26. Many of the people living with incomes below the global poverty line (around $500/person) are farmers. Max decides that he wants to help peanut farmers in a competitive market earn larger profit from their crops and invent a new method that helps conserve fertilizer and lower costs. (Some economists actually did some research like that.) This problem is about the short run and long run consequences. Suppose that before Max introduces the new method each farm has these costs. The farms are all assumed to be identical for simplicity. MC(q) = 2q + 12 9. ATC(q) =-+ 12 + q Fixed cost = $9 The units are all in kgs or $/kg. What is an individual farm's supply curve? а. q (P) 3D 0.5Р — 2 b. q(P) = –0.5P + 2 c. q(P) = 0.5P – 6 d. q(P) 3D —0.5Р + 6 %3D =

26. Many of the people living with incomes below the global poverty line (around $500/person) are farmers. Max decides that he wants to help peanut farmers in a competitive market earn larger profit from their crops and invent a new method that helps conserve fertilizer and lower costs. (Some economists actually did some research like that.) This problem is about the short run and long run consequences. Suppose that before Max introduces the new method each farm has these costs. The farms are all assumed to be identical for simplicity. MC(q) = 2q + 12 9. ATC(q) =-+ 12 + q Fixed cost = $9 The units are all in kgs or $/kg. What is an individual farm's supply curve? а. q (P) 3D 0.5Р — 2 b. q(P) = –0.5P + 2 c. q(P) = 0.5P – 6 d. q(P) 3D —0.5Р + 6 %3D =

Microeconomics: Private and Public Choice (MindTap Course List)

16th Edition

ISBN:9781305506893

Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Chapter8: Costs And The Supply Of Goods

Section: Chapter Questions

Problem 19CQ

Related questions

Question

Transcribed Image Text:26. Many of the people living with incomes below the global poverty line (around $500/person) are

farmers. Max decides that he wants to help peanut farmers in a competitive market earn larger profits

from their crops and invent a new method that helps conserve fertilizer and lower costs. (Some

economists actually did some research like that.) This problem is about the short run and long run

consequences.

Suppose that before Max introduces the new method each farm has these costs. The farms are all

assumed to be identical for simplicity.

MC(q) = 2q + 12

ATC(q)

9

+ 12 + q

Fixed cost = $9

The units are all in kgs or $/kg.

%3D

What is an individual farm's supply curve?

a. q(P) = 0.5P – 2

b. q (P) %3D — 0.5Р + 2

с. q (Р) 3D 0.5Р — 6

d. q (P) %3D — 0.5Р +6

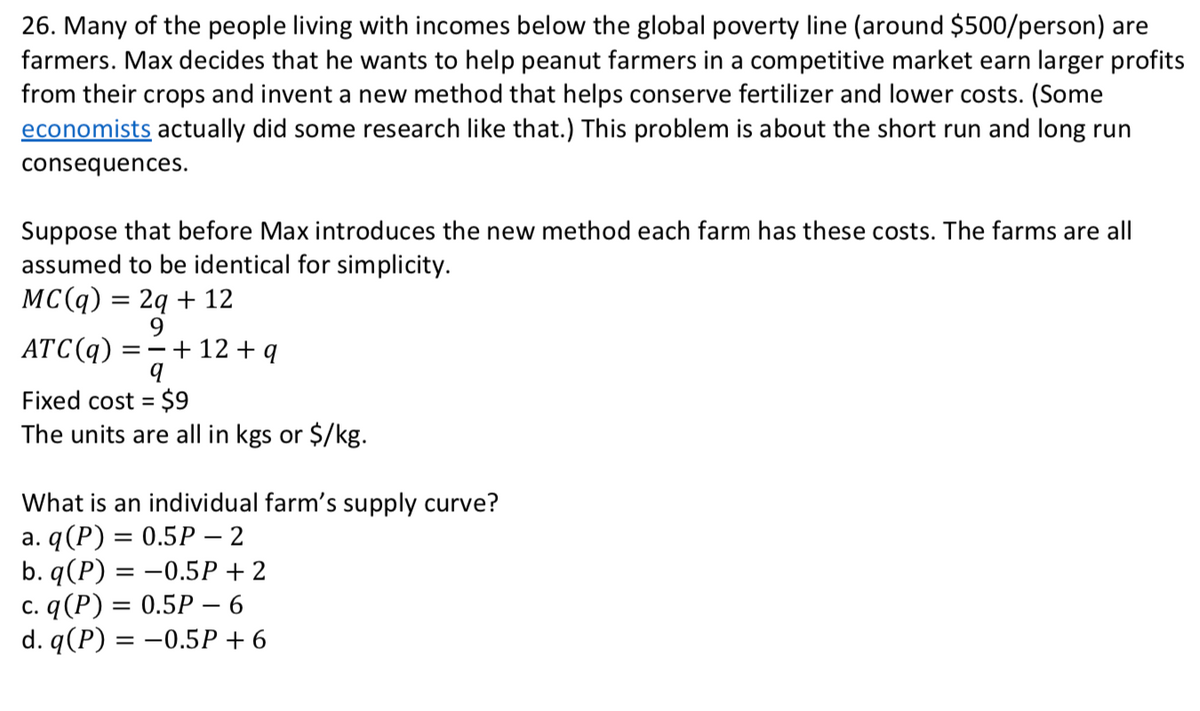

![27. (continued) There are four farms so what is the short run market supply curve? Combine that market

supply with this estimated market demand, Q(P) = 60 – P, to find the market price. Determine how

much each firm produces and what each firm makes in profit.

N = $

%3D

28. (continued) Now you introduce the new method which reduces the variable costs. As a result the MC

and ATC are lower:

MCС(q) %3D 2q + 6

9.

=-+6+q

ATC(q)

Repeat the steps above to find the new short run equilibrium.

How much profit does each firm now make? (this should be higher)

29. (continued) What will happen in the long run as farmers are allowed to enter or exit? Check the

boxes below for the variables that will decrease in the long run compared to the short run equilibrium

you found in the previous question.

[] N, the number of firms

[] P, the market price

[] q, the quantity each firm produces

[] T, the profit of an individual firm

[] ATC, the average total cost of each firm](/v2/_next/image?url=https%3A%2F%2Fcontent.bartleby.com%2Fqna-images%2Fquestion%2Ff0aac786-f258-42a6-87e3-0118f536800f%2F22caad20-e42a-4737-a9a1-1d0dc4c7281e%2Fwpunjxp_processed.png&w=3840&q=75)

Transcribed Image Text:27. (continued) There are four farms so what is the short run market supply curve? Combine that market

supply with this estimated market demand, Q(P) = 60 – P, to find the market price. Determine how

much each firm produces and what each firm makes in profit.

N = $

%3D

28. (continued) Now you introduce the new method which reduces the variable costs. As a result the MC

and ATC are lower:

MCС(q) %3D 2q + 6

9.

=-+6+q

ATC(q)

Repeat the steps above to find the new short run equilibrium.

How much profit does each firm now make? (this should be higher)

29. (continued) What will happen in the long run as farmers are allowed to enter or exit? Check the

boxes below for the variables that will decrease in the long run compared to the short run equilibrium

you found in the previous question.

[] N, the number of firms

[] P, the market price

[] q, the quantity each firm produces

[] T, the profit of an individual firm

[] ATC, the average total cost of each firm

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Microeconomics: Private and Public Choice (MindTa…

Economics

ISBN:

9781305506893

Author:

James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:

Cengage Learning

Economics: Private and Public Choice (MindTap Cou…

Economics

ISBN:

9781305506725

Author:

James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:

Cengage Learning

Principles of Economics 2e

Economics

ISBN:

9781947172364

Author:

Steven A. Greenlaw; David Shapiro

Publisher:

OpenStax

Microeconomics: Private and Public Choice (MindTa…

Economics

ISBN:

9781305506893

Author:

James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:

Cengage Learning

Economics: Private and Public Choice (MindTap Cou…

Economics

ISBN:

9781305506725

Author:

James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:

Cengage Learning

Principles of Economics 2e

Economics

ISBN:

9781947172364

Author:

Steven A. Greenlaw; David Shapiro

Publisher:

OpenStax