An automated turning machine is the current constraint at Jordison Corporation. Three products use this constrained resource. Data concerning those products appear below. LN JQ $168.82 $313.84 $403.08 $139.72 $245.80 $287.56 4. 20 RQ Selling price per unit Variable cost per unit Minutes on the constraint 1.50 7.60 Rank the products in order of their current profitability from most profitable to least profitable, In other words, rank the products in the order in which they should be emphasized. (Round your Intermedlate calculations to 2 decimal places.)

An automated turning machine is the current constraint at Jordison Corporation. Three products use this constrained resource. Data concerning those products appear below. LN JQ $168.82 $313.84 $403.08 $139.72 $245.80 $287.56 4. 20 RQ Selling price per unit Variable cost per unit Minutes on the constraint 1.50 7.60 Rank the products in order of their current profitability from most profitable to least profitable, In other words, rank the products in the order in which they should be emphasized. (Round your Intermedlate calculations to 2 decimal places.)

Chapter14: Capital Structure Management In Practice

Section14.A: Breakeven Analysis

Problem 7P

Related questions

Question

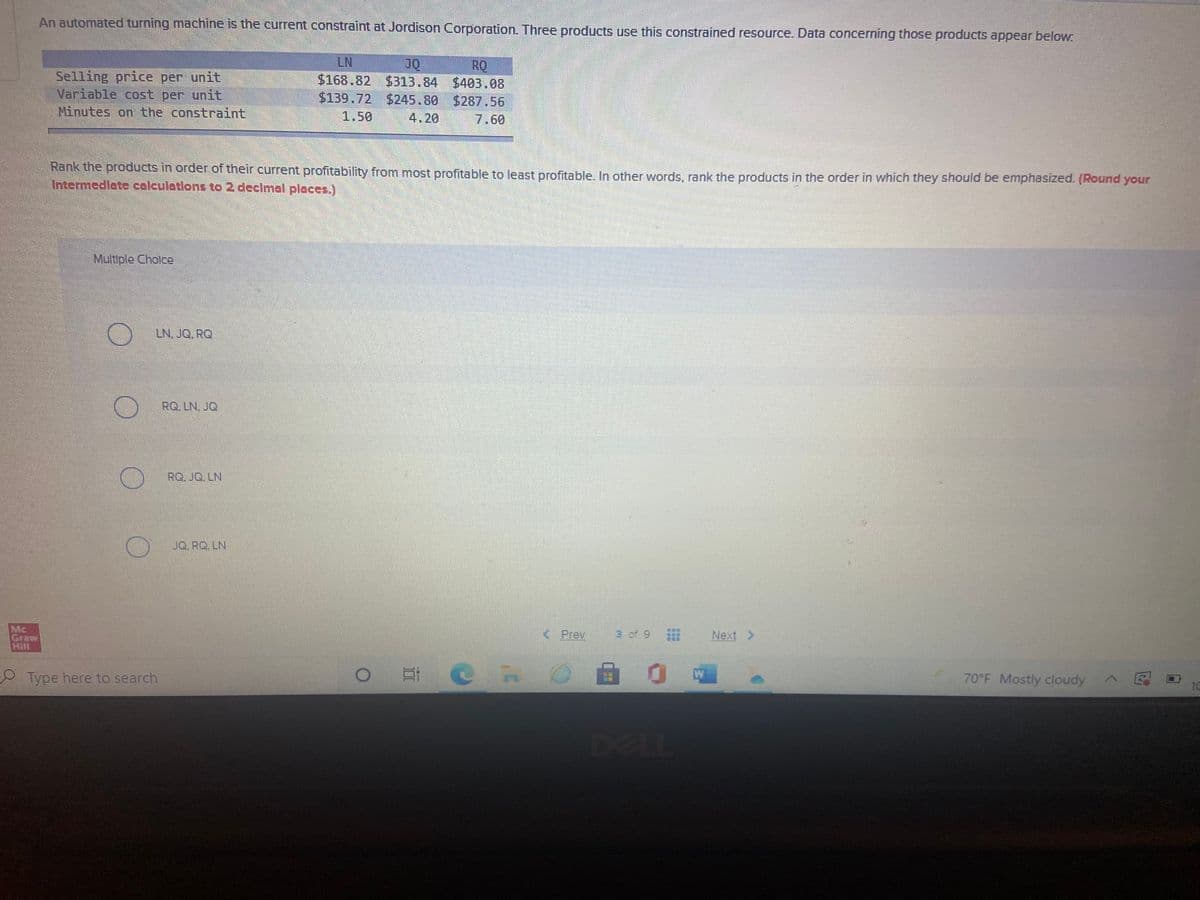

Transcribed Image Text:An automated turning machine is the current constraint at Jordison Corporation. Three products use this constrained resource. Data concerning those products appear below:

LN

JQ

$168.82 $313.84 $403.08

$139.72 $245.80 $287.56

RQ

Selling price per unit

Variable cost per unit

Minutes on the constraint

1.50

4.20

7.60

Rank the products in order of their current profitability from most profitable to least profitable, In other words, rank the products in the order in which they should be emphasized. (Round your

Intermedlate calculations to 2 declmoal places.)

Multiple Cholce

LN. JQ. RQ

RQ. LN. JQ

RQ. JQ. LN

JQ. RQ LN

Mc

Graw

Hill

< Prev

3 of 9

Next >

Type here to search

70°F Mostly cloudy

10

DELL

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 1 images

Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College