Barbour Corporation, located in Buffalo, New York, is a retailer of high-tech products and is known for its excellent quality and innovation. Recently, the firm conducted a relevant cost analysis of one of its product lines that has only two products, T-1 and T-2. The sales for T-2 are decreasing and the purchase costs are increasing. The firm might drop T-2 and sell only T-1. Barbour allocates fixed costs to products on the basis of sales revenue. When the president of Barbour saw the income statements (see below), he agreed that T-2 should be dropped. If T-2 is dropped, sales of T-1 are expected to increase by 10 percent next year, but the firm's cost structure will remain the same. Sales Variable costs: Cost of goods sold Selling & administrative Contribution margin Fixed expenses: Fixed corporate costs Fixed selling and administrative Total fixed expenses Operating income T-1 $ 235,000 2. Required % increase in sales from T-1 3. Required % increase in sales from T-1 77,000 17,000 $ 141,000 67,000 19,000 $ 86,000 $ 55,000 a at T-2 $ 288,000 Required: 1. Find the expected change in annual operating income by dropping T-2 and selling only T-1. 2. By what percentage would sales from T-1 have to increase in order to make up the financial loss from dropping T-2? (Enter your answer as a percentage rounded to 2 decimal places (i.e. 0.1234 should be entered as 12.34).) 3. What is the required percentage increase in sales from T-1 to compensate for lost margin from T-2, if total fixed costs can be reduced by $50,000? (Enter your answer as a percentage rounded to 2 decimal places (i.e. 0.1234 should be entered as 12.34).) % 144,000 57,000 $ 87,000 82,000 28,000 $ 110,000 $ (23,000)

Barbour Corporation, located in Buffalo, New York, is a retailer of high-tech products and is known for its excellent quality and innovation. Recently, the firm conducted a relevant cost analysis of one of its product lines that has only two products, T-1 and T-2. The sales for T-2 are decreasing and the purchase costs are increasing. The firm might drop T-2 and sell only T-1. Barbour allocates fixed costs to products on the basis of sales revenue. When the president of Barbour saw the income statements (see below), he agreed that T-2 should be dropped. If T-2 is dropped, sales of T-1 are expected to increase by 10 percent next year, but the firm's cost structure will remain the same. Sales Variable costs: Cost of goods sold Selling & administrative Contribution margin Fixed expenses: Fixed corporate costs Fixed selling and administrative Total fixed expenses Operating income T-1 $ 235,000 2. Required % increase in sales from T-1 3. Required % increase in sales from T-1 77,000 17,000 $ 141,000 67,000 19,000 $ 86,000 $ 55,000 a at T-2 $ 288,000 Required: 1. Find the expected change in annual operating income by dropping T-2 and selling only T-1. 2. By what percentage would sales from T-1 have to increase in order to make up the financial loss from dropping T-2? (Enter your answer as a percentage rounded to 2 decimal places (i.e. 0.1234 should be entered as 12.34).) 3. What is the required percentage increase in sales from T-1 to compensate for lost margin from T-2, if total fixed costs can be reduced by $50,000? (Enter your answer as a percentage rounded to 2 decimal places (i.e. 0.1234 should be entered as 12.34).) % 144,000 57,000 $ 87,000 82,000 28,000 $ 110,000 $ (23,000)

Chapter3: Cost-volume-profit Analysis

Section: Chapter Questions

Problem 3TP: As a manager, you have to choose between two options for new production equipment. Machine A will...

Related questions

Question

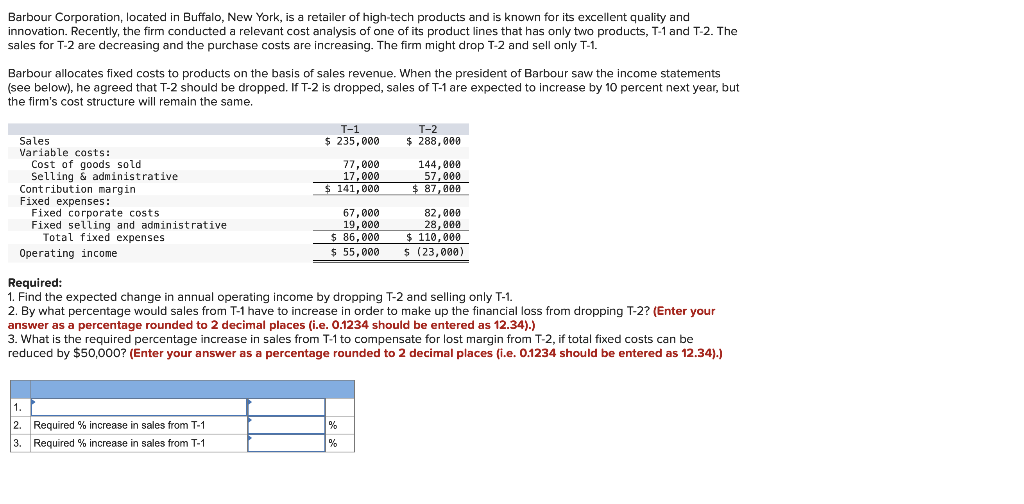

Transcribed Image Text:Barbour Corporation, located in Buffalo, New York, is a retailer of high-tech products and is known for its excellent quality and

innovation. Recently, the firm conducted a relevant cost analysis of one of its product lines that has only two products, T-1 and T-2. The

sales for T-2 are decreasing and the purchase costs are increasing. The firm might drop T-2 and sell only T-1.

Barbour allocates fixed costs to products on the basis of sales revenue. When the president of Barbour saw the income statements

(see below), he agreed that T-2 should be dropped. If T-2 is dropped, sales of T-1 are expected to increase by 10 percent next year, but

the firm's cost structure will remain the same.

Sales

Variable costs:

Cost of goods sold

Selling & administrative

Contribution margin

Fixed expenses:

Fixed corporate costs

Fixed selling and administrative

Total fixed expenses

Operating income

T-1

$ 235,000

77,000

17,000

$ 141,000

1.

2. Required % increase in sales from T-1

3. Required % increase in sales from T-1

67,000

19,000

$ 86,000

$ 55,000

T-2

$ 288,000

144,000

57,000

$ 87,000

Required:

1. Find the expected change in annual operating income by dropping T-2 and selling only T-1.

2. By what percentage would sales from T-1 have to increase in order to make up the financial loss from dropping T-2? (Enter your

answer as a percentage rounded to 2 decimal places (i.e. 0.1234 should be entered as 12.34).)

%

%

82,000

28,000

$ 110,000

$ (23,000)

3. What is the required percentage increase in sales from T-1 to compensate for lost margin from T-2, if total fixed costs can be

reduced by $50,000? (Enter your answer as a percentage rounded to 2 decimal places (i.e. 0.1234 should be entered as 12.34).)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning

Excel Applications for Accounting Principles

Accounting

ISBN:

9781111581565

Author:

Gaylord N. Smith

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning