(b) The following OLS regression results and White Heteroscedasticity Test are obtained from Eviews for the following regression model C = B% +BiYdu + B,W + B-IR + E. where C= real consumption expenditure Yd = real disposable personal income W = real wealth IR = real interest rate Dependent Variable: CONS Method: Least Squares Sample: 1947 2000 Included observations: 54 Variable Coefficient Std. Error t-Statistic Prob. -20.71811 12.83272 -1.614476 0.1127 YD 0.013758 0.002484 0.733991 53.34991 0.0000 0.035985 14.48563 0.0000

(b) The following OLS regression results and White Heteroscedasticity Test are obtained from Eviews for the following regression model C = B% +BiYdu + B,W + B-IR + E. where C= real consumption expenditure Yd = real disposable personal income W = real wealth IR = real interest rate Dependent Variable: CONS Method: Least Squares Sample: 1947 2000 Included observations: 54 Variable Coefficient Std. Error t-Statistic Prob. -20.71811 12.83272 -1.614476 0.1127 YD 0.013758 0.002484 0.733991 53.34991 0.0000 0.035985 14.48563 0.0000

Managerial Economics: Applications, Strategies and Tactics (MindTap Course List)

14th Edition

ISBN:9781305506381

Author:James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Chapter4A: Problems In Applying The Linear Regression Model

Section: Chapter Questions

Problem 1E

Related questions

Question

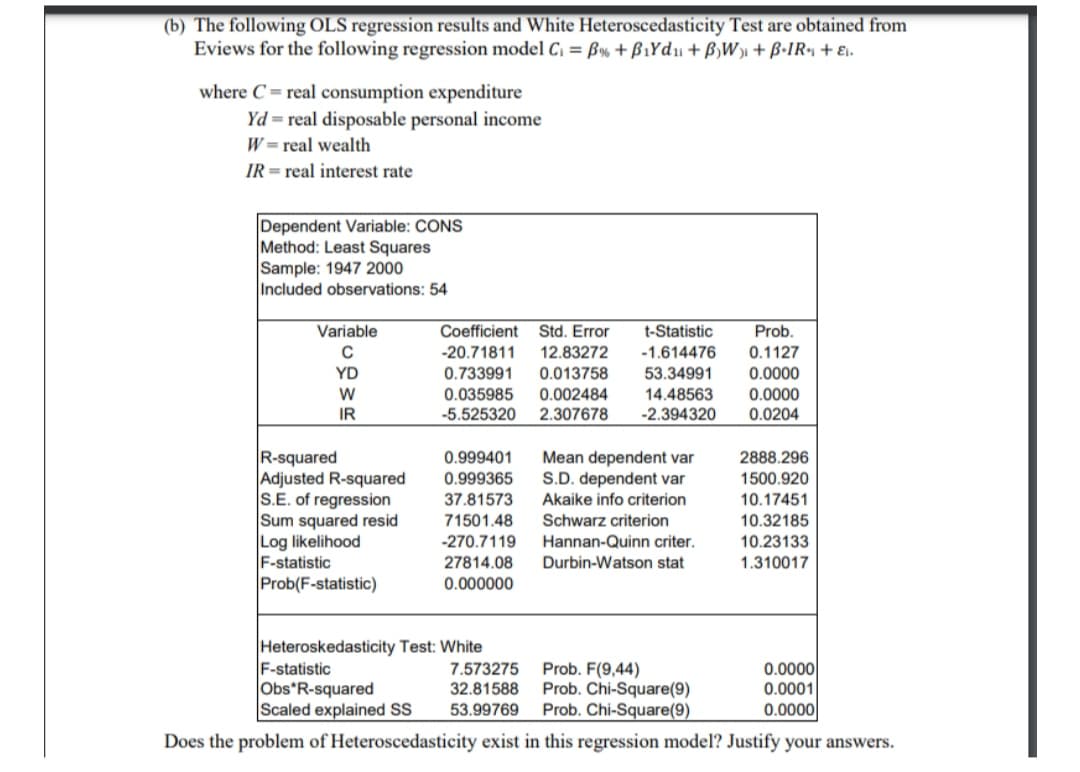

Transcribed Image Text:(b) The following OLS regression results and White Heteroscedasticity Test are obtained from

Eviews for the following regression model C, = B% +ß1Yd + B,Wi + B•IR + Ei.

where C = real consumption expenditure

Yd = real disposable personal income

W = real wealth

IR = real interest rate

Dependent Variable: CONS

Method: Least Squares

Sample: 1947 2000

Included observations: 54

Variable

Coefficient

Std. Error

t-Statistic

Prob.

C

-20.71811

12.83272

-1.614476

0.1127

YD

0.733991

0.013758

53.34991

0.0000

0.002484

2.307678

0.0000

0.0204

W

0.035985

14.48563

-2.394320

IR

-5.525320

R-squared

Adjusted R-squared

S.E. of regression

Sum squared resid

Log likelihood

F-statistic

Prob(F-statistic)

Mean dependent var

S.D. dependent var

Akaike info criterion

0.999401

2888.296

0.999365

1500.920

37.81573

71501.48

-270.7119

10.17451

Schwarz criterion

10.32185

Hannan-Quinn criter.

10.23133

27814.08

Durbin-Watson stat

1.310017

0.000000

Heteroskedasticity Test: White

F-statistic

Obs*R-squared

Scaled explained SS

Prob. F(9,44)

Prob. Chi-Square(9)

Prob. Chi-Square(9)

0.0000

0.0001|

0.0000

7.573275

32.81588

53.99769

Does the problem of Heteroscedasticity exist in this regression model? Justify your answers.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Managerial Economics: Applications, Strategies an…

Economics

ISBN:

9781305506381

Author:

James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:

Cengage Learning

Managerial Economics: Applications, Strategies an…

Economics

ISBN:

9781305506381

Author:

James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:

Cengage Learning