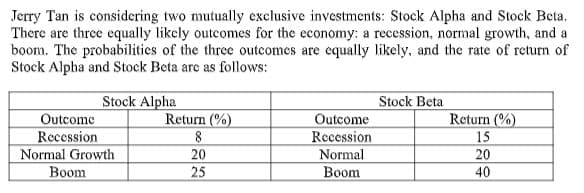

(a) (i) Calculate the expected returns and standard deviations of Stock Alpha and Stock Beta. (a) (ii) Assuming that Jerry Tan is a risk-adverse investor, recommend which stock he should select for long term investment. (b) Suppose that Jerry Tan has surplus funds to invest in both stocks, Alpha and Beta. He has decided to form a portfolio with investment in both stocks. The correlation coefficient between the expected return of both stocks is 0.8 and the weightage of investment is 40% for Stock Alpha and 60% for Stock Beta. Required: (i) Compute the expected return, Standard Deviation and Variance of the portfolio.

(a) (i) Calculate the expected returns and standard deviations of Stock Alpha and Stock Beta.

(a) (ii) Assuming that Jerry Tan is a risk-adverse investor, recommend which stock he should select for long term investment.

(b) Suppose that Jerry Tan has surplus funds to invest in both stocks, Alpha and Beta. He has decided to form a portfolio with investment in both stocks. The correlation coefficient between the expected return of both stocks is 0.8 and the weightage of investment is 40% for Stock Alpha and 60% for Stock Beta.

Required:

(i) Compute the expected return, Standard Deviation and Variance of the portfolio.

(c) Explain the specific risk and market risk in details, which affecting a company or a group of companies that represent a sector of the stock market.

(d) Give THREE (3) reasons why airlines and machine tool manufacturers have substantial macro and market risks.

Step by step

Solved in 4 steps with 3 images