Concept explainers

Videos

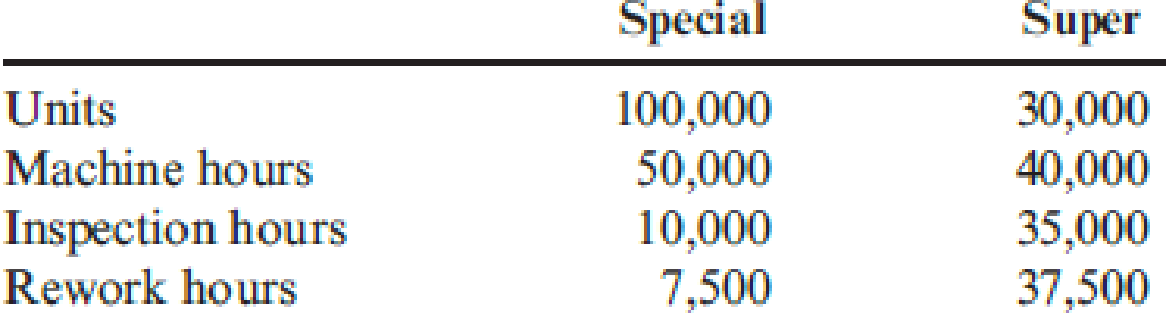

Harvey Company produces two models of blenders: the “Super Model” (priced at $400) and the “Special Model” (priced at $200). Recently, Harvey has been losing market share with its Special Model because of competitors offering blenders with the same quality and features but at a lower price. A careful market study revealed that if Harvey could reduce the price of its Special Model to $180, it would regain its former share of the market. Management, however, is convinced that any price reduction must be accompanied by a cost reduction of the same amount so that per-unit profitability is not affected. Earl Wise, company controller, has indicated that poor overhead costing assignments may be distorting management’s view of each product’s cost and, therefore, the ability to know how to set selling prices. Earl has identified the following overhead activities: machining, inspection, and rework. The three activities, their costs, and practical capacities are as follows:

The consumption patterns of the two products are as follows:

Harvey assigns overhead costs to the two products using a plantwide rate based on machine hours.

Required:

- 1. Calculate the unit overhead cost of the Special Model using machine hours to assign overhead costs. Now, repeat the calculation using ABC to assign overhead costs. Did improving the accuracy of cost assignments solve Harvey’s competitive problem? What did it reveal?

- 2. Now, assume that in addition to improving the accuracy of cost assignments, Earl observes that defective supplier components are the root cause of both the inspection and rework activities. Suppose further that Harvey has found a new supplier that provides higher-quality components such that inspection and rework costs are reduced by 50 percent. Now, calculate the cost of the Special Model (assuming that inspection and rework times are also reduced by 50 percent) using ABC. The relative consumption patterns also remain the same. Comment on the difference between ABC and ABM.

Trending nowThis is a popular solution!

