries Expense

28

Sale

8,900

109.00

970,100

151 Prepaid Insurance

531 Advertising Expense

Mar.

5

Purchase

14,200

63.60

903,120

181 Land

532 Delivery Expense

14

Sale

10,200

109.00

1,111,800

191 Office Equipment

533 Insurance Expense

25

Purchase

3,400

64.00

217,600

192 Accumulated Depreciation-Office Equipment

534 Office Supplies Expense

30

Sale

7,900

109.00

861,100

193 Store Equipment

535 Rent Expense

194 Accumulated Depreciation-Store Equipment

536 Repairs Expense

Instructions

537 Selling Expenses

1. Record the inventory, purchases, and cost of goods sold data in a perpetual inventory record similar to the one illustrated in Exhibit 3, using the

LIABILITIES

538 Store Supplies Expense

first-in, first-out method.

2. Determine the total sales and the total cost of goods sold for the period. Journalize the entries in the sales and cost of goods sold accounts.

210 Accounts Payable

561 Depreciation Expense-Office Equipment

Assume that all sales were on account and date your journal entry March 31. Refer to the Chart of Accounts for exact wording of account titles.

221 Notes Payable

562 Depreciation Expense-Store Equipment

3. Determine the gross profit from sales for the period.

222 Interest Payable

590 Miscellaneous Expense

4. Determine the ending inventory cost as of March 31.

231 Salaries Payable

710 Interest Expense

5. Based upon the preceding data, would you expect the ending inventory using the last-in, first-out method to be higher or lower?

241 Sales Tax Payable

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781337272124

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,