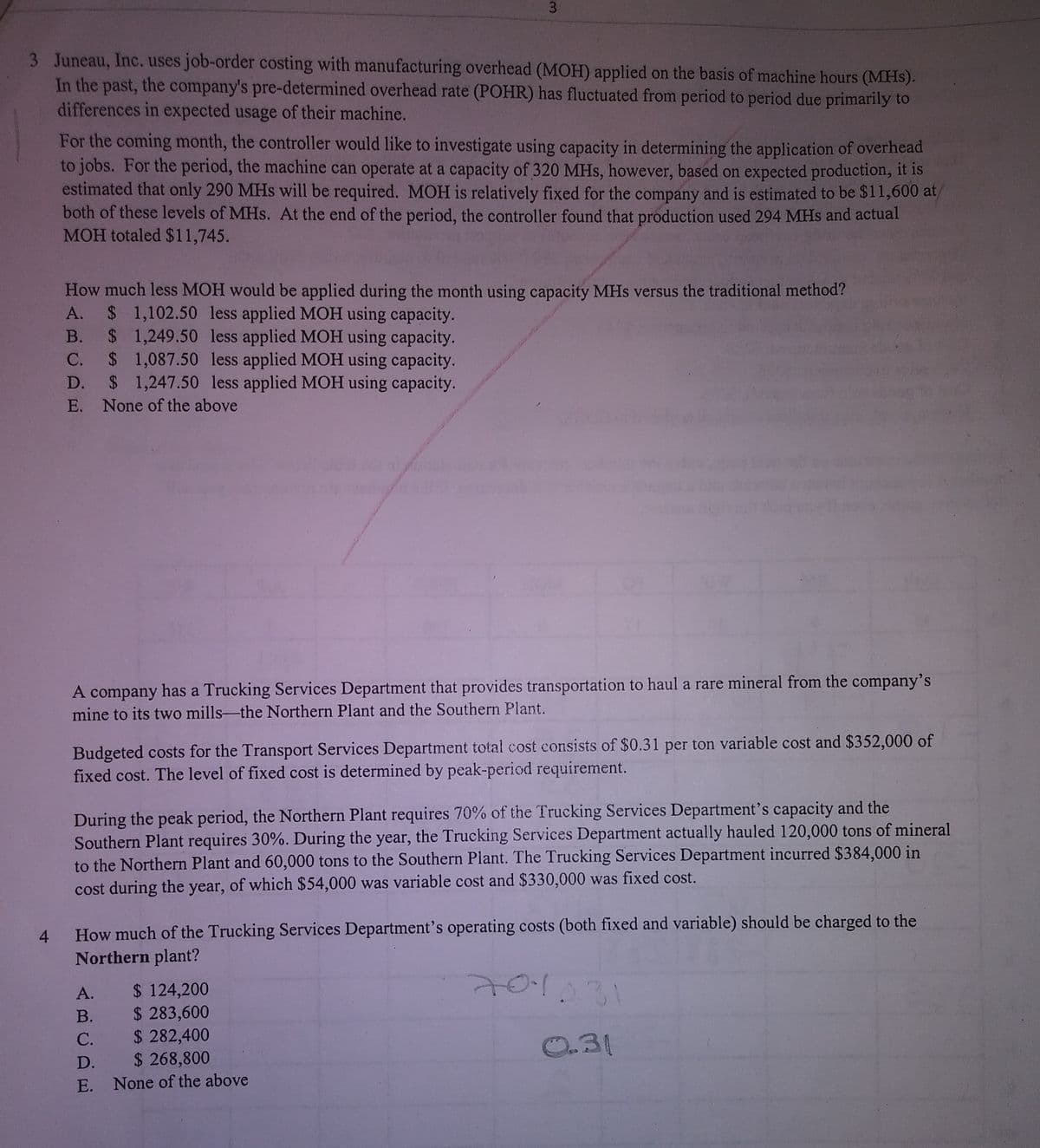

3 Juneau, Inc. uses job-order costing with manufacturing overhead (MOH) applied on the basis of machine hours (MHs). In the past, the company's pre-determined overhead rate (POHR) has fluctuated from period to period due primarily to differences in expected usage of their machine. For the coming month, the controller would like to investigate using capacity in determining the application of overhead to jobs. For the period, the machine can operate at a capacity of 320 MHs, however, based on expected production, it is estimated that only 290 MHs will be required. MOH is relatively fixed for the company and is estimated to be $11,600 at/ both of these levels of MHs. At the end of the period, the controller found that production used 294 MHs and actual MOH totaled $11,745. How much less MOH would be applied during the month using capacity MHs versus the traditional method? $ 1,102.50 less applied MOH using capacity. $ 1,249.50 less applied MOH using capacity. $ 1,087.50 less applied MOH using capacity. $ 1,247.50 less applied MOH using capacity. А. В. С. D. E. None of the above

3 Juneau, Inc. uses job-order costing with manufacturing overhead (MOH) applied on the basis of machine hours (MHs). In the past, the company's pre-determined overhead rate (POHR) has fluctuated from period to period due primarily to differences in expected usage of their machine. For the coming month, the controller would like to investigate using capacity in determining the application of overhead to jobs. For the period, the machine can operate at a capacity of 320 MHs, however, based on expected production, it is estimated that only 290 MHs will be required. MOH is relatively fixed for the company and is estimated to be $11,600 at/ both of these levels of MHs. At the end of the period, the controller found that production used 294 MHs and actual MOH totaled $11,745. How much less MOH would be applied during the month using capacity MHs versus the traditional method? $ 1,102.50 less applied MOH using capacity. $ 1,249.50 less applied MOH using capacity. $ 1,087.50 less applied MOH using capacity. $ 1,247.50 less applied MOH using capacity. А. В. С. D. E. None of the above

College Accounting, Chapters 1-27

23rd Edition

ISBN:9781337794756

Author:HEINTZ, James A.

Publisher:HEINTZ, James A.

Chapter26: Manufacturing Accounting: The Job Order Cost System

Section: Chapter Questions

Problem 5SEB: PREDETERMINED FACTORY OVERHEAD RATE Marston Enterprises calculates a predetermined factory overhead...

Related questions

Question

Please I want to learn how to make these problems with a good explanation. One of those there is the possible answer.

Thank you

Transcribed Image Text:3

3 Juneau, Inc. uses job-order costing with manufacturing overhead (MOH) applied on the basis of machine hours (MHs).

In the past, the company's pre-determined overhead rate (POHR) has fluctuated from period to period due primarily to

differences in expected usage of their machine.

For the coming month, the controller would like to investigate using capacity in determining the application of overhead

to jobs. For the period, the machine can operate at a capacity of 320 MHs, however, based on expected production, it is

estimated that only 290 MHs will be required. MOH is relatively fixed for the company and is estimated to be $11,600 at/

both of these levels of MHs. At the end of the period, the controller found that production used 294 MHs and actual

MOH totaled $11,745.

How much less MOH would be applied during the month using capacity MHs versus the traditional method?

$ 1,102.50 less applied MOH using capacity.

$ 1,249.50 less applied MOH using capacity.

$ 1,087.50 less applied MOH using capacity.

$ 1,247.50 less applied MOH using capacity.

А.

В.

С.

D.

E. None of the above

A company has a Trucking Services Department that provides transportation to haul a rare mineral from the company's

mine to its two mills-the Northern Plant and the Southern Plant.

A

Budgeted costs for the Transport Services Department total cost consists of $0.31 per ton variable cost and $352,000 of

fixed cost. The level of fixed cost is determined by peak-period requirement.

During the peak period, the Northern Plant requires 70% of the Trucking Services Department's capacity and the

Southern Plant requires 30%. During the year, the Trucking Services Department actually hauled 120,000 tons of mineral

to the Northern Plant and 60,000 tons to the Southern Plant. The Trucking Services Department incurred $384,000 in

cost during the year, of which $54,000 was variable cost and $330,000 was fixed cost.

How much of the Trucking Services Department's operating costs (both fixed and variable) should be charged to the

Northern plant?

4

$ 124,200

$ 283,600

$ 282,400

$ 268,800

E. None of the above

А.

В.

С.

O.31

D.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Recommended textbooks for you

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Excel Applications for Accounting Principles

Accounting

ISBN:

9781111581565

Author:

Gaylord N. Smith

Publisher:

Cengage Learning