Chapter 12 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Maxwell Company produces a variety of kitchen appliances, including cooking ranges and dishwashers. Over the past several years, competition has intensified. In order to maintainand perhaps increaseits market share, Maxwells management decided that the overall quality of its products had to be increased. Furthermore, costs needed to be reduced so that the selling prices of its products could be reduced. After some investigation, Maxwell concluded that many of its problems could be traced to the unreliability of the parts that were purchased from outside suppliers. Many of these components failed to work as intended, causing performance problems. Over the years, the company had increased its inspection activity of the final products. If a problem could be detected internally, then it was usually possible to rework the appliance so that the desired performance was achieved. Management also had increased its warranty coverage; warranty work had been increasing over the years. David Haight, president of Maxwell Company, called a meeting with his executive committee. Lee Linsenmeyer, chief engineer; Kit Applegate, controller; and Jeannie Mitchell, purchasing manager, were all in attendance. How to improve the companys competitive position was the meetings topic. The conversation of the meeting was recorded as seen on the following page: DAVID: We need to find a way to improve the quality of our products and at the same time reduce costs. Lee, you said that you have done some research in this area. Would you share your findings? LEE: As you know, a major source of our quality problems relates to the poor quality of the parts we acquire from the outside. We have a lot of different parts, and this adds to the complexity of the problem. What I thought would be helpful would be to redesign our products so that they can use as many interchangeable parts as possible. This will cut down the number of different parts, make it easier to inspect, and cheaper to repair when it comes to warranty work. My engineering staff has already come up with some new designs that will do this for us. JEANNIE: I like this idea. It will simplify the purchasing activity significantly. With fewer parts, I can envision some significant savings for my area. Lee has shown me the designs so I know exactly what parts would be needed. I also have a suggestion. We need to embark on a supplier evaluation program. We have too many suppliers. By reducing the number of different parts, we will need fewer suppliers. And we really dont need to use all the suppliers that produce the parts demanded by the new designs. We should pick suppliers that will work with us and provide the quality of parts that we need. I have done some preliminary research and have identified five suppliers that seem willing to work with us and assure us of the quality we need. Lee may need to send some of his engineers into their plants to make sure that they can do what they are claiming. DAVID: This sounds promising. Kit, can you look over the proposals and their estimates and give us some idea if this approach will save us any money? And if so, how much can we expect to save? KIT: Actually, I am ahead of the game here. Lee and Jeannie have both been in contact with me and have provided me with some estimates on how these actions would affect different activities. I have prepared a handout that includes an activity table revealing what I think are the key activities affected. I have also assembled some tentative information about activity costs. The table gives the current demand and the expected demand after the changes are implemented. With this information, we should be able to assess the expected cost savings. Additionally, the following activity cost data are provided: Purchasing parts: Variable activity cost: 30 per part number; 20 salaried clerks, each earning a 45,000 annual salary. Each clerk is capable of processing orders associated with 100 part numbers. Inspecting parts: Twenty-five inspectors, each earning a salary of 40,000 per year. Each inspector is capable of 2,000 hours of inspection. Reworking products: Variable activity cost: 25 per unit reworked (labor and parts). Warranty: Twenty repair agents, each paid a salary of 35,000 per year. Each repair agent is capable of repairing 500 units per year. Variable activity costs: 15 per product repaired. Required: 1. Compute the total savings possible as reflected by Kits handout. Assume that resource spending is reduced where possible. 2. Explain how redesign and supplier evaluation are linked to the savings computed in Requirement 1. Discuss the importance of recognizing and exploiting internal and external linkages. 3. Identify the organizational and operational activities involved in the strategy being considered by Maxwell Company. What is the relationship between organizational and operational activities?arrow_forwardAt the beginning of the last quarter of 20x1, Youngston, Inc., a consumer products firm, hired Maria Carrillo to take over one of its divisions. The division manufactured small home appliances and was struggling to survive in a very competitive market. Maria immediately requested a projected income statement for 20x1. In response, the controller provided the following statement: After some investigation, Maria soon realized that the products being produced had a serious problem with quality. She once again requested a special study by the controllers office to supply a report on the level of quality costs. By the middle of November, Maria received the following report from the controller: Maria was surprised at the level of quality costs. They represented 30 percent of sales, which was certainly excessive. She knew that the division had to produce high-quality products to survive. The number of defective units produced needed to be reduced dramatically. Thus, Maria decided to pursue a quality-driven turnaround strategy. Revenue growth and cost reduction could both be achieved if quality could be improved. By growing revenues and decreasing costs, profitability could be increased. After meeting with the managers of production, marketing, purchasing, and human resources, Maria made the following decisions, effective immediately (end of November 20x1): a. More will be invested in employee training. Workers will be trained to detect quality problems and empowered to make improvements. Workers will be allowed a bonus of 10 percent of any cost savings produced by their suggested improvements. b. Two design engineers will be hired immediately, with expectations of hiring one or two more within a year. These engineers will be in charge of redesigning processes and products with the objective of improving quality. They will also be given the responsibility of working with selected suppliers to help improve the quality of their products and processes. Design engineers were considered a strategic necessity. c. Implement a new process: evaluation and selection of suppliers. This new process has the objective of selecting a group of suppliers that are willing and capable of providing nondefective components. d. Effective immediately, the division will begin inspecting purchased components. According to production, many of the quality problems are caused by defective components purchased from outside suppliers. Incoming inspection is viewed as a transitional activity. Once the division has developed a group of suppliers capable of delivering nondefective components, this activity will be eliminated. e. Within three years, the goal is to produce products with a defect rate less than 0.10 percent. By reducing the defect rate to this level, marketing is confident that market share will increase by at least 50 percent (as a consequence of increased customer satisfaction). Products with better quality will help establish an improved product image and reputation, allowing the division to capture new customers and increase market share. f. Accounting will be given the charge to install a quality information reporting system. Daily reports on operational quality data (e.g., percentage of defective units), weekly updates of trend graphs (posted throughout the division), and quarterly cost reports are the types of information required. g. To help direct the improvements in quality activities, kaizen costing is to be implemented. For example, for the year 20x1, a kaizen standard of 6 percent of the selling price per unit was set for rework costs, a 25 percent reduction from the current actual cost. To ensure that the quality improvements were directed and translated into concrete financial outcomes, Maria also began to implement a Balanced Scorecard for the division. By the end of 20x2, progress was being made. Sales had increased to 26,000,000, and the kaizen improvements were meeting or beating expectations. For example, rework costs had dropped to 1,500,000. At the end of 20x3, two years after the turnaround quality strategy was implemented, Maria received the following quality cost report: Maria also received an income statement for 20x3: Maria was pleased with the outcomes. Revenues had grown, and costs had been reduced by at least as much as she had projected for the two-year period. Growth next year should be even greater as she was beginning to observe a favorable effect from the higher-quality products. Also, further quality cost reductions should materialize as incoming inspections were showing much higher-quality purchased components. Required: 1. Identify the strategic objectives, classified by the Balanced Scorecard perspective. Next, suggest measures for each objective. 2. Using the results from Requirement 1, describe Marias strategy using a series of if-then statements. Next, prepare a strategy map. 3. Explain how you would evaluate the success of the quality-driven turnaround strategy. What additional information would you like to have for this evaluation? 4. Explain why Maria felt that the Balanced Scorecard would increase the likelihood that the turnaround strategy would actually produce good financial outcomes. 5. Advise Maria on how to encourage her employees to align their actions and behavior with the turnaround strategy.arrow_forwardBienestar, Inc., has two plants that manufacture a line of wheelchairs. One is located in Kansas City, and the other in Tulsa. Each plant is set up as a profit center. During the past year, both plants sold their tilt wheelchair model for 1,620. Sales volume averages 20,000 units per year in each plant. Recently, the Kansas City plant reduced the price of the tilt model to 1,440. Discussion with the Kansas City manager revealed that the price reduction was possible because the plant had reduced its manufacturing and selling costs by reducing what was called non-value-added costs. The Kansas City manufacturing and selling costs for the tilt model were 1,260 per unit. The Kansas City manager offered to loan the Tulsa plant his cost accounting manager to help it achieve similar results. The Tulsa plant manager readily agreed, knowing that his plant must keep pacenot only with the Kansas City plant but also with competitors. A local competitor had also reduced its price on a similar model, and Tulsas marketing manager had indicated that the price must be matched or sales would drop dramatically. In fact, the marketing manager suggested that if the price were dropped to 1,404 by the end of the year, the plant could expand its share of the market by 20 percent. The plant manager agreed but insisted that the current profit per unit must be maintained. He also wants to know if the plant can at least match the 1,260 per-unit cost of the Kansas City plant and if the plant can achieve the cost reduction using the approach of the Kansas City plant. The plant controller and the Kansas City cost accounting manager have assembled the following data for the most recent year. The actual cost of inputs, their value-added (ideal) quantity levels, and the actual quantity levels are provided (for production of 20,000 units). Assume there is no difference between actual prices of activity units and standard prices. Required: 1. Calculate the target cost for expanding the Tulsa plants market share by 20 percent, assuming that the per-unit profitability is maintained as requested by the plant manager. 2. Calculate the non-value-added cost per unit. Assuming that non-value-added costs can be reduced to zero, can the Tulsa plant match the Kansas City per-unit cost? Can the target cost for expanding market share be achieved? What actions would you take if you were the plant manager? 3. Describe the role that benchmarking played in the effort of the Tulsa plant to protect and improve its competitive position.arrow_forward

- Danna Martin, president of Mays Electronics, was concerned about the end-of-the year marketing report that she had just received. According to Larry Savage, marketing manager, a price decrease for the coming year was again needed to maintain the companys annual sales volume of integrated circuit boards (CBs). This would make a bad situation worse. The current selling price of 18 per unit was producing a 2-per-unit profithalf the customary 4-per-unit profit. Foreign competitors kept reducing their prices. To match the latest reduction would reduce the price from 18 to 14. This would put the price below the cost to produce and sell it. How could these firms sell for such a low price? Determined to find out if there were problems with the companys operations, Danna decided to hire a consultant to evaluate the way in which the CBs were produced and sold. After two weeks, the consultant had identified the following activities and costs: The consultant indicated that some preliminary activity analysis shows that per-unit costs can be reduced by at least 7. Since the marketing manager had indicated that the market share (sales volume) for the boards could be increased by 50% if the price could be reduced to 12, Danna became quite excited. Required: 1. CONCEPTUAL CONNECTION What is activity-based management? What phases of activity analysis did the consultant provide? What else remains to be done? 2. CONCEPTUAL CONNECTION Identify as many nonvalue-added costs as possible. Compute the cost savings per unit that would be realized if these costs were eliminated. Was the consultant correct in the preliminary cost reduction assessment? Discuss actions that the company can take to reduce or eliminate the nonvalue-added activities. 3. Compute the unit cost required to maintain current market share, while earning a profit of 4 per unit. Now compute the unit cost required to expand sales by 50%, assuming a per-unit profit of 4. How much cost reduction would be required to achieve each unit cost? 4. Assume that further activity analysis revealed the following: switching to automated insertion would save 60,000 of engineering support and 90,000 of direct labor. Now, what is the total potential cost reduction per unit available from activity analysis? With these additional reductions, can Mays achieve the unit cost to maintain current sales? To increase it by 50%? What form of activity analysis is this: reduction, sharing, elimination, or selection? 5. CONCEPTUAL CONNECTION Calculate income based on current sales, prices, and costs. Then calculate the income by using a 14 price and a 12 price, assuming that the maximum cost reduction possible is achieved (including Requirement 4s reduction). What price should be selected?arrow_forwardGalveston Pump Corporation is considering implementing a JIT production system. The new system would reduce current average inventory levels of $2,000,000 by 75%, but it would require a much greater dependency on the company’s core suppliers for on-time deliveries and high-quality inputs. The company’s operations manager, Frank Griswold, is opposed to the idea of a new JIT system because he is concerned that the new system (a) will be too costly to manage; (b) will result in too many stockouts; and (c) will lead to the layoff of his employees, several of whom are currently managing inventory. He believes that these layoffs will affect the morale of his entire production department. The management accountant, Bonnie Barrett, is in favor of the new system because of its likely cost savings. Frank wants Bonnie to rework the numbers because he is concerned that top management will give more weight to financial factors and not give due consideration to nonfinancial factors such as employee…arrow_forwardGalveston Pump Corporation is considering implementing a JIT production system. The new system would reduce current average inventory levels of $2,000,000 by 75%, but it would require a much greater dependency on the company’s core suppliers for on-time deliveries and high-quality inputs. The company’s operations manager, Frank Griswold, is opposed to the idea of a new JIT system because he is concerned that the new system (a) will be too costly to manage; (b) will result in too many stockouts; and (c) will lead to the layoff of his employees, several of whom are currently managing inventory. He believes that these layoffs will affect the morale of his entire production department. The management accountant, Bonnie Barrett, is in favor of the new system because of its likely cost savings. Frank wants Bonnie to rework the numbers because he is concerned that top management will give more weight to financial factors and not give due consideration to nonfinancial factors such as employee…arrow_forward

