2. Give the 2022 entries for MPS Company to record pension expense and funding. The 2022 records of MPS Company provided the following data related to its noncontributory, defined benefit pension plan (amounts in PO005): a. Accumulated benefit obligation (report of actuary) Beginning balance Service cost P3,000 1,200 240 Interest cost Pension benefits paid Ending balance Discount rate used by actuary, 8% b. Plan assets at fair value (report of trustee): Beginning balance Actual return on plan assets (400) P4,040 P2,400 168 Contributions Pension benefits paid Ending balance Expected long-term rate of return of plan assets, 7% 1,016 (400) Р3,192 c. January 1, 2022, balance of unrecognized prior service cost, gains and losses, and transaction cost, zero.

2. Give the 2022 entries for MPS Company to record pension expense and funding. The 2022 records of MPS Company provided the following data related to its noncontributory, defined benefit pension plan (amounts in PO005): a. Accumulated benefit obligation (report of actuary) Beginning balance Service cost P3,000 1,200 240 Interest cost Pension benefits paid Ending balance Discount rate used by actuary, 8% b. Plan assets at fair value (report of trustee): Beginning balance Actual return on plan assets (400) P4,040 P2,400 168 Contributions Pension benefits paid Ending balance Expected long-term rate of return of plan assets, 7% 1,016 (400) Р3,192 c. January 1, 2022, balance of unrecognized prior service cost, gains and losses, and transaction cost, zero.

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter19: Accounting For Post Retirement Benefits

Section: Chapter Questions

Problem 9MC

Related questions

Question

Transcribed Image Text:2. Give the 2022 entries for MPS Company to record pension expense

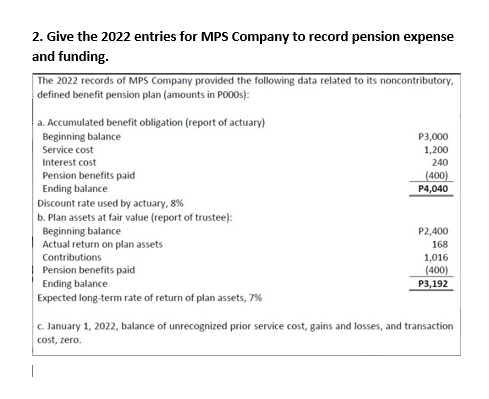

and funding.

The 2022 records of MPS Company provided the following data related to its noncontributory,

defined benefit pension plan (amounts in PO005):

a. Accumulated benefit obligation (report of actuary)

Beginning balance

P3,000

1,200

Service cost

Interest cost

240

Pension benefits paid

Ending balance

(400)

P4,040

Discount rate used by actuary, 8%

b. Plan assets at fair value (report of trustee):

Beginning balance

Actual return on plan assets

Contributions

400

168

Pension benefits paid

Ending balance

1,016

(400)

P3,192

Expected long-term rate of return of plan assets, 7%

c. January 1, 2022, balance of unrecognized prior service cost, gains and losses, and transaction

cost, zero.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning