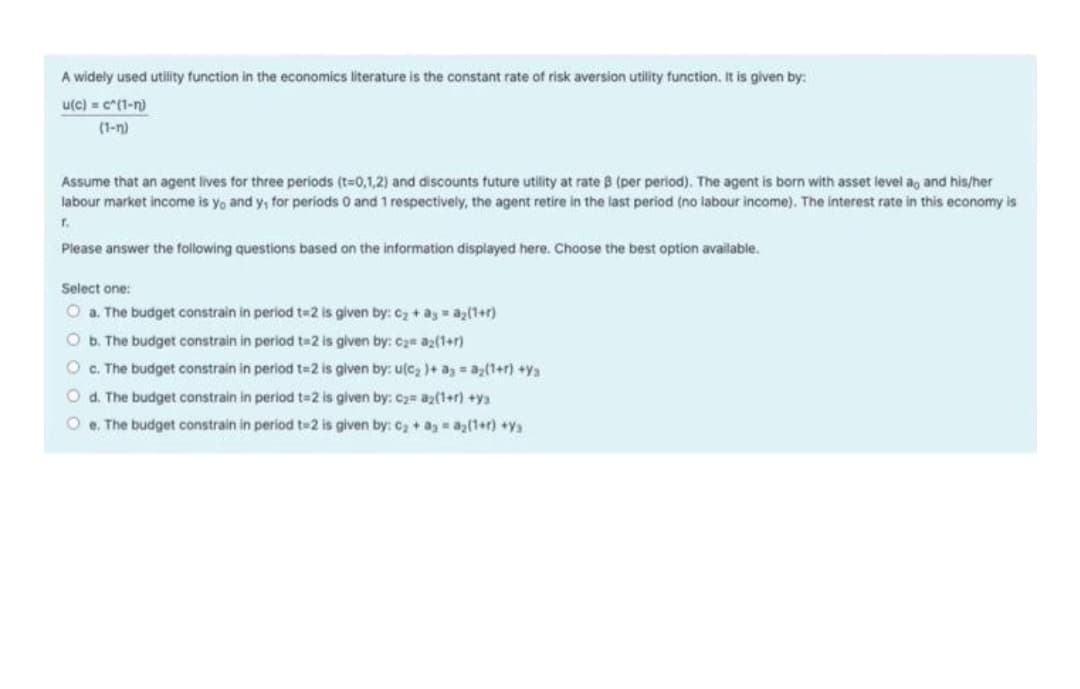

A widely used utility function in the economics literature is the constant rate of risk aversion utility function. It is given by: u(c) = c*(1-n) (1-n) Assume that an agent lives for three periods (t-0,1,2) and discounts future utility at rate B (per period). The agent is born with asset level ag and his/her labour market income is yo and y, for periods O and 1 respectively, the agent retire in the last period (no labour income). The interest rate in this economy is r. Please answer the following questions based on the information displayed here. Choose the best option available.

A widely used utility function in the economics literature is the constant rate of risk aversion utility function. It is given by: u(c) = c*(1-n) (1-n) Assume that an agent lives for three periods (t-0,1,2) and discounts future utility at rate B (per period). The agent is born with asset level ag and his/her labour market income is yo and y, for periods O and 1 respectively, the agent retire in the last period (no labour income). The interest rate in this economy is r. Please answer the following questions based on the information displayed here. Choose the best option available.

Chapter19: Externalities And Public Goods

Section: Chapter Questions

Problem 19.11P

Related questions

Question

Transcribed Image Text:A widely used utility function in the economics literature is the constant rate of risk aversion utility function. It is given by:

u(c) = c*(1-n)

(1-n)

Assume that an agent lives for three periods (t-0,1,2) and discounts future utility at rate B (per period). The agent is born with asset level a, and his/her

labour market income is yo and y, for periods O and 1 respectively, the agent retire in the last period (no labour income). The interest rate in this economy is

r.

Please answer the following questions based on the information displayed here. Choose the best option available.

Select one:

O a. The budget constrain in period t=2 is given by:C2+ ay az(1+r)

O b. The budget constrain in period t=2 is given by: Cam a2(1+r)

O C. The budget constrain in period t=2 is given by: u(c2)+ a a;(1+r) +ys

O d. The budget constrain in period t=2 is given by: C2= az(1+r) +ya

O e. The budget constrain in period t#2 is given by: C2+a a(1+r) +ya

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Recommended textbooks for you