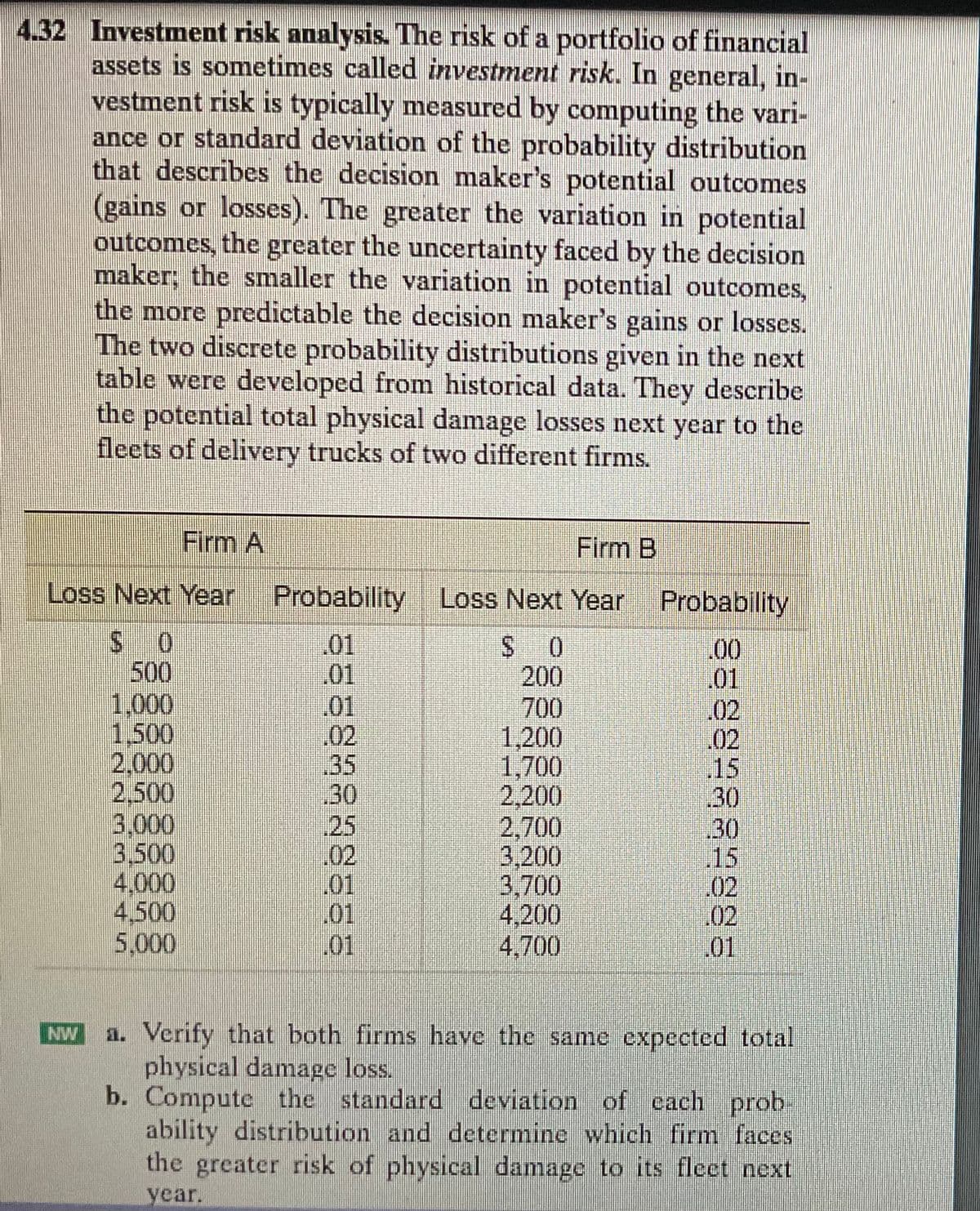

4.32 Investment risk analysis. The risk of a portfolio of financial assets is sometimes called investment risk. In general, in- vestment risk is typically measured by computing the vari- ance or standard deviation of the probability distribution that describes the decision maker's potential outcomes (gains or losses). The greater the variation in potential outcomes, the greater the uncertainty faced by the decision maker; the smaller the variation in potential outcomes, the more predictable the decision maker's gains or losses. The two discrete probability distributions given in the next table were developed from historical data. They describe the potential total physical damage losses next year to the fleets of delivery trucks of two different firms. Loss Next Year $0 500 NW 1,000 1,500 2,000 2,500 Firm A 3,000 3,500 4,000 4,500 5,000 Firm B Probability Loss Next Year $0 200 .01 .01 35 .30 .02 .01 .01 .01 700 1,200 1,700 2,200 2,700 3,200 3,700 4,200 4,700 Probability 00 .01 .02 .30 .30 .02 01 a. Verify that both firms have the same expected total physical damage loss. b. Compute the standard deviation of each prob- ability distribution and determine which firm faces the greater risk of physical damage to its fleet next

4.32 Investment risk analysis. The risk of a portfolio of financial assets is sometimes called investment risk. In general, in- vestment risk is typically measured by computing the vari- ance or standard deviation of the probability distribution that describes the decision maker's potential outcomes (gains or losses). The greater the variation in potential outcomes, the greater the uncertainty faced by the decision maker; the smaller the variation in potential outcomes, the more predictable the decision maker's gains or losses. The two discrete probability distributions given in the next table were developed from historical data. They describe the potential total physical damage losses next year to the fleets of delivery trucks of two different firms. Loss Next Year $0 500 NW 1,000 1,500 2,000 2,500 Firm A 3,000 3,500 4,000 4,500 5,000 Firm B Probability Loss Next Year $0 200 .01 .01 35 .30 .02 .01 .01 .01 700 1,200 1,700 2,200 2,700 3,200 3,700 4,200 4,700 Probability 00 .01 .02 .30 .30 .02 01 a. Verify that both firms have the same expected total physical damage loss. b. Compute the standard deviation of each prob- ability distribution and determine which firm faces the greater risk of physical damage to its fleet next

Chapter8: Analysis Of Risk And Return

Section: Chapter Questions

Problem 13QTD

Related questions

Question

Transcribed Image Text:4.32 Investment risk analysis. The risk of a portfolio of financial

assets is sometimes called investment risk. In general, in-

vestment risk is typically measured by computing the vari-

ance or standard deviation of the probability distribution

that describes the decision maker's potential outcomes

(gains or losses). The greater the variation in potential

outcomes, the greater the uncertainty faced by the decision

maker; the smaller the variation in potential outcomes,

the more predictable the decision maker's gains or losses.

The two discrete probability distributions given in the next

table were developed from historical data. They describe

the potential total physical damage losses next year to the

fleets of delivery trucks of two different firms.

Loss Next Year

SO

500

NW

1,000

1,500

2,000

2.500

Firm A

3.000

3,500

4,000

4,500

5,000

Firm B

Probability Loss Next Year

01

SO 0

.01

200

.01

700

1,200

1,700

2,200

2,700

3.200

3.700

4,200

4,700

30

.01

01

Probability

85984579985

.30

a. Verify that both firms have the same expected total

physical damage loss.

b.

Compute the standard deviation of cach prob.

ability distribution and determine which firm faces

the greater risk of physical damage to its fleet next

year.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 8 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT