Concept explainers

Videos

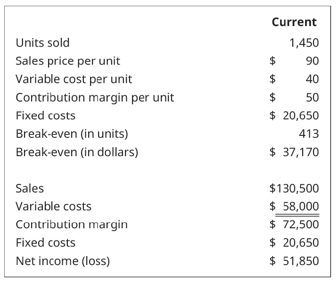

Baghdad Company produces a single product. They have recently received the result of a market survey that indicates that they can increase the retail price of their product by 10% without losing customers or market share. All other costs will remain unchanged. If they enact the 10% price increase, what will be their new break-even point in units and dollars? Their most recent CVP analysis is:

Want to see the full answer?

Check out a sample textbook solution

Chapter 3 Solutions

Principles of Accounting Volume 2

Additional Business Textbook Solutions

Intermediate Accounting

Horngren's Financial & Managerial Accounting, The Financial Chapters (Book & Access Card)

Financial Accounting, Student Value Edition (4th Edition)

Intermediate Accounting (2nd Edition)

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Financial Accounting (12th Edition) (What's New in Accounting)

- Marchete Company produces a single product. They have recently received the results of a market survey that indicates that they can increase the retail price of their product by 8% without losing customers or market share. All other costs will remain unchanged. Their most recent CVP analysis is shown. If they enact the 8% price increase, what will be their new break-even point in units and dollars?arrow_forwardSchylar Pharmaceuticals, Inc., plans to sell 130,000 units of antibiotic at an average price of 22 each in the coming year. Total variable costs equal 1,086,800. Total fixed costs equal 8,000,000. (Round all ratios to four significant digits, and round all dollar amounts to the nearest dollar.) Required: 1. What is the contribution margin per unit? What is the contribution margin ratio? 2. Calculate the sales revenue needed to break even. 3. Calculate the sales revenue needed to achieve a target profit of 245,000. 4. What if the average price per unit increased to 23.50? Recalculate: a. Contribution margin per unit b. Contribution margin ratio (rounded to four decimal places) c. Sales revenue needed to break even d. Sales revenue needed to achieve a target profit of 245,000arrow_forwardBoxer Production, Inc., is in the process of considering a flexible manufacturing system that will help the company react more swiftly to customer needs. The controller, Mick Morrell, estimated that the system will have a 10-year life and a required return of 10% with a net present value of negative $500,000. Nevertheless, he acknowledges that he did not quantify the potential sales increases that might result from this improvement on the issue of on-time delivery, because it was too difficult to quantify. If there is a general agreement that qualitative factors may offer an additional net cash flow of $150,000 per year, how should Boxer proceed with this Investment?arrow_forward

- Faldo Company produces a single product. The projected income statement for the coming year, based on sales of 200,000 units, is as follows: Required: 1. Compute the unit contribution margin and the units that must be sold to break even. Suppose that 30,000 units are sold above the break-even point. What is the profit? 2. Compute the contribution margin ratio and the break-even point in dollars. Suppose that revenues are 200,000 greater than expected. What would the total profit be? 3. Compute the margin of safety in sales revenue. 4. Compute the operating leverage. Compute the new profit level if sales are 20 percent higher than expected. 5. How many units must be sold to earn a profit equal to 10 percent of sales? 6. Assume the income tax rate is 40 percent. How many units must be sold to earn an after-tax profit of 180,000?arrow_forwardMarshall s target margin of safety be in units and dollars if they required a $14,000 margin of safety?arrow_forwardDelta Co. sells a product for $150 per unit. The variable cost per unit is $90 and fixed costs are $15,250. Delta Co.s tax rate is 36% and the company wants to earn $44,000 after taxes. What would be Deltas desired pre-tax income? What would be break-even point in units to reach the income goal of $44,000 after taxes? What would be break-even point in sales dollars to reach the income goal of $44000 after taxes? Create a contribution margin income statement to show that the break-even point calculated in B, generates the desired after-tax income.arrow_forward

- The president of Poleski would like to know the effect that each of the following suggestions for improving performance would have on contribution margin per unit, sales needed to break even, and projected net income for next year. Each change should be considered independently. Reset the Data Section to its original values after each suggestion is analyzed. Fill in the table following the suggestions with the results of your analysis. a. The president suggests cutting the products price. Since the market is relatively sensitive to price, . . . a 10% cut in price ought to generate a 30% increase in sales (to 156,000 units). How can you lose? b. The sales manager feels that putting all sales personnel on straight commission would help. This would eliminate 77,000 in fixed sales salaries expense. Variable sales commissions would increase to 2.00 per unit. This move would also increase sales volume by 30%. c. Poleskis head of product engineering wants to redesign the package for the product. This will cut 1.00 per unit from direct materials and 0.50 per unit from direct labor, but will increase fixed factory overhead by 100,000 for additional depreciation on the new packaging machine. The package redesign would not affect sales volume. d. The firms consumer marketing manager suggests undertaking a new advertising campaign on Facebook. This would cost 30,000 more than is currently planned for advertising but would be expected to increase sales volume by 30%. e. The production superintendent suggests raising quality and raising price. This will increase direct materials by 1.00 per unit, direct labor by 0.50 per unit, and fixed factory overhead by 110,000. With improved quality, . . . raise the price to 18.50 and advertise the heck out of it. If you double your current planned advertising, Ill bet you can increase your sales volume by 30%.arrow_forwardSuppose you are analyzing a firm that is successfully executing a strategy that differentiates its products from those of its competitors. Because of this strategy, you project that next year the firm will generate 6.0% revenue growth from price increases and 3.0% revenue growth from sales volume increases. Assume that the firms production cost structure involves strictly variable costs. (That is, the cost to produce each unit of product remains the same.) Should you project that the firms gross profit will increase next year? If you project that the gross profit will increase, is the increase a result of volume growth, price growth, or both? Should you project that the firms gross profit margin (gross profit divided by sales) will increase next year? If you project that the gross profit margin will increase, is the increase a result of volume growth, price growth, or both?arrow_forwardFlanders Manufacturing is considering purchasing a new machine that will reduce variable costs per part produced by $0.15. The machine will increase fixed costs by $18,250 per year. The information they will use to consider these changes is shown here.arrow_forward

- Nico Parts, Inc., produces electronic products with short life cycles (of less than two years). Development has to be rapid, and the profitability of the products is tied strongly to the ability to find designs that will keep production and logistics costs low. Recently, management has also decided that post-purchase costs are important in design decisions. Last month, a proposal for a new product was presented to management. The total market was projected at 200,000 units (for the two-year period). The proposed selling price was 130 per unit. At this price, market share was expected to be 25 percent. The manufacturing and logistics costs were estimated to be 120 per unit. Upon reviewing the projected figures, Brian Metcalf, president of Nico, called in his chief design engineer, Mark Williams, and his marketing manager, Cathy McCourt. The following conversation was recorded: BRIAN: Mark, as you know, we agreed that a profit of 15 per unit is needed for this new product. Also, as I look at the projected market share, 25 percent isnt acceptable. Total profits need to be increased. Cathy, what suggestions do you have? CATHY: Simple. Decrease the selling price to 125 and we expand our market share to 35 percent. To increase total profits, however, we need some cost reductions as well. BRIAN: Youre right. However, keep in mind that I do not want to earn a profit that is less than 15 per unit. MARK: Does that 15 per unit factor in preproduction costs? You know we have already spent 100,000 on developing this product. To lower costs will require more expenditure on development. BRIAN: Good point. No, the projected cost of 120 does not include the 100,000 we have already spent. I do want a design that will provide a 15-per-unit profit, including consideration of preproduction costs. CATHY: I might mention that post-purchase costs are important as well. The current design will impose about 10 per unit for using, maintaining, and disposing our product. Thats about the same as our competitors. If we can reduce that cost to about 5 per unit by designing a better product, we could probably capture about 50 percent of the market. I have just completed a marketing survey at Marks request and have found out that the current design has two features not valued by potential customers. These two features have a projected cost of 6 per unit. However, the price consumers are willing to pay for the product is the same with or without the features. Required: 1. Calculate the target cost associated with the initial 25 percent market share. Does the initial design meet this target? Now calculate the total life-cycle profit that the current (initial) design offers (including preproduction costs). 2. Assume that the two features that are apparently not valued by consumers will be eliminated. Also assume that the selling price is lowered to 125. a. Calculate the target cost for the 125 price and 35 percent market share. b. How much more cost reduction is needed? c. What are the total life-cycle profits now projected for the new product? d. Describe the three general approaches that Nico can take to reduce the projected cost to this new target. Of the three approaches, which is likely to produce the most reduction? 3. Suppose that the Engineering Department has two new designs: Design A and Design B. Both designs eliminate the two nonvalued features. Both designs also reduce production and logistics costs by an additional 8 per unit. Design A, however, leaves post-purchase costs at 10 per unit, while Design B reduces post-purchase costs to 4 per unit. Developing and testing Design A costs an additional 150,000, while Design B costs an additional 300,000. Assuming a price of 125, calculate the total life-cycle profits under each design. Which would you choose? Explain. What if the design you chose cost an additional 500,000 instead of 150,000 or 300,000? Would this have changed your decision? 4. Refer to Requirement 3. For every extra dollar spent on preproduction activities, how much benefit was generated? What does this say about the importance of knowing the linkages between preproduction activities and later activities?arrow_forwardA company has prepared the following statistics regarding its production and sales at different capacity levels. Total costs: 1. At what point is break-even reached in sales dollars? In units? (Hint: Use the capacity level to determine the number of units.) 2. If the company is operating at 60% capacity, should it accept an offer from a customer to buy 10,000 units at 3 per unit?arrow_forwardHarvey Company produces two models of blenders: the Super Model (priced at 400) and the Special Model (priced at 200). Recently, Harvey has been losing market share with its Special Model because of competitors offering blenders with the same quality and features but at a lower price. A careful market study revealed that if Harvey could reduce the price of its Special Model to 180, it would regain its former share of the market. Management, however, is convinced that any price reduction must be accompanied by a cost reduction of the same amount so that per-unit profitability is not affected. Earl Wise, company controller, has indicated that poor overhead costing assignments may be distorting managements view of each products cost and, therefore, the ability to know how to set selling prices. Earl has identified the following overhead activities: machining, inspection, and rework. The three activities, their costs, and practical capacities are as follows: The consumption patterns of the two products are as follows: Harvey assigns overhead costs to the two products using a plantwide rate based on machine hours. Required: 1. Calculate the unit overhead cost of the Special Model using machine hours to assign overhead costs. Now, repeat the calculation using ABC to assign overhead costs. Did improving the accuracy of cost assignments solve Harveys competitive problem? What did it reveal? 2. Now, assume that in addition to improving the accuracy of cost assignments, Earl observes that defective supplier components are the root cause of both the inspection and rework activities. Suppose further that Harvey has found a new supplier that provides higher-quality components such that inspection and rework costs are reduced by 50 percent. Now, calculate the cost of the Special Model (assuming that inspection and rework times are also reduced by 50 percent) using ABC. The relative consumption patterns also remain the same. Comment on the difference between ABC and ABM.arrow_forward

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning