. 3,690,000 B. 3,900,000 C. 2,805,000

Q: Question 45 On January 1, the assets were P500,000 and the liabilities were P200,000. During the…

A: Equity is the difference between assets and liabilities of the business.

Q: Grand Champion Inc. purchased America’s Sweethearts Corporation On January 1, 2019. At the time,…

A: The technique of integrating many business divisions of a company into a bigger organization is…

Q: A. 109,650 B. 108,000 C. 106,350 D. 110,000

A: Solution : Given Capital balances: Partner Capital Profit sharing ratio Larry…

Q: 2............ 3............. 4............. 5............ (b) autred 80,000 90,000 80,000 20,000…

A: A capital budget is a tool for evaluating two or more projects. The tool helps business owners…

Q: P 122,500 219,000 60,000 60,000 Accounts Payable Accounts Receivable Accumulated…

A: Formula: Net income = Total Revenues - Total expenses

Q: What is the impairment loss for the current year?

A: Impairment: Impairment is the sudden loss in the value of an asset other than depreciation for…

Q: 2:25 O 令l 30% The following accounts are extracted from the books of X Inc. on December 31, 202O:…

A: The answers for the multiple choice questions and relevant working are presented hereunder :

Q: I need help with this Accounting Question.

A: In order to capitalise the borrowing cost, the weighted average expenditure incurred on constitution…

Q: 20,000 20,000 20,000 360,000 200,000 360,000 8.6 Which of the following best explains what is meant…

A: 8.6 Capital Expenditures are the expenses incurred by an organization for acquiring, upgrading, and…

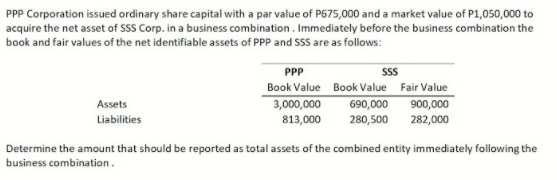

Q: How much is the consolidated total assets?

A: Consolidated total assets is defined as the net book value of all the assets of the company as well…

Q: A. P240,000 B. P560,000 C. P320,000 D. P400,000 E. Answer not Given

A: Break-even point: It can be defined as that level of production at which the company’s costs fall…

Q: 234,000 384,000 230,400 276,000

A: Step 1 Creditors management is the managing the creditors and accounts payables in an effective…

Q: Question 5 The following balances were extracted from the books of Billion Precision for the year…

A: Statement of comprehensive income is the statement showing the income calculated by deducting the…

Q: Year 1 4 CFx ($12,292) $8,123 $4,523 $3,523 $1,477 11.00% CFy ($12,292) $4,423 $2,477 $4,523 $5,523…

A: Calculations are given below -

Q: Investment Perlod 1 3 4 A $(1,000) $100 $100 $100 $100 $1,100 B (1,000) 264 264 264 264 264 (1,000)…

A: Rate of return= 5% Period= 5 years NPV = CF0 + CF1 ··· + CFt /(1+r)t Where CF= Cash Flow of various…

Q: 78,000 ₱75,000 ₱80,000 ₱77,000

A: The total cost of a product comprises of fixed cost and variable cost.

Q: PROVIDE COMPUTATION! 5. Cumulative compensation expense at the end of year 1 a. P407,000 c.…

A:

Q: Maintenance and Repairs Expense 48,000 Depreciation Expense Insurance Expense Salaries and Wages…

A: “Since you have asked multiple sub-parts, we will solve the first three sub-part for you. If you…

Q: 2,950 B. P55,300 C. P82,950

A: The question is based on the concept pf Financial Accounting.

Q: How much are the revenue and cost of construction recognized in 20x2? Revenue Cost of construction…

A: Solution Given Contract price =4000000 Total estimated cost =3000000 20X1 20X2…

Q: 3. Find the IRR on the following projects: A B. D -$1,000 $100 $300 $400 -$200 $120 $150 $150…

A: Hi There, Thanks for posting the questions. As per our Q&A guidelines, must be answered only one…

Q: PA3. 11.2 During the current year, Alanna Co. had the following transactions pertaining to its new…

A: note: “Since you have asked multiple question, we will solve the first question for you. If you want…

Q: Question 10 of 20: Select the best answer for the question The books of the Marvel Company showed…

A: Accounting equation has three important elements. These are assets, liabilities and equity. At the…

Q: O A. $69,000 O B. $80,000 O C. $65,000 $111.000

A: Always there would be priority that project with maximum NPV will be selected only and sum of all…

Q: 9. $177,400 $106,440 10. $2,330,000 11. $342,900 $264,033 Level 2 Chapter 18- Section II - Exercise…

A:

Q: Choose and explain. a. P4,170,000 b. P4,270,000

A: The question is based on the concept of Cost Acounting.

Q: 1,600 1,400 1,200 1,000 1 2 4 5 i-8% 3.

A: The present value of the cash flow is the current worth of a cash flow at a certain rate of interest…

Q: O b. 6,550,000

A: Option B) 655,000 USING THE FORMULA approach. These methods will be used to compute the gross sales.…

Q: teddy’s Pillow’s had beginning net fixed assets of $461 and ending net fixed assets of $530. Assets…

A: The net amount spent by a corporation to acquire fixed assets over a period of time is referred to…

Q: 9. P = P400, 000; A= P401, 000; r = 3.5% 10. P = P90,000; A= P95, 000; r = 4.5%

A: 9) Principal (P) = P 400000 Maturity value (A) = P 401000 r = 3.5% Let n = Years to reach to the…

Q: . 2,000,000 b. 1,000,000 c. No provision is to be recognized but a disclosure of Php2,000,000 is…

A: Provision refers to the account that would be recorded to present the liability of the entity and it…

Q: BE9.1 (LO 1) The following expenditures were incurred by Rosenberg Construction in purchasing land:…

A: Cost of the land = (Cash price + Accrued taxes + Attorney’s fees + Real estate broker’s commission +…

Q: Year 2 4 ($12,292) ($12,292) CFx $8,123 $4,523 $3,523 $1,477 11.00% CFy $4,423 $2,477 $4,523 $5,523…

A: Given:

Q: 1. What is the cost of the land? a. 4,550,000 b. 4,800,000 c. 4,850,000 d. 4,450,000 2. What is the…

A: Cost of Fixed Assets Fixed assets is recorded at cost of acquisition. All expenditures directly…

Q: Department 1 P486,000 27,000 4,200 3.

A: Overhead Applied: It is a direct overhead expense that gets recorded in cost accounting, it is a…

Q: Calculate Current Ratio Debtors Turnover Ratio Stock Turnover Ratio Return on Total Assets

A: Since you have asked multiple question, so we will solve the all 4 question for you.

Q: EIL.25 (LOS)) (Revaluation Accounting) Pengo Ltd. owns land that it purchased at a cost of V400…

A: Other Comprehensive Income= It includes only those incomes and expenses or losses which cannot be…

Q: The following account balances were included in Bromley Companγs balance sheet on December 31, 2018:…

A: A balance sheet displays the final amounts in a company's asset, liability, and equity accounts as…

Q: а. $150,000 b. $100,000 С. $125,000 d.

A: Manufacturing Overheads are the various indirect material, labour and other costs incurred during a…

Q: Problem 5-18 (AA) On June 1, 202O, Circus Company began construction o new manufacturing plant. The…

A: Here 6% interest rate on loan is per annum basis

Q: EA1. LO 11.1 Fombell, Incorporated has the following assets in its trial balance: $ 10,000 60,000…

A: As posted multiple independent questions we are answering only first question kindly repost the…

Q: ARR 6% fe (years) A B C D. itial Cost F, years 1-4 11,000 13,500 14,000 8400 4000 4500 4880 3000 W B…

A: In the cost benefit ratio we choose the project with high B/C ratio.

Q: Q 5. [A] From the following data, indicate the effect that the changes in the relevant items will…

A: Working capital: It is a financial standard which act for operating liquidity available to an…

Q: PROBLEMS Problem 23-1 (IAA) Simple Company reported the following information in relation to land:…

A: Note: Since you have posted a question with multiple sub-parts, we will solve the first three…

Q: Investment Perlod 1 3 4 A $(1,000) $100 $100 $100 $100 $1,100 B (1,000) 264 264 264 264 264 C…

A: IRR is an estimation of required rate of return that is compounded on a project or investment to…

Q: Instructions Dec. 31, 20Y3 Dec. 31, 20Y2 Assets 3 Cash $155,000.00 $150,000.00 4 Accounts receivable…

A:

Q: Project A Project B Project C Project D 2.000 YEARS Investment Amount(PB) 1.000 1.000 2.000 1 250…

A: The company is considering the value for different projects and these are evaluated on the basis of…

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

- On January 1, 20x1, John Corp. acquired the identifiable net assets of Jose Corp. by paying cash of ₱1,500,000 and issuing 10,000 ordinary shares with par and fair value of ₱100 and ₱120 per share, respectively. The identifiable assets of Jose had book values of ₱3,200,000 and fair values of ₱4,000,000 and its liabilities have book values equal to its fair values amounting to ₱1,500,000. As per agreement, John Corp. agreed to pay additional amount equal to 20% of the 20x1 year-end profit that exceeds ₱500,000 on January 2, 20x2. On the date of acquisition Jon estimated that the fair value of contingent consideration is ₱15,000. Assume the actual profit of ABC on December 31, 20x1 is ₱600,000. What is the gain (loss) on extinguishment of contingent consideration liability.DDD Company issued its ordinary shares for the net assets of EEE Company in a business combination treated as acquisition. DDD’s ordinary share issued was worth P1,000,000. At the date of combination, DDD’s net assets had a book value of P1,200,000 and a fair value of P1,600,000. EEE’s net assets had a book value of P650,000 and a fair value of P800,000. Immediately following the combination, the net assets of the combined company should have been reported at what amount?On January 1, 20X1, P Company (PC) purchased 80% of the outstanding shares of S Company (SC) at thecost of P700,000. On that date, SC had P300,000 and P500,000 capital stock and retained earnings,respectively. The non-controlling interest (NCI) is measured on a fair-value basis.For 20X1, PC had a comprehensive income (CI) of P300,000 and paid dividends of P100,000. On the otherhand, SC reported a CI of P150,000 and paid dividends of P50,000. All of the assets and liabilities of SCompany had book values that approximately equal to their respective market values.On December 31, 20X1, PC sold a piece of equipment with a book value of P30,000 to SC for P25,000.The gain on the sale is included in the CI of PC indicated above. The equipment has a 10-year useful life.It has been used for the past five (5) years before the date of acquisition. Required:a. Prepare the journal entries that both companies should make for the year 20X1.b. Allocate the consolidated comprehensive income at the end…

- On June 1, 2020, SME A acquired 35% of the equity of entities X, Y, Z for P64,000 and P58,000 and P37,000, respectively, SME A has joint control over the strategic financial and operating decisions of entities X, Y and Z. Transaction costs of 5% of the purchase price of the shares were incurred by SME A. On December 31, 2020, Entity X declared dividends of P9,000 and Entity Y, P15,000 for the year 2020. These dividends are to be paid by X and Y in 2021. Entity Z declared and paid a dividend of P24,000 for the year ended 2020. For the year ended December, 31, 2020, entities X and Y recognized loss of P30,000 and P42,000. respectively. However, entity Z recognized a profit of P18,000 for that year. Published price quotations do not exist for the shares of X, Y and Z. Using appropriate valuation techniques, SME A determined the fair values of their investments in entities X, Y and Z at December 31, 2020 as P60,000, P65,000, and P49,000, respectively. Costs to sell are estimated at 9% of…XYZ Company merged into UUU Company on July 1, 2021. In exchange for the net assets at fair market value of XYZ Company amounting to P696,450, UUU, issued 68,000 ordinary shares at P9 par value with a market price of P12 per share. Out-of-pockets of the combination were as follows: Legal fees for the contract of business combination P35,600; Audit fee for SEC registration of stock issue P90,000; Printing costs of stock certificates P14,500; Broker’s fee P23,600; Accountant’s fee for pre-acquisition P80,000; Other indirect cost of acquisition P75,000; General and allocated expenses P43,000 and Listing fees in issuing new shares P36,000. XYZ will pay an additional cash consideration of P455,000 in the event that UUU’s net income will be equal or greater than P950,000 for the period ended December 31, 2021. At acquisition date, there is a high probability of reaching the target net income and the fair value of the additional consideration was determined to be P195,000. Actual net income…XYZ Company merged into UUU Company on July 1, 2021. In exchange for the net assets at fair market value of XYZ Company amounting to P696,450, UUU, issued 68,000 ordinary shares at P9 par value with a market price of P12 per share. Out-of-pockets of the combination were as follows: Legal fees for the contract of business combination P35,600; Audit fee for SEC registration of stock issue P90,000; Printing costs of stock certificates P14,500; Broker’s fee P23,600; Accountant’s fee for pre-acquisition P80,000; Other indirect cost of acquisition P75,000; General and allocated expenses P43,000 and Listing fees in issuing new shares P36,000. XYZ will pay an additional cash consideration of P455,000 in the event that UUU’s net income will be equal or greater than P950,000 for the period ended December 31, 2021. At acquisition date, there is a high probability of reaching the target net income and the fair value of the additional consideration was determined to be P195,000. Actual net income…

- Gera Corporation owns two financial investments in the shares of listed companies. Details of which are as follows: Investment 1 – Acquired on September 1, 2020, at a cost of P50,000 with a Fair value of P60,000 at year-end for the purpose of trading. Investment 2 - Acquired on August 1, 2020, at a cost of P25,000 to hold indefinitely. Its fair value at year-end is P20,000. What are the amounts to appear in the Statement of Comprehensive Income for the year ended September 30, 2020?The Elf Co. acquired a 60% interest in the Pea Co. when Pea's equity comprised share capital of P100,000 and retained earnings of P150,000. Pea's current statement of financial position shows share capital of P100,000, a revaluation reserve of P75,000 and retained earnings of P300,000. Under IAS 27, Consolidated and Separate Financial Statements, what amount in respect of the non-controlling interest should be included in Elf Co.'s consolidated statement of financial position?XYZ Company merged into UUU Company on July 1, 2021. In exchange for the netassets at fair market value of XYZ Company amounting to P696,450, UUU, issued68,000 ordinary shares at P9 par value with a market price of P12 per share. Outof-pockets of the combination were as follows: Legal fees for the contract ofbusiness combination P35,600; Audit fee for SEC registration of stock issueP90,000; Printing costs of stock certificates P14,500; Broker’s fee P23,600;Accountant’s fee for pre-acquisition P80,000; Other indirect cost of acquisitionP75,000; General and allocated expenses P43,000 and Listing fees in issuingnew shares P36,000. XYZ will pay an additional cash consideration of P455,000in the event that UUU’s net income will be equal or greater than P950,000 for theperiod ended December 31, 2021. At acquisition date, there is a high probabilityof reaching the target net income and the fair value of the additionalconsideration was determined to be P195,000. Actual net income for the…

- If PROMDI Co., a new company would acquire the net assets of CARDO Co and SYANO Co. PROMDI Co will be issuing 30,000 shares to CARDO and 12,000 shares to SYANO. The following is the balance sheet of PROMDI Co, followed by the fair values and additional unpaid costs incurred by PROMDI in the acquisition: REQUIREMENTS:A. GoodwillB. Consolidated Total Assets at the date of acquisitionC. Consolidated Total Liabilities at the date of acquisitionD. Consolidated Equity at the date of acquisitionDonut Inc. issued 20,000 common shares in exchange for all the outstanding shares of Munchkin Inc. On acquisition date, Munchkin Inc.’s net identifiable assets have carrying amount of P4,000,000 and fair value of P2,000,000. The transaction increased Donut Inc.’s share premium by P400,000; however, no goodwill resulted from the business combination. How much is the acquisition-date fair value per share of the common shares issued by Donut Inc.?* a. P 100 b. P 20 c. P 40 d. P 80XENON Company merged into URANIUM Company on July 1, 2021. In exchange for the net assets at fair market value of XENON Company amounting to P696,450, URANIUM, issued 68,000 ordinary shares at P9 par value with a market price of P12 per share. Out-of-pockets of the combination were as follows: Legal fees for the contract of business combination P35,600; Audit fee for SEC registration of stock issue P90,000; Printing costs of stock certificates P14,500; Broker’s fee P23,600; Accountant’s fee for pre-acquisition P80,000; Other indirect cost of acquisition P75,000; General and allocated expenses P43,000; Listing fees in issuing new shares P36,000. XENON will pay an additional cash consideration of P455,000 in the event that URANIUM’s net income will be equal or greater than P950,000 for the period ended December 31, 2021. At acquisition date, there is a high probability of reaching the target net income and the fair value of the additional consideration was determined to be P195,000.…