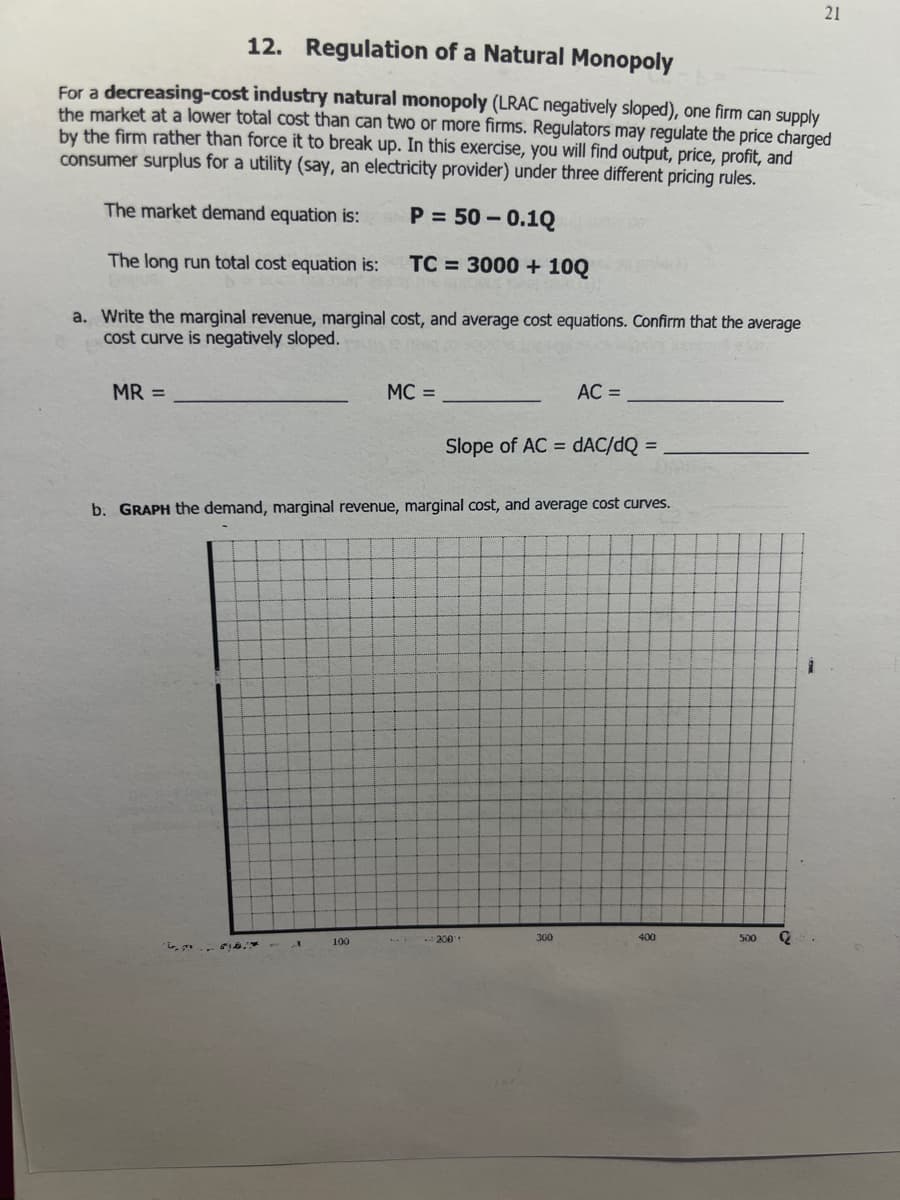

12. Regulation of a Natural Monopoly For a decreasing-cost industry natural monopoly (LRAC negatively sloped), one firm can supply the market at a lower total cost than can two or more firms. Regulators may regulate the price charged by the firm rather than force it to break up. In this exercise, you will find output, price, profit, and consumer surplus for a utility (say, an electricity provider) under three different pricing rules. The market demand equation is: P = 50 – 0.1Q The long run total cost equation is: TC = 3000 + 10Q a. Write the marginal revenue, marginal cost, and average cost equations. Confirm that the average cost curve is negatively sloped. MR = MC = AC = Slope of AC = dAC/dQ = b. GRAPH the demand, marginal revenue, marginal cost, and average cost curves. 100 200 300 400 500

12. Regulation of a Natural Monopoly For a decreasing-cost industry natural monopoly (LRAC negatively sloped), one firm can supply the market at a lower total cost than can two or more firms. Regulators may regulate the price charged by the firm rather than force it to break up. In this exercise, you will find output, price, profit, and consumer surplus for a utility (say, an electricity provider) under three different pricing rules. The market demand equation is: P = 50 – 0.1Q The long run total cost equation is: TC = 3000 + 10Q a. Write the marginal revenue, marginal cost, and average cost equations. Confirm that the average cost curve is negatively sloped. MR = MC = AC = Slope of AC = dAC/dQ = b. GRAPH the demand, marginal revenue, marginal cost, and average cost curves. 100 200 300 400 500

Microeconomics A Contemporary Intro

10th Edition

ISBN:9781285635101

Author:MCEACHERN

Publisher:MCEACHERN

Chapter15: Economic Regulation And Antitrust Policy

Section: Chapter Questions

Problem 10PAE

Related questions

Question

Could I have help figuring out how to solve this problem?

