Bank overdraft 4.200 47,456 46,883 190,883 Net assets Сapials Аpel Ere 88,714 62,491 39,678 190,883 Inie Total capital Additional information Inie decided to retire from the business on 31* December, 2020 and Pee is admitted as a partner on that date. The following matters are agreed: i. Apel and Ere are to share profits in the same ratio as before, and Pee is to have the same share of profits as Ere. ii. The following assets were revalued: Premises for GH¢120,000 Plant for GH¢35,000 Inventory for GH¢54,179 iii. Provision is to be made for doubtful debts in the sum of GH¢3,000. iv. Goodwill is to be recorded in the books on the day Inie retires in the sum of GH¢42,000. The partners in the new firm do not wish to maintain a goodwill account so that amount is to be written back against the new partners' capital accounts. Inie is to take his car at its book vahue of GH¢3,900 in part payment, and the balance of all he is owed by the firm in cash except GH¢20,000 which he is willing to leave as a loan V. account. The partners in the new firm are to start on an equal footing so far as capital accounts are concerned. Pee is to contribute cash of GH¢82,091. vii. The original partner in the old firm who has the higher investment will draw out cash so that his capital account balances equal those of his new partners. vi.

Bank overdraft 4.200 47,456 46,883 190,883 Net assets Сapials Аpel Ere 88,714 62,491 39,678 190,883 Inie Total capital Additional information Inie decided to retire from the business on 31* December, 2020 and Pee is admitted as a partner on that date. The following matters are agreed: i. Apel and Ere are to share profits in the same ratio as before, and Pee is to have the same share of profits as Ere. ii. The following assets were revalued: Premises for GH¢120,000 Plant for GH¢35,000 Inventory for GH¢54,179 iii. Provision is to be made for doubtful debts in the sum of GH¢3,000. iv. Goodwill is to be recorded in the books on the day Inie retires in the sum of GH¢42,000. The partners in the new firm do not wish to maintain a goodwill account so that amount is to be written back against the new partners' capital accounts. Inie is to take his car at its book vahue of GH¢3,900 in part payment, and the balance of all he is owed by the firm in cash except GH¢20,000 which he is willing to leave as a loan V. account. The partners in the new firm are to start on an equal footing so far as capital accounts are concerned. Pee is to contribute cash of GH¢82,091. vii. The original partner in the old firm who has the higher investment will draw out cash so that his capital account balances equal those of his new partners. vi.

Chapter15: Partnership Accounting

Section: Chapter Questions

Problem 1PA: The partnership of Tatum and Brook shares profits and losses in a 60:40 ratio respectively after...

Related questions

Question

Required: prepare

a. Revaluation account

b.

c. Retiring partner's (Inie) account

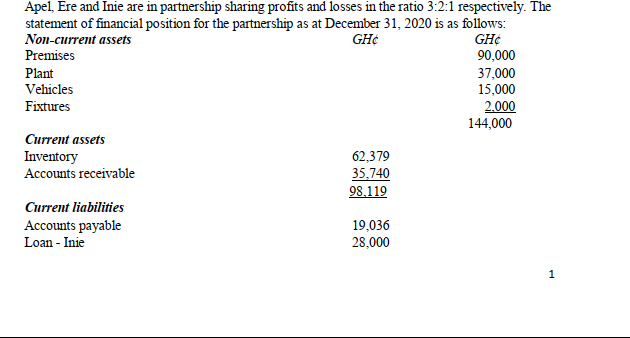

Transcribed Image Text:Apel, Ere and Inie are in partnership sharing profits and losses in the ratio 3:2:1 respectively. The

statement of financial position for the partnership as at December 31, 2020 is as follows:

Non-current assets

GH¢

90,000

GH¢

Premises

Plant

37,000

15,000

Vehicles

2.000

144,000

Fixtures

Current assets

Inventory

Accounts receivable

62,379

35,740

98.119

Current liabilities

Accounts payable

19,036

28,000

Loan - Inie

1

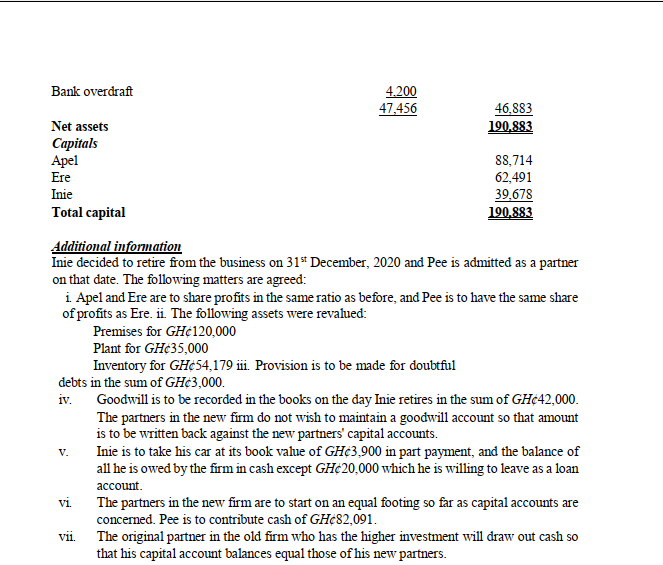

Transcribed Image Text:Bank overdraft

4.200

47,456

46,883

190,883

Net assets

Capitals

Apel

Ere

88,714

62,491

39,678

190,883

Inie

Total capital

Additional information

Inie decided to retire from the business on 31* December, 2020 and Pee is admitted as a partner

on that date. The following matters are agreed:

i Apel and Ere are to share profits in the same ratio as before, and Pee is to have the same share

of profits as Ere. ii. The following assets were revalued:

Premises for GH¢120,000

Plant for GH¢35,000

Inventory for GH¢54,179 ii. Provision is to be made for doubtful

debts in the sum of GH¢3,000.

iv.

Goodwill is to be recorded in the books on the day Inie retires in the sum of GH¢42,000.

The partners in the new firm do not wish to maintain a goodwill account so that amount

is to be written back against the new partners' capital accounts.

Inie is to take his car at its book value of GH¢3,900 in part payment, and the balance of

all he is owed by the firm in cash except GH¢20,000 which he is willing to leave as a loan

V.

account.

vi

The partners in the new firm are to start on an equal footing so far as capital accounts are

concerned. Pee is to contribute cash of GH¢82,091.

The original partner in the old firm who has the higher investment will draw out cash so

that his capital account balances equal those of his new partners.

vi

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 4 steps

Recommended textbooks for you

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning