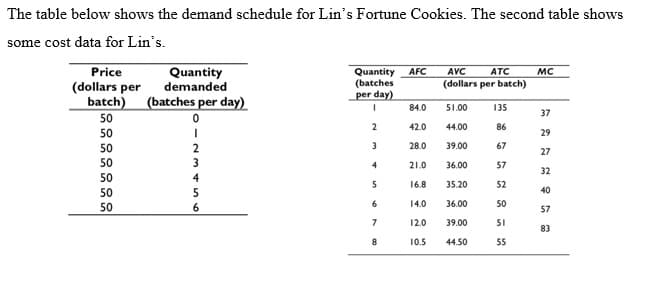

At a market price of $83 a batch, what quantity does Lin’s produce and what is the firm’s economic profit in the short run? Do firms enter or exit the market and what is Lin’s economic profit in the long run?

Q: 1. Suvreen runs a flower shop in a perfectly competitive market and sells each flower bouquet for…

A: Since you have posted a question with multiple sub-parts, we will solve first three subparts for…

Q: Now, suppose in addition that the market demand is Q = 18,000 - 100p. (d) In the long run…

A: Perfect competition(PC) is that market structure where there are infinite number of buyers and…

Q: Suppose that the agricultural sector is perfectly competitive. Also suppose that all current…

A: Here market equilibrium price is at $1.99 which is greater than ATC $1.50 per pound of roma…

Q: At a market price of $35.20 a batch, what quantity does Lin’s produce and what is the firm’s…

A: Price (dollars per batch) Quantity demanded (batches per day) Total Revenue Marginal…

Q: Suppose the shirts industry is perfectly competitive and begins in a long-run equilibrium. (a)…

A: Perfect competition refers to the situation where there are many buyers and sellers exist in the…

Q: graph shows the short run cot curve of a firm in a purely competitive market. Which of the following…

A: The profit maximizing output for the firm occurs where the (the upward sloping part of the) marginal…

Q: MC E ATC AVC Output igure 8.7 shows cost curves for Penny's Parasols, a perfectly competitive firm.…

A: In perfect competition, eqm. Q(quantity) is determined by the intersection of MC(marginal cost) and…

Q: a. Is the firm making an economic profit or loss? b. Will firms enter or exit this market? c. Sketch…

A: Firms in a perfectly competitive market face a perfectly elastic individual demand curve as they…

Q: When might a competitive firm shutdown in the short run and exit the market in the long run?

A: When a perfectly competitive firm finds itself in shutdown, that is, its market price is equal to…

Q: (d) Find an expression for Chetan's supply curve. (e) Sketch Chetan's supply curve, his marginal…

A: Chetan's Fishing rods is a price taker so they are operating in perfectly competitive market. Chetan…

Q: Why is a firm in a perfectly competitive market called a price taker? Why do the price, MR and…

A: In a perfectly competitive market there are large number of firms producing identical products thus…

Q: Give an example of a firm which competes in a competitive market. Explain. Suppose that the this…

A: Perfect competition is a benchmark, or "ideal market," to which real market designs can measure up.…

Q: following graph shows the market demand and supply curves for camisoles that are sold in a perfectly…

A: Below is the edited graph:

Q: Using graph, explain when the firm in a competitive market is in equilibrium?

A: A market is a place where the buyers and the sellers interact with each other and the exchange of…

Q: The graph below displays the short-run cost curves for Paola's Pears, a small farm competing in the…

A: perfect competition market is the form of market where large numbers of sellers and buyers exchange…

Q: The situation facing by firm “Smart”, a producer of running shoes, is shown in the following…

A: A monopolistic firm shares similar profit-maximizing constraint as the monopoly firm according to…

Q: . Calculate profit for each quantity. How much should the firm produce to maximize profut ? b.…

A:

Q: The market for fertilizer is perfectly competitive.Firms in the market are producing output but…

A: a) In the competitive market, the firms produce to the level where the price (P) and marginal cost…

Q: Mariel runs an ice cream shop. Her short-run cost is given by 300 + 3000 + 3g where q s the number…

A: TC(total cost) has 2 components- TFC(total fixed cost) and TVC(total variable cost). ATC(average…

Q: Assume that Harry Ellis produces table lamps in the perfectly competitive table lamp market. OUTPUT…

A: Fixed Cost refers to that part or component of cost that remains fixed despite the varying quantity…

Q: Assume hotdog stands in New York are in a perfectly competitive market. Jacob is taking over a hot…

A: Hi student, thanks for posting the question. A per the guideline we are providing answer for the…

Q: Only answer question 6A

A: Total variable cost is the cost of producing an output which increases with an increase in the…

Q: 1.1) Complete the table. 1.2) Draw a graph for each AVC, ATC and MC on one graph. 1.3) Suppose…

A: Q TC TFC TVC AVC AFC ATC TR1( at p = 20) MC MR1 MR 2( at p= 60) 0 50 50 - - - - 0 - - - 1 70 50…

Q: If economic profits are being made in a perfectly competitive market, then firms will ________ the…

A: The equilibrium price and quantity of a good sold in the market are determined by the forces of…

Q: Farmer Jones grows oranges in Florida. Suppose the market for oranges is perfectly competitive and…

A: we can fill the table by calculating the TR , MR , AR which are as follow-

Q: an excess profit be earned in perfectly competitive markets in the long run. Explain.

A: Perfect competition refers to the market where there is large number of buyers and sellers who deal…

Q: Sterling runs a donut shop which which is being operated in a perfectly competitive market where…

A: Firms in perfectly competitive market, are price taking firms because there are a large number of…

Q: At a market price of $21 a toy, what quantity does the firm produce in the short run and does the…

A: The fixed cost of production is the cost which remains the same at all the levels of income. This…

Q: What is Economic profit

A: Economic profit refers to the profit that obtained by deducting the implicit cost or opportunity…

Q: Whe Should a firm close or shut down in a perfect competitive market or firm?

A: In a perfect competition, a firm thinks to shut down when it faces losses. That is, when Revenues…

Q: 29. In the long run, a profit maximizing firm will choose to exit a market when a. fixei costs…

A: In the short-run, a firm exits a market if it is not able to cover its variable costs, i.e., it…

Q: At his profit maximizing output, what is the total profit earned by Tim?

A: Answer: A monopolistically competitive firm maximizes its profit where the marginal revenue (MR) is…

Q: What is Jacob’s average fixed cost (per day)? What is his variable cost (per day)? And finally, what…

A: Since you have posted a question with multiple sub-parts, we will solve first three subparts for…

Q: a. Complete the table by filling in the values for profit, marginal revenue, and marginal cost. b.…

A: Total cost is the cost incurred by the firm for the production of final goods. The cost is divided…

Q: Lisa lawn company (LLC) is a lawn mowing business in a perfectly competitive market for lawn moving…

A: Disclaimer- “Since you have asked multiple question, we will solve the first three question for you…

Q: Suppose the book-printing industry is competitive and begins in long-run equilibrium. a. Draw a…

A: a) Typical firm in the industry The Above figure 1 shows the curves of a typical firm in the…

Q: 2. Many small boats are made of fiberglass, which is derived from crude oil. Suppose that the price…

A: In an economy, oil is considered as a cruical resource because it can be used in various areas and…

Q: 6. The following figure shows long-run average and marginal cost curves for a competitive firm. The…

A: The measure that depicts expenses being incurred by the entity for carrying out its day-to-day…

Q: Assume that apples are produced in a perfectly competitive market. Grande’s Orchard is a typical…

A: When market demand increases, the value of the nice rises, and therefore the market quantity…

Q: Is the firm maximizing profit? 2. What quantity of output should the firm produce in the long run

A: 1. Given the values: TC = 70 + 10q + 2q2MC = 10 +4q Price = MR = $20 At profit maximizing, MR=MC MR…

Q: Why is a firm in a perfectly competitive market called a price taker? Why do the price, MR and…

A: Perfect competition: It refers to the market in which the firms are the price taker and the buyers…

Q: Lisa’s Lawn Company (LLC) is a lawn-mowing business in a perfectly competitive market for…

A: Marginal cost is the change in cost of production stemming from one more unit of production of the…

Q: A. If a firm operating in a perfectly competitive market doubles the amount it sells, what happens…

A: a) Firms are price taker in perfectly competitive market. So, when the firm doubles the amount it…

Q: 5. Profit maximization and shutting down in the short run Suppose that the market for microwave…

A:

Q: d. What happens to the quantity of running shoes in the entire market in the long run? e. Does Lite…

A: As Lite and Kool Inc. earn an economic profit in the short-run, new firms will enter the market and…

Q: Show what happens in the short run on both graphs when a new medical study shows soybeans to be…

A: In a perfect competition market, individual firms supply their goods at prices that are determined…

Q: -run equilibrium in a perfectly competitive market, firms earn positive economic profits. Is…

A: A perfect competition is where there is free market entry for the firms. If the firm earns profits…

At a market price of $83 a batch, what quantity does Lin’s produce and what is the firm’s economic profit in the short run? Do firms enter or exit the market and what is Lin’s economic profit in the long run?

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

- What two lines on a cost curve diagram intersect at the shutdown point?A computer company produces affordable, easy-to-use home computer systems and has fixed costs of 250. The marginal cost of producing computers is 700 for the first computer, 250 for the second, 300 for the third, 350 for the fourth, 430 for the fifth, 450 for the sixth, and 500 for the seventh. Create a table that shows the companys output, total cost, marginal cost, average cost, variable cost, and average variable cost. At what price is the zero-profit point? At what price is the shutdown point? If the company sells the computers for 500, is it making a profit or a loss? How big is the profit or loss? Sketch a graph with AC, MC, and AVG curves to illustrate your answer and show the profit or loss. If the firm sells the computers for 300, is it making a profit or a loss? How big is the profit or loss? Sketch a graph with AC, MC, and AVG curves to illustrate your answer and show the profit or loss.Ariana Grande has just finished recording her latestCD. Her record company’s marketing departmentdetermines that the demand for the CD is asfollows:Price Number of CDs$24 10,00022 20,00020 30,00018 40,00016 50,00014 60,000The company can produce the CD with no fixed costand a variable cost of $5 per CD.a. Find total revenue for quantity equal to 10,000,20,000, and so on. What is the marginal revenuefor each 10,000 increase in the quantity sold?

- A toy manufacturer makes miniature trucks. The pricep(in dollar) and the demandx(numberof miniature trucks) are related by the equation 6000−600p=x. The total cost for the sametoy manufacturer to producexminiature trucks can be modeled byC(x) = 8x+ 450.(a) (10 points) Express the pricepin terms of the demandx. Find the revenueR(x) if themanufacturer sellsxminiature trucks in a month and find the domain of this function.(b) (10 points) Graph the cost and revenue functions on the same coordinate system for 0≤x≤6000.(c) (10 points) What is the minimum number of trucks the toy manufacturer must sell tobreak even?(d) (10 points) FindP′(300) and interpret the result.(e) (10 points) What is the exact profit from the sale of the 301stminiature truck?The market for apple pies in the city of Ectenia is competitive and has the followingdemand schedule:Price Quantity Demanded$ 1 1,200 pies2 1,1003 1,0004 9005 8006 7007 6008 5009 40010 30011 20012 10013 0 ch producer in the market has fixed costs of $9 and the following marginal cost:Quantity Marginal Cost1 pie $ 22 43 64 85 106 12a. Compute each producer’s total cost and average total cost for 1 to 6 pies.b. The price of a pie is now $11. How many pies are sold? How many pies does eachproducer make? How many producers are there? How much profit does eachproducer earn?c. Is the situation described in part (b) a long-run equilibrium? Why or why not?d. Suppose that in the long run there is free entry and exit. How much profit does eachproducer earn in the long-run equilibrium? What is the market price? How many piesdoes each producer make? How many pies are sold in the market? How many pieproducers are operating?A computer company produces affordable, easyto-use home computer systems and has fixed costs of$250. The marginal cost of producing computers is $700for the first computer, $250 for the second, $300 for thethird, $350 for the fourth, $400 for the fifth, $450 for thesixth, and $500 for the seventh.a. Create a table that shows the company’s output,total cost, marginal cost, average cost, variablecost, and average variable cost.b. At what price is the zero-profit point? At whatprice is the shutdown point?c. If the company sells the computers for $500, is itmaking a profit or a loss? How big is the profitor loss? Sketch a graph with AC, MC, and AVCcurves to illustrate your answer and show theprofit or loss.d. If the firm sells the computers for $300, is itmaking a profit or a loss? How big is the profitor loss? Sketch a graph with AC, MC, and AVCcurves to illustrate your answer and show theprofit or loss.

- Suppose that the manager of a donut shop tellsyou that he sold 220 donuts today, for a total revenue of $220 and average revenue of $0.90. What’swrong with this story?Don't use chatgpt or any AI A profit-maximising firm in a competitive market is currently producing 1,000 units of output. It has average revenue of $50, average total cost of $40 and fixed cost of $10,000. a) What is its profit? b) What is its marginal cost? c) What is its average variable cost? Is the efficient scale of the firm more than, less than or exactly 1,000 units?Price1 Price2 Quantity 1 Quantity2 demand for a.cashews 7.50dollar per pound 6.00 dollar per pound 800 pounds per month 1,000 pounds per month 65 per year b.portable hard drive (1 terabyte) 80 dollar 120 dollar 75 per year 65 per year c.12-gauge copper wire 0.60 per lineal foot 0.45 per lineal foot 2,5000 lineal feet per week 5,000 lineal feet per week d.Toothpaste 2.00 dollar per tube 2.40 dollar per tube 10 tubes per moth 9 tubes per month Using the midpoint formula, calculate elasticity for each of the following changes in demand.

- What is the marginal revenue for the following: qty: 100, 200 Price:39750, 39500 Revenue:3975000, 7900000 Total Cost: 2000000,4000000 Profits: 1975000,3900000 Marginal Revenue ___?, ___? Suppose that managers at Honda are deciding how to price the new Honda Accord. The managers estimate that their total costs increase by $20,000 for each car they produce. They also estimate the demand curve they face; it is described by the equation: Q = -0.4 P + 16,000, where Q represents the quantity of Honda Accords they will sell and P represents the price they charge in US dollars. We can re-write that demand curve as: P = 40,000 - 2.5 Q. Take every possibly quantity that the managers might choose between 0 and 7,000 in units of 100. For each possible quantity, calculate the associated price the managers would need to charge, the revenue they would earn, and the total costs. You can then calculate profits for each level of quantity. Highlight the cell that contains the highest value of profit.…problem statement of MICROMAX during covid 19 period why was fall down in the demand of micromax mobile explain in briefThe market for apple pies in the city of Ectenia iscompetitive and has the following demand schedule:Price Quantity Demanded$1 1,200 pies2 1,1003 1,0004 9005 8006 7007 6008 5009 40010 30011 20012 10013 0Each producer in the market has fixed costs of $9 andthe following marginal cost schedule:Quantity Marginal Cost1 pie $ 22 43 64 85 106 12a. Compute each producer’s total cost andaverage total cost for each quantity from 1 to6 pies.b. The price of a pie is now $11. How many pies aresold? How many pies does each producer make?How many producers are there? How much profitdoes each producer earn?c. Is the situation described in part (b) a long-runequilibrium? Why or why not?d. Suppose that in the long run there is free entryand exit. How much profit does each producerearn in the long-run equilibrium? What isthe market price? How many pies does eachproducer make? How many pies are sold inthe market? How many pie producers areoperating?