- Galveston Pump Corporation is considering implementing a JIT production system. The new system would reduce current average inventory levels of $2,000,000 by 75%, but it would require a much greater dependency on the company’s core suppliers for on-time deliveries and high-quality inputs. The company’s operations manager, Frank Griswold, is opposed to the idea of a new JIT system because he is concerned that the new system (a) will be too costly to manage; (b) will result in too many stockouts; and (c) will lead to the layoff of his employees, several of whom are currently managing inventory. He believes that these layoffs will affect the morale of his entire production department. The management accountant, Bonnie Barrett, is in favor of the new system because of its likely cost savings. Frank wants Bonnie to rework the numbers because he is concerned that top management will give more weight to financial factors and not give due consideration to nonfinancial factors such as employee…arrow_forwardIn 20X1, LLHC sold for $2,400 per ton, making it one of the most profitable products. A similar examination of some of the other low-volume products revealed that they also had very respectable profit margins. Unfortunately, the performance of the high-volume products was less impressive, with many showing losses or very low-profit margins. This situation led Ryan Chesser to call a meeting with his marketing vice president, Jennifer Woodruff, and his controller, Kaylin Penn. Ryan: The above-average profitability of our low-volume specialty products and the poor profit performance of our high-volume products make me believe that we should switch our marketing emphasis to the low-volume line. Perhaps we should drop some of our high-volume products, particularly those showing a loss. Jennifer: I’m not convinced that solution is the right one. I know our high-volume products are of high quality, and I’m convinced that we are as efficient in our production as other firms. I think that…arrow_forwardJW Computers is a small firm focused on the assembly and sale of custom computers. The firm is facing stiff competition from low-priced alternatives, and is looking at various solutions to remain competitive and profitable. Current financials for the firm are shown in the table below. In the 1st option, marketing will increase sales by 50%. The 2nd option is Vendor (Supplier) changes, which would result in a decrease of 10% in the cost of inputs. Finally, there is the 3rd OM option, which would reduce production costs by 25%. a. Which of the 3 options would you recommend to the firm if it can only pursue one option? b. What is the new profit for the 1st option? c. What is the new profit for the 2nd option?arrow_forward

- Peterson Corporation is considering implementing a JIT production system. The new system would reduce current average inventory levels of $2,000,000 by 75%, but it would require a much greater dependency on the company’s core suppliers for on-time deliveries and high-quality inputs. The company’s operations manager, John Leung, is opposed to the idea of a new JIT system. He is concerned that the new system (a) will be too costly to manage; (b) will result in too many stock outs; and (c) will lead to the layoff of his employees, several of whom are currently managing inventory. He believes that these layoffs will affect the morale of his entire production department. The management accountant, Susan Chow, is in favour of the new system, due to the likely result in cost savings. John wants Susan to revise her cost saving estimation because he is concerned that top management will give more weight to financial factors and not give due consideration to nonfinancial factors such as employee…arrow_forwardThe Monroe Forging Company sells a corrugated steel product to the Standard Manufacturing Company and is in competition on such sales with other suppliers of the Standard Manufacturing Co. The vice president of sales of Monroe Forging Co. believes that by reducing the price of the product, a 40% increase in the volume of units sold to the Standard Manufacturing Co. could be secured. As the manager of the cost and analysis department, you have been asked to analyze the proposal of the vice president and submit your recommendations as to whether it is financially beneficial to the Monroe Forging Co. You are specifically requested to determine the following: (a) Net profit or loss based on the pricing proposal. (b) Unit sales volume under the proposed price that is required to make the same $40,000 profit that is now earned at the current price and unit sales volume. Use the following data in your analysis:arrow_forwardTool Industries manufactures large workbenches for industrial use. Sam Hartnet, the Vice President for marketing at Tool Industries, concluded from market analysis that sales were dwindling for Tool's workbenches due to aggressive pricing by competitors. Tool's workbench sells for $1,440 whereas the competition's comparable workbench sells for $1,300. Sam determined that a price drop to $1,300 would be necessary to protect its market share and maintain an annual sales level of 13,600 workbenches. Cost data based on sales of 13,600 workbenches: Budgeted Quantity Actual Quantity Actual Cost Direct materials (pounds) 178,000 171,000 $ 3,453,000 Direct labor (hours) 74,000 73,000 826,500 Machine setups (number of setups) 1,200 1,000 253,000 Mechanical assembly (machine hours) 29,400 282,750 3,756,000 The current cost per unit is (rounded to the nearest whole dollar): Multiple Choice $560. $495. $437. $609. $417.arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning