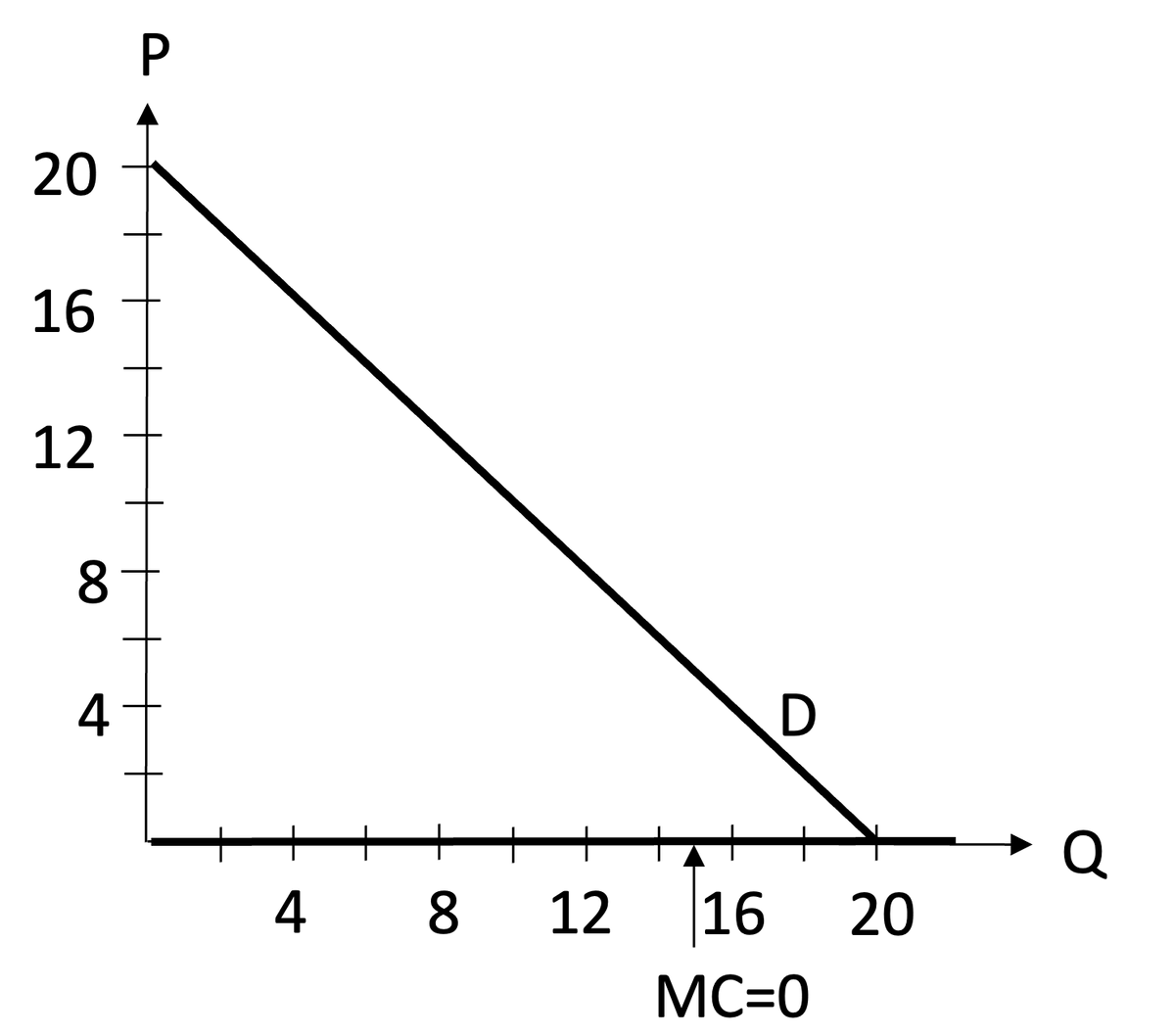

A monopolist has a single customer with the demand curve P=20-Q. (So this customer will buy different quantities at different prices.) Suppose the monopolist’s marginal cost is MC=0. (And assume FC=0 to keep things simple.) a) The monopolist uses “standard” pricing, i.e., it sets a single price for all units that the customer buys. The graph below shows the demand curve and MC curve. Solve graphically for the price & quantity that will maximize profit for the monopolist. Shade the areas on your graph that represent consumer surplus and the monopolist’s profit. Having observed the success of the monopolist in part (a), you’re plotting to enter the market and tempt the single customer to switch to you. Assume the following: You also have FC=0 and MC=0. You and the monopolist produce identical products, so if you do attract away the single customer, they come to you with the same demand curve as above, i.e., P=20-Q IMPORTANT: The monopolist has committed to their price from part (a), even if you ent

A monopolist has a single customer with the demand curve P=20-Q. (So this customer will buy different quantities at different prices.) Suppose the monopolist’s marginal cost is MC=0. (And assume FC=0 to keep things simple.)

a) The monopolist uses “standard” pricing, i.e., it sets a single

Having observed the success of the monopolist in part (a), you’re plotting to enter the market and tempt the single customer to switch to you. Assume the following:

- You also have FC=0 and MC=0.

- You and the monopolist produce identical products, so if you do attract away the single customer, they come to you with the same demand curve as above, i.e., P=20-Q

- IMPORTANT: The monopolist has committed to their price from part (a), even if you enters. (E.g., the monopolist has publicly posted their price from (a) and it can’t be adjusted.)

b) One way for you to enter the market is to employ “standard” pricing. If you do that and wish to tempt the customer to switch to you, then the price that will maximize your profit is 1 penny less that the monopolist’s posted price from (a). If you announce that price, how many units will the customer buy from you and what will be your profit?

c) As an alternative to the “standard” pricing in part(b), you decide to study whether a two-part tariff might be an effective way to tempt the customer to switch to you.

IMPORTANT REQUIREMENT: The monopolist’s price in part (a) is still available to the customer, and that means that the customer will only switch to you if they are better off buying from you than from the monopolist.

What is the two-part tariff that maximizes your profit? Explain your answer and explain how it addresses this requirement. What is your profit with your answer? What is the consumer’s CS with your answer?

Trending now

This is a popular solution!

Step by step

Solved in 2 steps