1. The estimation of a Cobb-Douglas production function for 20 firms of a given industry yields: 16.907 + 0.322k₁ + 2.777l R2 = 0.915 DW = 2.032 RSS=0.461 Use a = 5% Var = B 0.166070 0.031857 0.216639 -0.857446 -0.057229 4.939971/ where : fitted values of naturals logaritrhms of output (output express in 1000 tons); k: natural logaritrhms of capital output (output express in 1000 tons) l: natural logaritrhms of labour (labour is in hours) RSS: residual sum of squares t: firm index Var ß: variance - covariance matrix of estimates a. Evaluate the statistical significance of the coefficients.

1. The estimation of a Cobb-Douglas production function for 20 firms of a given industry yields: 16.907 + 0.322k₁ + 2.777l R2 = 0.915 DW = 2.032 RSS=0.461 Use a = 5% Var = B 0.166070 0.031857 0.216639 -0.857446 -0.057229 4.939971/ where : fitted values of naturals logaritrhms of output (output express in 1000 tons); k: natural logaritrhms of capital output (output express in 1000 tons) l: natural logaritrhms of labour (labour is in hours) RSS: residual sum of squares t: firm index Var ß: variance - covariance matrix of estimates a. Evaluate the statistical significance of the coefficients.

Managerial Economics: Applications, Strategies and Tactics (MindTap Course List)

14th Edition

ISBN:9781305506381

Author:James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Chapter9: Applications Of Cost Theory

Section: Chapter Questions

Problem 3E

Related questions

Question

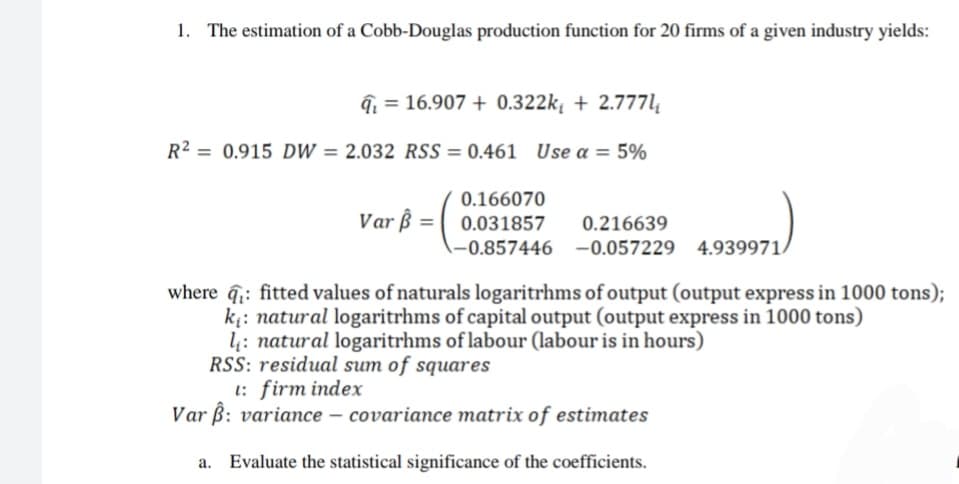

Transcribed Image Text:1. The estimation of a Cobb-Douglas production function for 20 firms of a given industry yields:

= 16.907 + 0.322k₁ + 2.777l₁

R² = 0.915 DW = 2.032 RSS=0.461 Use a = 5%

Var ß=

0.166070

0.031857 0.216639

-0.857446 -0.057229 4.939971/

where : fitted values of naturals logaritrhms of output (output express in 1000 tons);

k₁: natural logaritrhms of capital output (output express in 1000 tons)

l: natural logaritrhms of labour (labour is in hours)

RSS: residual sum of squares

t: firm index

Var ß: variance - covariance matrix of estimates

a. Evaluate the statistical significance of the coefficients.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Managerial Economics: Applications, Strategies an…

Economics

ISBN:

9781305506381

Author:

James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:

Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:

9781337106665

Author:

Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:

Cengage Learning

Managerial Economics: Applications, Strategies an…

Economics

ISBN:

9781305506381

Author:

James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:

Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:

9781337106665

Author:

Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:

Cengage Learning