Transcribed Image Text:21

12. Regulation of a Natural Monopoly

For a decreasing-cost industry natural monopoly (LRAC negatively sloped), one firm can supply

the market at a lower total cost than can two or more firms. Regulators may regulate the price charged

by the firm rather than force it to break up. In this exercise, you will find output, price, profit, and

consumer surplus for a utility (say, an electricity provider) under three different pricing rules.

The market demand equation is:

P = 50 – 0.1Q

The long run total cost equation is:

TC = 3000 + 10Q

a. Write the marginal revenue, marginal cost, and average cost equations. Confirm that the average

cost curve is negatively sloped.

MR =

MC =

AC =

Slope of AC = dAC/dQ =

b. GRAPH the demand, marginal revenue, marginal cost, and average cost curves.

100

200

300

400

500

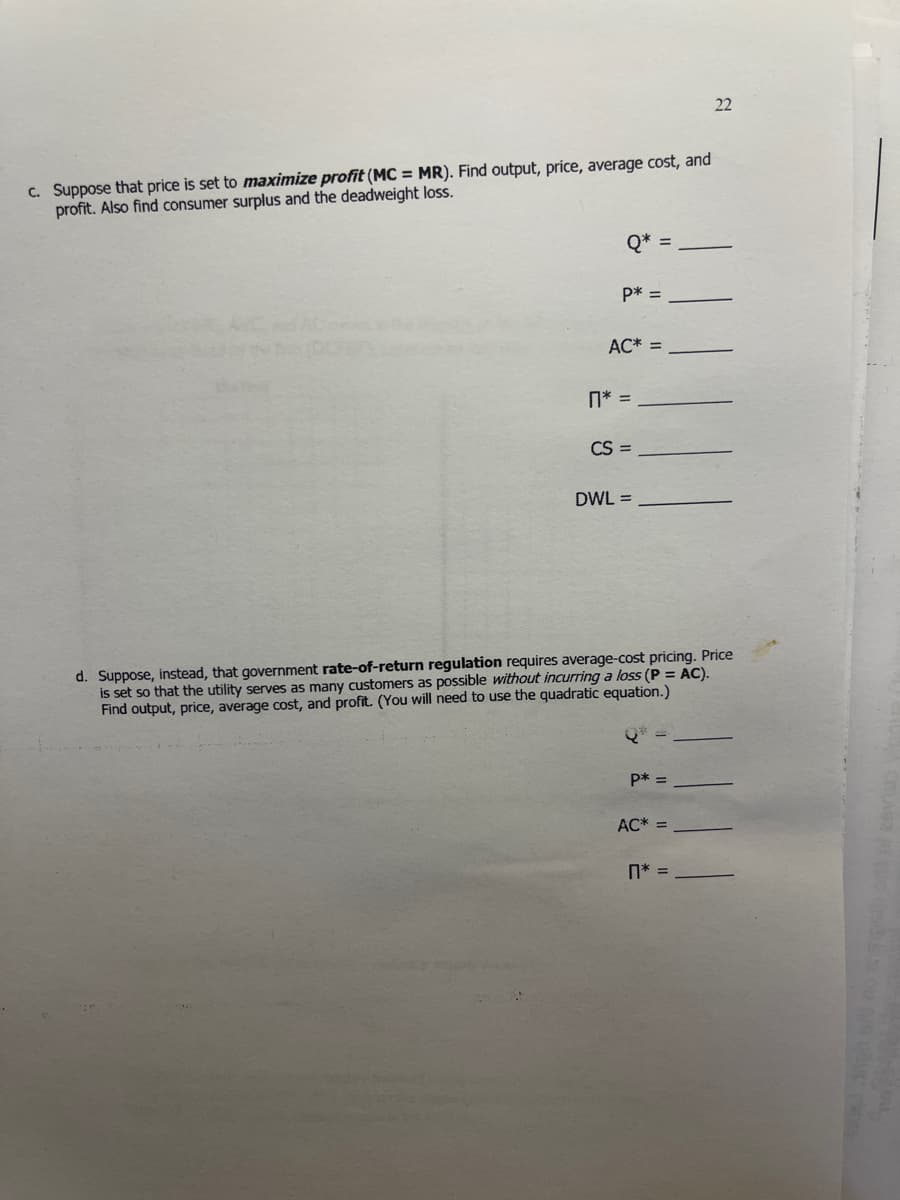

Transcribed Image Text:22

C. Suppose that price is set to maximize profit (MC = MR). Find output, price, average cost, and

profit. Also find consumer surplus and the deadweight loss.

Q* =

p* =

AC* =

n* =

CS =

DWL =

d. Suppose, instead, that government rate-of-return regulation requires average-cost pricing. Price

is set so that the utility serves as many customers as possible without incurring a loss (P = AC).

Find output, price, average cost, and profit. (You will need to use the quadratic equation.)

P* =

AC* =

n* =

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Economics, 7th Edition (MindTap Cou…

Economics

ISBN:

9781285165875

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Principles of Economics, 7th Edition (MindTap Cou…

Economics

ISBN:

9781285165875

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Principles of Economics (MindTap Course List)

Economics

ISBN:

9781305585126

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Principles of Microeconomics (MindTap Course List)

Economics

ISBN:

9781305971493

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning