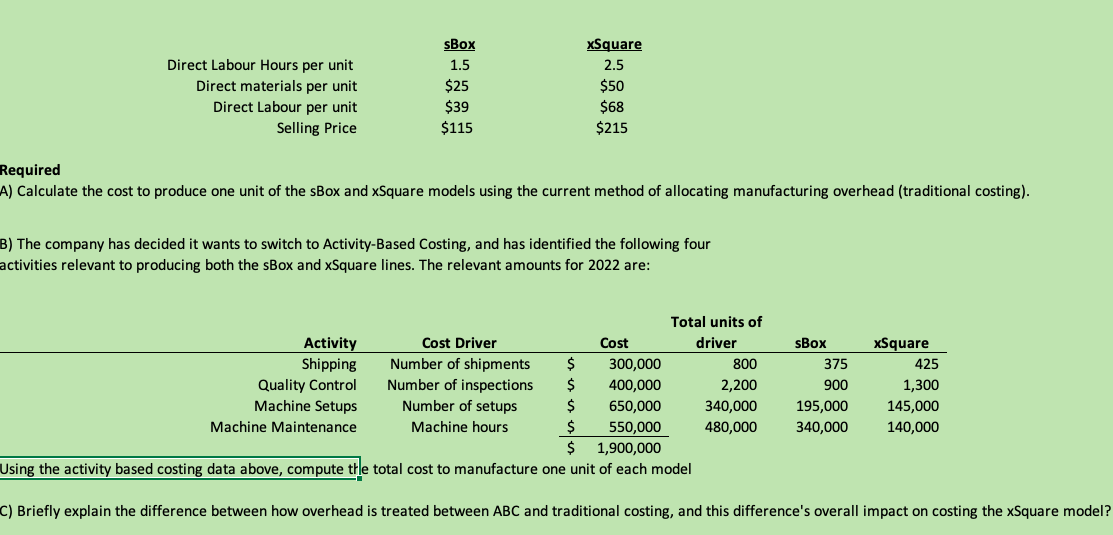

Bata Ltd manufactures two different models of its famous video game console: the sBox and xSquare models. The company has been producing the sBox model for 10 years; whereas the xSquare model was introduced this year to appeal to a wider variety of consumers and capture a larger segment of the video game market. Once the xSquare product line was introduced, profits declined rapidly. Management has become concerned about the accuracy of their costing system as sales of the xSquare system have been increasing rapidly since being released. Bata Ltd currently allocates manufacturing overhead using direct labor hours as the cost driver. The company has estimated it will incur $1,900,000 in manufacturing overhead costs and produce 50,000 units of the sBox model and 7,000 units of the xSquare model. The following information pertains to the production of the sBox and xSquare models:

Q: Cans plc is developing a new form of 'crinkly can' for soft drinks. The crinkly can has grooves in…

A: Contribution Margin is simply the leftover amount after direct sales costs that a company has to pay…

Q: Each year, Sunshine Motos surveys 7,500 former and prospective customers regarding satisfaction and…

A: The difference in the total costs as a result of the change in certain activities is known as the…

Q: Required: a. How much overhead will be assigned to each product if these three cost drivers are…

A:

Q: Siegel Corporation manufactures a product available in both a deluxe and a regular model. The…

A: Manufacturing overheads are the indirect costs and expense related to production and manufacturing…

Q: Maglie Company manufactures two video game consoles: handheld and home. The handheld consoles are…

A: Case 1:Under ABC CostingActivity based costing allocates manufacturing overhead on a more logical…

Q: Required: a. How much overhead will be assigned to each product if these three cost drivers are…

A: In this Numerical Has Covered The concept of Activity Based Costing and Traditional Costing.…

Q: Tool Industries manufactures large workbenches for industrial use. Sam Hartnet, the Vice President…

A: According to the question, we are required to compute the current cost per unit or workbenches. As…

Q: Pix Paper Inc. produces photographic paper for printing digital images. One of the processes for…

A: Computation of Cost per pound - Working

Q: Clason, Inc. manufactures door panels. Suppose clason is considering sending the following amounts…

A: Cost of new quality program = 68000 + 27000+ 39000 +58000 = $ 192000 Cost of old program = 86000+…

Q: Harris Systems has decided to adopt ABC. To remain competitive, Harris Systems’s management believes…

A:

Q: Titan Computer Company manufactures a tablet computer called AllPad. The company sells these tablets…

A: Competitive strategy: Cost leadership and differentiation are the two competitive strategies. In…

Q: The Presidio Company has redesigned one of its products and is deciding on the pricing for the…

A: Desired profit = (Investment required x Target return on investment)

Q: Silver Company manufactures a product that is available in both a complex model and a regular model.…

A: Model Complex Regular Total Estimated production 5000 40000 (*) Direct labor hours per…

Q: How much overhead will be assigned to each product if these three cost drivers are used to allocate…

A:

Q: Quality Industries manufactures large workbenches for industrial use. Yewell Hartnet, the Vice…

A: Unit cost for 14,100=8,299,75014,100=588.63 or 589 Thus, the unit cost for 14,100 tables is 589.

Q: Thai manufacturing Inc. began operations five years ago producing a new diagnostic instrument, it…

A: PLEASE LIKE THE ANSWER, YOUR RESPONSE MATTERS Part A Other reasons might cause a firm to construct…

Q: After completing his analysis, Jacobs shows the results to Charles Clark, the Plum division…

A:

Q: TwoShaft Inc. manufactures a wide variety of parts for recreational boating, including boat engines.…

A: Direct cost is the cost that is directly involved in the production process of the company.

Q: Magle Company manufactures two video game consoies handheld and home. The handheld consoles are…

A: Overheads are those indirect costs which can not be allocated directly. Activity based costing…

Q: Tell what life-cycle cost management is and how it can be used to maximize profits over a product's…

A: In this question there are multiple question, but we solved on 3 sub-parts as per guidelines, if you…

Q: McDermott Company has developed a new industrial component called IC-75. The company is excited…

A: Reference Value- A reference value is the recognized and accurate measurement for each part. The…

Q: . A company produces two kinds of hammers: one with longer handles and one with shorter handles. The…

A: Contribution margin = Sales price - Variable expenses

Q: Maxwell Company produces a variety of kitchen appliances, including cooking ranges and dishwashers.…

A:

Q: Holton Chairs had been an innovative designer and producer of quality office chairs since Arnold…

A: Recording Journal entries in the books of Holton-Central Holdings Inc. DATE PARTICULARS Ref No…

Q: Ken Yalters, the COO of FreshSkin, asked his cost management team for a product line profitability…

A: solution : calculation of profit before taxes for the Bskin product, per life-cycle income…

Q: Maglie Company manufactures two video game consoles: handheld and home. The handheld consoles are…

A: The overhead cost is allocated to the production on the basis of predetermined overhead rate.

Q: The Chromosome Manufacturing Company produces two products, X and Y. The company president, Gene…

A: 1) Overhead cost allocated to X based on labor hours=Total overhead cost×(Labor hour of X/Labor hour…

Q: Dana Wise, president of Tidwell Company, recently returned from a conference on quality and…

A: 1. Prepare a simple quality cost report classifying costs by category.

Q: Nico Parts, Inc., produces electronic products with short life cycles (of less than two years).…

A: The question is based on the concept of Cost Accounting.

Q: Benchmark Industries manufactures large workbenches for industrial use. Wally Garcia, the vice…

A: Budgeted amounts are prepared so that they can help the firm in attaining the actual output within…

Q: Maglie Company manufactures two video game consoles: handheld and home. The handheld consoles are…

A: Formula: Allocation of overhead = ( Individual activity level / total activity level ) x Total cost…

Q: The Baldwin Company, originally established 16 years ago to make footballs, is now a leading…

A: Income statement: It is a financial statement that calculates the net income generated by a company…

Q: ABC Corporation has recently completed a project to reduce total production costs by 5%. Net income…

A: Part A: Cost of Quality: Cost of quality (COQ) is defined as a methodology that allows an…

Q: The Chromosome Manufacturing Company produces two products, X and Y. The company president, Gene…

A: Overhead expenses refers to all those expenses which are considered as continuos form of expenses…

Q: Ken Yalters, the COO of FreshSkin, asked his cost management team for a product line profitability…

A: Profit before taxes can be calculated by deducting research and development expenses and selling…

Q: Mirabel Manufacturing is a small but growing company that manufactures and sells marine sonar…

A: Note: Since we only answer up to 3 sub-parts, we’ll answer the first 3. Please resubmit the question…

Q: Titan Computer Company manufactures a tablet computer called All Pad. The company sells these…

A: Competitive strategy: Cost leadership and differentiation are the two competitive strategies. In…

Q: For years, Tamarindo Company produced only one product: backpacks. Recently, Tamarindo added a line…

A:

Q: Maglie Company manufactures two video game consoles: handheld and home. The handheld consoles are…

A: Total cost = Direct materials + direct labor + overhead applied Predetermined overhead rate =…

Q: Thai manufacturing Inc. began operations five years ago producing a new diagnostic instrument, it…

A:

Q: Whitaker Company produces two models of blenders for restaurants: the “Super Model” (priced at…

A: Total overhead=Machining Cost+Inspection Cost+Rework Cost Overhead per machine hour=Total…

Q: Holton Chairs had been an innovative designer and producer of quality office chairs since Arnold…

A: A journal entry is made to record the financial transaction in the books of accounts. Note: As you…

Q: Ken Yalters, the COO of FreshSkin, asked his cost management team for a product line profitability…

A: % of allocation of research and development and selling expense to Bskin = 100% - 75% = 25%…

Q: what life-cycle cost management is and how it can be used to maximize profits over a product's life…

A: Life cycle cost management is defined as the procedure for controlling as well as planning the costs…

Q: Maglie Company manufactures two video game consoles: handheld and home. The handheld consoles are…

A: The question is related to Overhead allocation. The details are given regarding the same.

Q: Sylar Company manufactures a product that is available in both a Deluxe model and a Regular model.…

A: Calvulation of manufacturing overhead rate per Direct Labour Hour:: Manufacturing overhead…

Any help would be appreciated.

Step by step

Solved in 4 steps with 7 images

- Boxer Production, Inc., is in the process of considering a flexible manufacturing system that will help the company react more swiftly to customer needs. The controller, Mick Morrell, estimated that the system will have a 10-year life and a required return of 10% with a net present value of negative $500,000. Nevertheless, he acknowledges that he did not quantify the potential sales increases that might result from this improvement on the issue of on-time delivery, because it was too difficult to quantify. If there is a general agreement that qualitative factors may offer an additional net cash flow of $150,000 per year, how should Boxer proceed with this Investment?At the beginning of the last quarter of 20x1, Youngston, Inc., a consumer products firm, hired Maria Carrillo to take over one of its divisions. The division manufactured small home appliances and was struggling to survive in a very competitive market. Maria immediately requested a projected income statement for 20x1. In response, the controller provided the following statement: After some investigation, Maria soon realized that the products being produced had a serious problem with quality. She once again requested a special study by the controllers office to supply a report on the level of quality costs. By the middle of November, Maria received the following report from the controller: Maria was surprised at the level of quality costs. They represented 30 percent of sales, which was certainly excessive. She knew that the division had to produce high-quality products to survive. The number of defective units produced needed to be reduced dramatically. Thus, Maria decided to pursue a quality-driven turnaround strategy. Revenue growth and cost reduction could both be achieved if quality could be improved. By growing revenues and decreasing costs, profitability could be increased. After meeting with the managers of production, marketing, purchasing, and human resources, Maria made the following decisions, effective immediately (end of November 20x1): a. More will be invested in employee training. Workers will be trained to detect quality problems and empowered to make improvements. Workers will be allowed a bonus of 10 percent of any cost savings produced by their suggested improvements. b. Two design engineers will be hired immediately, with expectations of hiring one or two more within a year. These engineers will be in charge of redesigning processes and products with the objective of improving quality. They will also be given the responsibility of working with selected suppliers to help improve the quality of their products and processes. Design engineers were considered a strategic necessity. c. Implement a new process: evaluation and selection of suppliers. This new process has the objective of selecting a group of suppliers that are willing and capable of providing nondefective components. d. Effective immediately, the division will begin inspecting purchased components. According to production, many of the quality problems are caused by defective components purchased from outside suppliers. Incoming inspection is viewed as a transitional activity. Once the division has developed a group of suppliers capable of delivering nondefective components, this activity will be eliminated. e. Within three years, the goal is to produce products with a defect rate less than 0.10 percent. By reducing the defect rate to this level, marketing is confident that market share will increase by at least 50 percent (as a consequence of increased customer satisfaction). Products with better quality will help establish an improved product image and reputation, allowing the division to capture new customers and increase market share. f. Accounting will be given the charge to install a quality information reporting system. Daily reports on operational quality data (e.g., percentage of defective units), weekly updates of trend graphs (posted throughout the division), and quarterly cost reports are the types of information required. g. To help direct the improvements in quality activities, kaizen costing is to be implemented. For example, for the year 20x1, a kaizen standard of 6 percent of the selling price per unit was set for rework costs, a 25 percent reduction from the current actual cost. To ensure that the quality improvements were directed and translated into concrete financial outcomes, Maria also began to implement a Balanced Scorecard for the division. By the end of 20x2, progress was being made. Sales had increased to 26,000,000, and the kaizen improvements were meeting or beating expectations. For example, rework costs had dropped to 1,500,000. At the end of 20x3, two years after the turnaround quality strategy was implemented, Maria received the following quality cost report: Maria also received an income statement for 20x3: Maria was pleased with the outcomes. Revenues had grown, and costs had been reduced by at least as much as she had projected for the two-year period. Growth next year should be even greater as she was beginning to observe a favorable effect from the higher-quality products. Also, further quality cost reductions should materialize as incoming inspections were showing much higher-quality purchased components. Required: 1. Identify the strategic objectives, classified by the Balanced Scorecard perspective. Next, suggest measures for each objective. 2. Using the results from Requirement 1, describe Marias strategy using a series of if-then statements. Next, prepare a strategy map. 3. Explain how you would evaluate the success of the quality-driven turnaround strategy. What additional information would you like to have for this evaluation? 4. Explain why Maria felt that the Balanced Scorecard would increase the likelihood that the turnaround strategy would actually produce good financial outcomes. 5. Advise Maria on how to encourage her employees to align their actions and behavior with the turnaround strategy.Wright Plastic Products is a small company that specialized in the production of plastic dinner plates until several years ago. Although profits for the company had been good, they have been declining in recent years because of increased competition. Many competitors offer a full range of plastic products, and management felt that this created a competitive disadvantage. The output of the companys plants was exclusively devoted to plastic dinner plates. Three years ago, management made a decision to add additional product lines. They determined that existing idle capacity in each plant could easily be adapted to produce other plastic products. Each plant would produce one additional product line. For example, the Atlanta plant would add a line of plastic cups. Moreover, the variable cost of producing a package of cups (one dozen) was virtually identical to that of a package of plastic plates. (Variable costs referred to here are those that change in total as the units produced change. The costs include direct materials, direct labor, and unit-based variable overhead such as power and other machine costs.) Since the fixed expenses would not change, the new product was forecast to increase profits significantly (for the Atlanta plant). Two years after the addition of the new product line, the profits of the Atlanta plant (as well as other plants) had not improvedin fact, they had dropped. Upon investigation, the president of the company discovered that profits had not increased as expected because the so-called fixed cost pool had increased dramatically. The president interviewed the manager of each support department at the Atlanta plant. Typical responses from four of those managers are given next. Materials handling: The additional batches caused by the cups increased the demand for materials handling. We had to add one forklift and hire additional materials handling labor. Inspection: Inspecting cups is more complicated than plastic plates. We only inspect a sample drawn from every batch, but you need to understand that the number of batches has increased with this new product line. We had to hire more inspection labor. Purchasing: The new line increased the number of purchase orders. We had to use more resources to handle this increased volume. Accounting: There were more transactions to process than before. We had to increase our staff. Required: 1. Explain why the results of adding the new product line were not accurately projected. 2. Could this problem have been avoided with an activity-based cost management system? If so, would you recommend that the company adopt this type of system? Explain and discuss the differences between an activity-based cost management system and a traditional cost management system.

- Nico Parts, Inc., produces electronic products with short life cycles (of less than two years). Development has to be rapid, and the profitability of the products is tied strongly to the ability to find designs that will keep production and logistics costs low. Recently, management has also decided that post-purchase costs are important in design decisions. Last month, a proposal for a new product was presented to management. The total market was projected at 200,000 units (for the two-year period). The proposed selling price was 130 per unit. At this price, market share was expected to be 25 percent. The manufacturing and logistics costs were estimated to be 120 per unit. Upon reviewing the projected figures, Brian Metcalf, president of Nico, called in his chief design engineer, Mark Williams, and his marketing manager, Cathy McCourt. The following conversation was recorded: BRIAN: Mark, as you know, we agreed that a profit of 15 per unit is needed for this new product. Also, as I look at the projected market share, 25 percent isnt acceptable. Total profits need to be increased. Cathy, what suggestions do you have? CATHY: Simple. Decrease the selling price to 125 and we expand our market share to 35 percent. To increase total profits, however, we need some cost reductions as well. BRIAN: Youre right. However, keep in mind that I do not want to earn a profit that is less than 15 per unit. MARK: Does that 15 per unit factor in preproduction costs? You know we have already spent 100,000 on developing this product. To lower costs will require more expenditure on development. BRIAN: Good point. No, the projected cost of 120 does not include the 100,000 we have already spent. I do want a design that will provide a 15-per-unit profit, including consideration of preproduction costs. CATHY: I might mention that post-purchase costs are important as well. The current design will impose about 10 per unit for using, maintaining, and disposing our product. Thats about the same as our competitors. If we can reduce that cost to about 5 per unit by designing a better product, we could probably capture about 50 percent of the market. I have just completed a marketing survey at Marks request and have found out that the current design has two features not valued by potential customers. These two features have a projected cost of 6 per unit. However, the price consumers are willing to pay for the product is the same with or without the features. Required: 1. Calculate the target cost associated with the initial 25 percent market share. Does the initial design meet this target? Now calculate the total life-cycle profit that the current (initial) design offers (including preproduction costs). 2. Assume that the two features that are apparently not valued by consumers will be eliminated. Also assume that the selling price is lowered to 125. a. Calculate the target cost for the 125 price and 35 percent market share. b. How much more cost reduction is needed? c. What are the total life-cycle profits now projected for the new product? d. Describe the three general approaches that Nico can take to reduce the projected cost to this new target. Of the three approaches, which is likely to produce the most reduction? 3. Suppose that the Engineering Department has two new designs: Design A and Design B. Both designs eliminate the two nonvalued features. Both designs also reduce production and logistics costs by an additional 8 per unit. Design A, however, leaves post-purchase costs at 10 per unit, while Design B reduces post-purchase costs to 4 per unit. Developing and testing Design A costs an additional 150,000, while Design B costs an additional 300,000. Assuming a price of 125, calculate the total life-cycle profits under each design. Which would you choose? Explain. What if the design you chose cost an additional 500,000 instead of 150,000 or 300,000? Would this have changed your decision? 4. Refer to Requirement 3. For every extra dollar spent on preproduction activities, how much benefit was generated? What does this say about the importance of knowing the linkages between preproduction activities and later activities?Bienestar, Inc., has two plants that manufacture a line of wheelchairs. One is located in Kansas City, and the other in Tulsa. Each plant is set up as a profit center. During the past year, both plants sold their tilt wheelchair model for 1,620. Sales volume averages 20,000 units per year in each plant. Recently, the Kansas City plant reduced the price of the tilt model to 1,440. Discussion with the Kansas City manager revealed that the price reduction was possible because the plant had reduced its manufacturing and selling costs by reducing what was called non-value-added costs. The Kansas City manufacturing and selling costs for the tilt model were 1,260 per unit. The Kansas City manager offered to loan the Tulsa plant his cost accounting manager to help it achieve similar results. The Tulsa plant manager readily agreed, knowing that his plant must keep pacenot only with the Kansas City plant but also with competitors. A local competitor had also reduced its price on a similar model, and Tulsas marketing manager had indicated that the price must be matched or sales would drop dramatically. In fact, the marketing manager suggested that if the price were dropped to 1,404 by the end of the year, the plant could expand its share of the market by 20 percent. The plant manager agreed but insisted that the current profit per unit must be maintained. He also wants to know if the plant can at least match the 1,260 per-unit cost of the Kansas City plant and if the plant can achieve the cost reduction using the approach of the Kansas City plant. The plant controller and the Kansas City cost accounting manager have assembled the following data for the most recent year. The actual cost of inputs, their value-added (ideal) quantity levels, and the actual quantity levels are provided (for production of 20,000 units). Assume there is no difference between actual prices of activity units and standard prices. Required: 1. Calculate the target cost for expanding the Tulsa plants market share by 20 percent, assuming that the per-unit profitability is maintained as requested by the plant manager. 2. Calculate the non-value-added cost per unit. Assuming that non-value-added costs can be reduced to zero, can the Tulsa plant match the Kansas City per-unit cost? Can the target cost for expanding market share be achieved? What actions would you take if you were the plant manager? 3. Describe the role that benchmarking played in the effort of the Tulsa plant to protect and improve its competitive position.Salem Electronics currently produces two products: a programmable calculator and a tape recorder. A recent marketing study indicated that consumers would react favorably to a radio with the Salem brand name. Owner Kenneth Booth was interested in the possibility. Before any commitment was made, however, Kenneth wanted to know what the incremental fixed costs would be and how many radios must be sold to cover these costs. In response, Betty Johnson, the marketing manager, gathered data for the current products to help in projecting overhead costs for the new product. The overhead costs based on 30,000 direct labor hours follow. (The high-low method using direct labor hours as the independent variable was used to determine the fixed and variable costs.) All depreciation. The following activity data were also gathered: Betty was told that a plantwide overhead rate was used to assign overhead costs based on direct labor hours. She was also informed by engineering that if 20,000 radios were produced and sold (her projection based on her marketing study), they would have the same activity data as the recorders (use the same direct labor hours, machine hours, setups, and so on). Engineering also provided the following additional estimates for the proposed product line: Upon receiving these estimates, Betty did some quick calculations and became quite excited. With a selling price of 26 and just 18,000 of additional fixed costs, only 4,500 units had to be sold to break even. Since Betty was confident that 20,000 units could be sold, she was prepared to strongly recommend the new product line. Required: 1. Reproduce Bettys break-even calculation using conventional cost assignments. How much additional profit would be expected under this scenario, assuming that 20,000 radios are sold? 2. Use an activity-based costing approach, and calculate the break-even point and the incremental profit that would be earned on sales of 20,000 units. 3. Explain why the CVP analysis done in Requirement 2 is more accurate than the analysis done in Requirement 1. What recommendation would you make?

- Harvey Company produces two models of blenders: the Super Model (priced at 400) and the Special Model (priced at 200). Recently, Harvey has been losing market share with its Special Model because of competitors offering blenders with the same quality and features but at a lower price. A careful market study revealed that if Harvey could reduce the price of its Special Model to 180, it would regain its former share of the market. Management, however, is convinced that any price reduction must be accompanied by a cost reduction of the same amount so that per-unit profitability is not affected. Earl Wise, company controller, has indicated that poor overhead costing assignments may be distorting managements view of each products cost and, therefore, the ability to know how to set selling prices. Earl has identified the following overhead activities: machining, inspection, and rework. The three activities, their costs, and practical capacities are as follows: The consumption patterns of the two products are as follows: Harvey assigns overhead costs to the two products using a plantwide rate based on machine hours. Required: 1. Calculate the unit overhead cost of the Special Model using machine hours to assign overhead costs. Now, repeat the calculation using ABC to assign overhead costs. Did improving the accuracy of cost assignments solve Harveys competitive problem? What did it reveal? 2. Now, assume that in addition to improving the accuracy of cost assignments, Earl observes that defective supplier components are the root cause of both the inspection and rework activities. Suppose further that Harvey has found a new supplier that provides higher-quality components such that inspection and rework costs are reduced by 50 percent. Now, calculate the cost of the Special Model (assuming that inspection and rework times are also reduced by 50 percent) using ABC. The relative consumption patterns also remain the same. Comment on the difference between ABC and ABM.Bannister Company, an electronics firm, buys circuit boards and manually inserts various electronic devices into the printed circuit board. Bannister sells its products to original equipment manufacturers. Profits for the last two years have been less than expected. Mandy Confer, owner of Bannister, was convinced that her firm needed to adopt a revenue growth and cost reduction strategy to increase overall profits. After a careful review of her firms condition, Mandy realized that the main obstacle for increasing revenues and reducing costs was the high defect rate of her products (a 6 percent reject rate). She was certain that revenues would grow if the defect rate was reduced dramatically. Costs would also decline as there would be fewer rejects and less rework. By decreasing the defect rate, customer satisfaction would increase, causing, in turn, an increase in market share. Mandy also felt that the following actions were needed to help ensure the success of the revenue growth and cost reduction strategy: a. Improve the soldering capabilities by sending employees to an outside course. b. Redesign the insertion process to eliminate some of the common mistakes. c. Improve the procurement process by selecting suppliers that provide higher-quality circuit boards. Required: 1. State the revenue growth and cost reduction strategy using a series of cause-and-effect relationships expressed as if-then statements. 2. Illustrate the strategy using a strategy map. 3. Explain how the revenue growth strategy can be tested. In your explanation, discuss the role of lead and lag measures, targets, and double-loop feedback.Jadlow Company produces handcrafted leather purses. Virtually all of the manufacturing cost consists of materials and labor. Over the past several years, profits have been declining because the cost of the two major inputs has been increasing. Janice Jadlow, the president of the company, has indicated that the price of the purses cannot be increased; thus, the only way to improve or at least stabilize profits is to increase overall productivity. At the beginning of 20x2, Janice implemented a new cutting and assembly process that promised less materials waste and a faster production time. At the end of 20x2, Janice wants to know how much profits have changed from the prior year because of the new process. In order to provide this information to Janice, the controller of the company gathered the following data: Required: 1. Compute the productivity profile for each year. Comment on the effectiveness of the new production process. 2. Compute the increase in profits attributable to increased productivity. 3. Calculate the price-recovery component, and comment on its meaning.

- Danna Martin, president of Mays Electronics, was concerned about the end-of-the year marketing report that she had just received. According to Larry Savage, marketing manager, a price decrease for the coming year was again needed to maintain the companys annual sales volume of integrated circuit boards (CBs). This would make a bad situation worse. The current selling price of 18 per unit was producing a 2-per-unit profithalf the customary 4-per-unit profit. Foreign competitors kept reducing their prices. To match the latest reduction would reduce the price from 18 to 14. This would put the price below the cost to produce and sell it. How could these firms sell for such a low price? Determined to find out if there were problems with the companys operations, Danna decided to hire a consultant to evaluate the way in which the CBs were produced and sold. After two weeks, the consultant had identified the following activities and costs: The consultant indicated that some preliminary activity analysis shows that per-unit costs can be reduced by at least 7. Since the marketing manager had indicated that the market share (sales volume) for the boards could be increased by 50% if the price could be reduced to 12, Danna became quite excited. Required: 1. CONCEPTUAL CONNECTION What is activity-based management? What phases of activity analysis did the consultant provide? What else remains to be done? 2. CONCEPTUAL CONNECTION Identify as many nonvalue-added costs as possible. Compute the cost savings per unit that would be realized if these costs were eliminated. Was the consultant correct in the preliminary cost reduction assessment? Discuss actions that the company can take to reduce or eliminate the nonvalue-added activities. 3. Compute the unit cost required to maintain current market share, while earning a profit of 4 per unit. Now compute the unit cost required to expand sales by 50%, assuming a per-unit profit of 4. How much cost reduction would be required to achieve each unit cost? 4. Assume that further activity analysis revealed the following: switching to automated insertion would save 60,000 of engineering support and 90,000 of direct labor. Now, what is the total potential cost reduction per unit available from activity analysis? With these additional reductions, can Mays achieve the unit cost to maintain current sales? To increase it by 50%? What form of activity analysis is this: reduction, sharing, elimination, or selection? 5. CONCEPTUAL CONNECTION Calculate income based on current sales, prices, and costs. Then calculate the income by using a 14 price and a 12 price, assuming that the maximum cost reduction possible is achieved (including Requirement 4s reduction). What price should be selected?Danna Wise, president of Tidwell Company, recently returned from a conference on quality and productivity. At the conference, she was told that many American firms have quality costs totaling 20 to 30% of sales. The quality experts at the conference convinced her that a company could increase its profitability by improving quality. However, she was of the opinion that the quality of Tidwell Company was much less than 20%probably more in the 4 to 6% range. However, because the potential for increasing profits was so great if she was wrong, she decided to request a preliminary estimate of the total quality costs currently being incurred. She asked her controller for a summary of quality costs, with the costs classified into four categories: prevention, appraisal, internal failure, or external failure. She also wanted the costs expressed as a percentage of both sales and profits. The controller had his staff assemble the following information from the past year, 20X1: a. Sales revenue, 37,240,000; net income, 4,000,000. b. During the year, customers returned 40,000 units needing repair. Repair cost averages 9 per unit. c. Twelve inspectors are employed, each earning an annual salary of 80,000. The inspectors are involved only with final inspection (product acceptance). d. Total scrap is 200,000 units. Of this total, ninety percent is quality related. The cost of scrap is about 10 per unit. e. Each year, approximately 800,000 units are rejected in final inspection. Of these units, seventy-five percent can be recovered through rework. The cost of rework is 1.80 per I unit. f. A customer cancelled an order that would have increased profits by 600,000. The customers reason for cancellation was poor product performance. g. The company employs 10 full-time employees in its complaint department. Each earns 48,600 a year. h. The company gave sales allowances totaling 180,000 due to substandard products being sent to the customer. i. The company requires all new employees to take its 4-hour quality training program. The estimated annual cost of the program is 120,000. Required: 1. Prepare a simple quality cost report classifying costs by category. 2. Compute the quality cost-sales ratio. Also, compare the total quality costs with total profits. Should Danna be concerned with the level of quality costs? 3. Prepare a pie chart for the quality costs. Discuss the distribution of quality costs among the four categories. Are they properly distributed? Explain. 4. Discuss how the company can improve its overall quality and at the same time reduce total quality costs. 5. By how much will profits increase if quality costs are reduced to 3% of sales?Mallorys Video Supply has changed its focus tremendously and as a result has dropped the selling price of DVD players from $45 to $38. Some units in the work-in-process inventory have costs of $30 per unit associated with them, but Mallory can only sell these units in their current state for $22 each. Otherwise, it will cost Mallory $11 per unit to rework these units so that they can be sold for $38 each. How much is the financial impact if the units are processed further? A. $5 per unit profit 8. $16 per unit profit C. $3 per unit loss D. $12 per unit loss