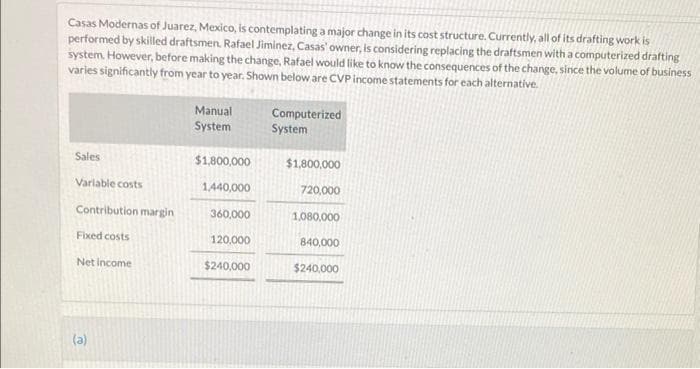

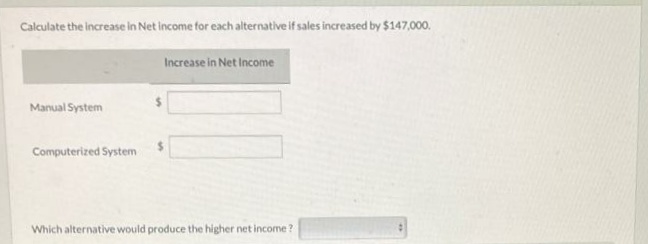

Casas Modernas of Juarez, Mexico, is contemplating a major change in its cost structure. Currently, all of its drafting work is performed by skilled draftsmen. Rafael Jiminez, Casas' owner, is considering replacing the draftsmen with a computerized drafting system. However, before making the change, Rafael would like to know the consequences of the change, since the volume of business varies significantly from year to year. Shown below are CVP income statements for each alternative. Sales Variable costs Contribution margin Fixed costs Net income Manual System $1,800,000 1,440,000 360,000 120,000 $240,000 Computerized System $1,800,000 720,000 1,080,000 840,000 $240,000

Q: a) Estimated profit and loss account (Profit and loss budget) b) Cash budget c) Estimated balance…

A: Computation of accounts receivables at the end of Year Accounts Receivables at 31.12.201X = Turnover…

Q: n engineer intends to travel abroad to take a postgraduate course at a maternity hospital. He…

A: Value would he need to have today to make his plans viable = $72.688.7

Q: uring 2020, Ma

A: Shareholders also invest money in the company and in return they become the owners in proportion to…

Q: Tetros bros producing oxygen valves and it was leading in market share for its oxygen new gen kit…

A: Bonds was used to raise money for the business for various purposes in which the company will pay…

Q: A business purchased a new car at the start of October for $16,800 cash. The car has a useful life…

A: Introduction: Depreciation: Decreasing value of fixed assets over its useful life period called as…

Q: 1. Calculate the normal tax consequences arising from the above distributions for Sehari (Pty) Ltd’s…

A: The tax slab rate as applicable is as follows: Taxable Income (R) Tax Rate R1 - R216,200 18%…

Q: Equity Investments: Less than 20% ownership On September 12, 3,600 shares of Denver Company’s…

A: Journal entries means the entry in prime book with chronological sequence. Share has been valued at…

Q: On January 1, ABC, DEF and GHI admitted JKL as a new partner. The partners were sharing profits in a…

A: The capital balance of the partners after the admission of partners are adjusted as per the balance…

Q: Study the information provided below and calculate the expected value of closing inventory as at 31…

A: The cost of goods sold includes the total cost of goods that are sold during the period. Cost of…

Q: Bal. 1/1 Bal. 12/31 Bal. 1/1 Direct material Direct labor Manufacturing overhead Bal. 12/31…

A: Raw material inventory :- raw material inventory describe about, how much raw material in inventory,…

Q: If JoBlo Inc., has a retained earnings opening balance of $50,000 at the beginning of the year, and…

A: Introduction: Retained Earnings: Retained Earnings are shareholder funds. Profit is retained with…

Q: A primary advantage of using generalized audit software packages to audit the financial statements…

A: The primary advantage of using a prepacked audit system is determine by the use cases.

Q: Partners ABC, DEF and GHI share profits and losses in the ratio of 2:3:5, respectively. At the end…

A: Liquidation means where the business is shut down , assets are sold out and liabilities are paid…

Q: 1 2 3 5. 6. 7. Lacson invested P100,000 cash in the business Paid P5,000 for office rent for the…

A: Introduction:- Journal entry is the first stage of accounting process. Journal entry used to record…

Q: 4. Find the compound amount and interest on P360,000 for 8 years and 6 months at 10% compounded…

A: Compound Amount = P x (1 + r)^n Interest = Compound Amount - Principal

Q: NTJ Distributors Ltd has has an annual demand for an airport metal detector of 1400 units. The cost…

A: Lets understand the basics. Economic order quantity is a quantity at which carrying cost and…

Q: Required information [The following information applies to the questions displayed below.] Lamonte…

A: The income statement includes all the revenue and expenses. The resulted amount after deducting…

Q: Kegler Bowling buys scorekeeping equipment with an invoice cost of $185,000. The electrical work…

A: The equipment cost includes all those expenses that are incurred to make the equipment ready to use.…

Q: The cost of a manufactured product (product cost) generally consists of which of the following?…

A: Product Cost - Product Cost is the cost incurred by the organization for the product of the entity.…

Q: Sky Company is unable to reconcile the bank balance at January 31. Sky's reconciliation is as…

A: A bank reconciliation statement is prepared by the management to match the company's cash balance…

Q: During her lifetime, Elaine made several property transfers, including the following: a) The…

A: As per the Federal rules any gift given in the year 2022 exceeding $16,000 to a single person will…

Q: Partners ABC, DEF and GHI share profits and losses in the ratio of 2:3:5, respectively. At the end…

A: Partnership is formed by two or more persons who have decided to share profit and loss in their…

Q: In how many months will money become three times itself at 9% compounded semiannually? Solution:

A: Future Value = Present Value x (1 + r)^n Rearranging the formula, we get (1 + r)^n = Future Value /…

Q: On January 15, Ross Furniture, Inc., accepts a $5,000, 180-day, 10 percent note from a customer at…

A: Introduction: Journals: 1 ) Journals are book of prime records. 2 ) All the business transactions…

Q: Macaron Corporation is making a $96,400 investment in equipment with a 5-year life. The company uses…

A: Lets understand the basics. Depreciation is a reduction in value of asset due to wear and tear…

Q: Zachary Company has 600,000 shares of common stock outstanding. Perette Corporation purchases…

A: Introduction: Common stock outstanding: It shows the number of share issued by the company which are…

Q: The Dorilane Company produces a set of wood patio furniture consisting of a table and four customer…

A: Cost is classified into two categories: Fixed: It is the cost that remains same as a whole but…

Q: If Kim buys a car for $30,000 with an estimated life of 5 years, with a residual value of $5,000,…

A: Introduction: Depreciation: Decreasing value of fixed assets over its useful life period called as…

Q: Machinery Purchased for $ 800000 Accumulated depreciation value is $ 600000 Sold for $400000…

A: The depreciation expense is charged on fixed assets as reduced value of the fixed asset with usage…

Q: . Which of the following business units has the highest beta factor?

A: Banks or any other business has one the feature or we can say a disadvantage which is the risk which…

Q: If the company sells 4,900 units, its total contribution margin should be closest to: (Do not round…

A: Contribution margin is that portion of sales, which comes after subtracting total variable cost from…

Q: direct materials mix variance for this problem

A: The benchmark is established in advance, and actual performance is assessed in comparison to it.…

Q: Gibson Boot Co. sells men’s, women’s, and children’s boots. For each type of boot sold, it operates…

A: Calculation of above requirement are as follows

Q: Which of the following statement is correct about the statement of affairs?

A: choice questions kindly resubmit remaining question. Companies whenever went for the liquidation…

Q: What is the journal entry to record a sale of a completed job for $10,000 with terms of n/60. Group…

A: Job Order: The job ad, also known as the requisition, is referred to as the job order. Once a…

Q: On January 1, 2020, Surf Company purchased the debt instruments of Smooth Company with a face value…

A: Unrealized gain/(loss)=Fair market value of investment-Book value of investment

Q: Your company declared $13,800 cash dividends on stock. dividends payable at the beginning of the…

A: The cash flow statement is prepared to record the cash flow from various activities during the…

Q: Record the journal entries for the 2 listed events below. 1. On June 13, 2022, Best Buy issued…

A: Introduction: A journal entry is a record of a business transaction in an accounting system. Journal…

Q: Pulsar Plc is considering of exporting its products to the Swedish market. It expects to earn an…

A: Formula = Economic profit / ( loss) = Revenue Less : opportunity cost Less : explicit cost

Q: Comparing Three Depreciation Methods Dexter Industries purchased packaging equipment on January 8…

A: Depreciation Expenses - Depreciation Expenses are the expense incurred on the wear and tear of the…

Q: If money is worth 8% annually, what annual payment is required to raise ₱ 18,811 after 2 years if…

A: Future Value of Annuity Due = (1 + r) x P x [{(1 + r)^n} - 1] / r

Q: a. Production schedule by product. Note: Use a negative sign in your schedule to indicate that an…

A: Budgeting is a process by which a business entity make its financial plans and set targets. Budgets…

Q: Nature of Transaction 1. Cash payment on hydro bill that arrived today 2. Cash sale 3. Bank interest…

A: Introduction: Journals: All the business transactions are to be recorded in Journals. Journals also…

Q: Cash Flow from Operating Activities (Indirect Method) The Arcadia Company owns no plant assets and…

A: Under indirect method of cash flow statement, net income will be adjusted to the non cash expenses…

Q: Martinez Company’s relevant range of production is 7,500 units to 12,500 units. When it produces and…

A: The incremental cost is also known as marginal cost. It is an additional cost incurred due to an…

Q: Zannel plc is considering a new project to produce a revolutionary surveillance device. The initial…

A: NPV (Net Present Value) represents the difference between the present value of future expected cash…

Q: 2.1 Use the information provided below to calculate the number of units of Product Tex that must be…

A: Given that, Estimated Sales volume for ; June = 25 000 units July = 21 000 units August = 30 000…

Q: Arca Company reports the following for its product for its first year of operations. Direct…

A: Given that, Selling price per unit = $390 Units produced = 2,580 units Units sold = 2,180 units…

Q: ABC Corporation is experiencing difficulty in paying its bills and is considering filing for…

A: The net free assets are the amount of realized value of an asset after secured creditor and…

Q: a. The market value of the comps should be available. b. The valuation object should be compared…

A: d. The prices of the comps should be standardized, meaning a price ratio instead of the absolute…

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

- At the beginning of the last quarter of 20x1, Youngston, Inc., a consumer products firm, hired Maria Carrillo to take over one of its divisions. The division manufactured small home appliances and was struggling to survive in a very competitive market. Maria immediately requested a projected income statement for 20x1. In response, the controller provided the following statement: After some investigation, Maria soon realized that the products being produced had a serious problem with quality. She once again requested a special study by the controllers office to supply a report on the level of quality costs. By the middle of November, Maria received the following report from the controller: Maria was surprised at the level of quality costs. They represented 30 percent of sales, which was certainly excessive. She knew that the division had to produce high-quality products to survive. The number of defective units produced needed to be reduced dramatically. Thus, Maria decided to pursue a quality-driven turnaround strategy. Revenue growth and cost reduction could both be achieved if quality could be improved. By growing revenues and decreasing costs, profitability could be increased. After meeting with the managers of production, marketing, purchasing, and human resources, Maria made the following decisions, effective immediately (end of November 20x1): a. More will be invested in employee training. Workers will be trained to detect quality problems and empowered to make improvements. Workers will be allowed a bonus of 10 percent of any cost savings produced by their suggested improvements. b. Two design engineers will be hired immediately, with expectations of hiring one or two more within a year. These engineers will be in charge of redesigning processes and products with the objective of improving quality. They will also be given the responsibility of working with selected suppliers to help improve the quality of their products and processes. Design engineers were considered a strategic necessity. c. Implement a new process: evaluation and selection of suppliers. This new process has the objective of selecting a group of suppliers that are willing and capable of providing nondefective components. d. Effective immediately, the division will begin inspecting purchased components. According to production, many of the quality problems are caused by defective components purchased from outside suppliers. Incoming inspection is viewed as a transitional activity. Once the division has developed a group of suppliers capable of delivering nondefective components, this activity will be eliminated. e. Within three years, the goal is to produce products with a defect rate less than 0.10 percent. By reducing the defect rate to this level, marketing is confident that market share will increase by at least 50 percent (as a consequence of increased customer satisfaction). Products with better quality will help establish an improved product image and reputation, allowing the division to capture new customers and increase market share. f. Accounting will be given the charge to install a quality information reporting system. Daily reports on operational quality data (e.g., percentage of defective units), weekly updates of trend graphs (posted throughout the division), and quarterly cost reports are the types of information required. g. To help direct the improvements in quality activities, kaizen costing is to be implemented. For example, for the year 20x1, a kaizen standard of 6 percent of the selling price per unit was set for rework costs, a 25 percent reduction from the current actual cost. To ensure that the quality improvements were directed and translated into concrete financial outcomes, Maria also began to implement a Balanced Scorecard for the division. By the end of 20x2, progress was being made. Sales had increased to 26,000,000, and the kaizen improvements were meeting or beating expectations. For example, rework costs had dropped to 1,500,000. At the end of 20x3, two years after the turnaround quality strategy was implemented, Maria received the following quality cost report: Maria also received an income statement for 20x3: Maria was pleased with the outcomes. Revenues had grown, and costs had been reduced by at least as much as she had projected for the two-year period. Growth next year should be even greater as she was beginning to observe a favorable effect from the higher-quality products. Also, further quality cost reductions should materialize as incoming inspections were showing much higher-quality purchased components. Required: 1. Identify the strategic objectives, classified by the Balanced Scorecard perspective. Next, suggest measures for each objective. 2. Using the results from Requirement 1, describe Marias strategy using a series of if-then statements. Next, prepare a strategy map. 3. Explain how you would evaluate the success of the quality-driven turnaround strategy. What additional information would you like to have for this evaluation? 4. Explain why Maria felt that the Balanced Scorecard would increase the likelihood that the turnaround strategy would actually produce good financial outcomes. 5. Advise Maria on how to encourage her employees to align their actions and behavior with the turnaround strategy.Salem Electronics currently produces two products: a programmable calculator and a tape recorder. A recent marketing study indicated that consumers would react favorably to a radio with the Salem brand name. Owner Kenneth Booth was interested in the possibility. Before any commitment was made, however, Kenneth wanted to know what the incremental fixed costs would be and how many radios must be sold to cover these costs. In response, Betty Johnson, the marketing manager, gathered data for the current products to help in projecting overhead costs for the new product. The overhead costs based on 30,000 direct labor hours follow. (The high-low method using direct labor hours as the independent variable was used to determine the fixed and variable costs.) All depreciation. The following activity data were also gathered: Betty was told that a plantwide overhead rate was used to assign overhead costs based on direct labor hours. She was also informed by engineering that if 20,000 radios were produced and sold (her projection based on her marketing study), they would have the same activity data as the recorders (use the same direct labor hours, machine hours, setups, and so on). Engineering also provided the following additional estimates for the proposed product line: Upon receiving these estimates, Betty did some quick calculations and became quite excited. With a selling price of 26 and just 18,000 of additional fixed costs, only 4,500 units had to be sold to break even. Since Betty was confident that 20,000 units could be sold, she was prepared to strongly recommend the new product line. Required: 1. Reproduce Bettys break-even calculation using conventional cost assignments. How much additional profit would be expected under this scenario, assuming that 20,000 radios are sold? 2. Use an activity-based costing approach, and calculate the break-even point and the incremental profit that would be earned on sales of 20,000 units. 3. Explain why the CVP analysis done in Requirement 2 is more accurate than the analysis done in Requirement 1. What recommendation would you make?Kimball Company has developed the following cost formulas: Materialusage:Ym=80X;r=0.95Laborusage(direct):Yl=20X;r=0.96Overheadactivity:Yo=350,000+100X;r=0.75Sellingactivity:Ys=50,000+10X;r=0.93 where X=Directlaborhours The company has a policy of producing on demand and keeps very little, if any, finished goods inventory (thus, units produced equals units sold). Each unit uses one direct labor hour for production. The president of Kimball Company has recently implemented a policy that any special orders will be accepted if they cover the costs that the orders cause. This policy was implemented because Kimballs industry is in a recession and the company is producing well below capacity (and expects to continue doing so for the coming year). The president is willing to accept orders that minimally cover their variable costs so that the company can keep its employees and avoid layoffs. Also, any orders above variable costs will increase overall profitability of the company. Required: 1. Compute the total unit variable cost. Suppose that Kimball has an opportunity to accept an order for 20,000 units at 220 per unit. Should Kimball accept the order? (The order would not displace any of Kimballs regular orders.) 2. Explain the significance of the coefficient of correlation measures for the cost formulas. Did these measures have a bearing on your answer in Requirement 1? Should they have a bearing? Why or why not? 3. Suppose that a multiple regression equation is developed for overhead costs: Y = 100,000 + 100X1 + 5,000X2 + 300X3, where X1 = direct labor hours, X2 = number of setups, and X3 = engineering hours. The coefficient of determination for the equation is 0.94. Assume that the order of 20,000 units requires 12 setups and 600 engineering hours. Given this new information, should the company accept the special order referred to in Requirement 1? Is there any other information about cost behavior that you would like to have? Explain.

- Leather Works is a family-owned maker of leather travel bags and briefcases located in the northeastern part of the United States. Foreign competition has forced its owner, Heather Gray, to explore new ways to meet the competition. One of her cousins, Wallace Hayes, who recently graduated from college with a major in accounting, told her about the use of cost variance analysis to learn about efficiencies of production. In May of last year, Heather asked Matt Jones, chief accountant, and Alfred Prudest, production manager, to implement a standard costing system. Matt and Alfred, in turn, retained Shannon Leikam, an accounting professor at Hardings College, to set up a standard costing system by using information supplied to her by Matts and Alfreds staff. To verify that the information was accurate, Shannon visited the plant and measured workers output using time and motion studies. During those visits, she was not accompanied by either Matt or Alfred, and the workers knew about Shannons schedule in advance. The cost system was implemented in June of last year. Recently, the following dialogue took place among Heather, Matt, and Alfred: HEATHER: How is the business performing? ALFRED: You know, we are producing a lot more than we used to, thanks to the contract that you helped obtain from Lean, Inc., for laptop covers. (Lean is a national supplier of computer accessories.) MATT: Thank goodness for that new product. It has kept us from sinking even more due to the inroads into our business made by those foreign suppliers of leather goods. HEATHER: What about the standard costing system? MATT: The variances are mostly favorable, except for the first few months when the supplier of leather started charging more. HEATHER: How did the union members take to the standards? ALFRED: Not bad. They grumbled a bit at first, but they have taken it in stride. Weve consistently shown favorable direct labor efficiency variances and direct materials usage variances. The direct labor rate variance has been flat. MATT: It should be since direct labor rates are negotiated by the union representative at the start of the year and remain the same for the entire year. HEATHER: Matt, would you send me the variance report for laptop covers immediately? The following chart summarizes the direct materials and direct labor variances from November of last year through April of this year (extracted from the report provided by Matt). Standards for each laptop cover are as follows: a. Three feet of direct materials at 7.50 per foot b. Forty-five minutes of direct labor at 14 per hour In addition, the data for May of this year, but not the variances for the month, are as follows: Actual direct labor cost per hour exceeded the budgeted rate by 0.10 per hour. Required: 1. For May of this year, calculate the price and quantity variances for direct labor and direct materials. 2. Discuss the trend of the direct materials and labor variances. 3. What type of actions must the workers have taken during the period they were being observed for the setting of standards? 4. What can be done to ensure that the standards are set correctly? (CMA adapted)Bienestar, Inc., has two plants that manufacture a line of wheelchairs. One is located in Kansas City, and the other in Tulsa. Each plant is set up as a profit center. During the past year, both plants sold their tilt wheelchair model for 1,620. Sales volume averages 20,000 units per year in each plant. Recently, the Kansas City plant reduced the price of the tilt model to 1,440. Discussion with the Kansas City manager revealed that the price reduction was possible because the plant had reduced its manufacturing and selling costs by reducing what was called non-value-added costs. The Kansas City manufacturing and selling costs for the tilt model were 1,260 per unit. The Kansas City manager offered to loan the Tulsa plant his cost accounting manager to help it achieve similar results. The Tulsa plant manager readily agreed, knowing that his plant must keep pacenot only with the Kansas City plant but also with competitors. A local competitor had also reduced its price on a similar model, and Tulsas marketing manager had indicated that the price must be matched or sales would drop dramatically. In fact, the marketing manager suggested that if the price were dropped to 1,404 by the end of the year, the plant could expand its share of the market by 20 percent. The plant manager agreed but insisted that the current profit per unit must be maintained. He also wants to know if the plant can at least match the 1,260 per-unit cost of the Kansas City plant and if the plant can achieve the cost reduction using the approach of the Kansas City plant. The plant controller and the Kansas City cost accounting manager have assembled the following data for the most recent year. The actual cost of inputs, their value-added (ideal) quantity levels, and the actual quantity levels are provided (for production of 20,000 units). Assume there is no difference between actual prices of activity units and standard prices. Required: 1. Calculate the target cost for expanding the Tulsa plants market share by 20 percent, assuming that the per-unit profitability is maintained as requested by the plant manager. 2. Calculate the non-value-added cost per unit. Assuming that non-value-added costs can be reduced to zero, can the Tulsa plant match the Kansas City per-unit cost? Can the target cost for expanding market share be achieved? What actions would you take if you were the plant manager? 3. Describe the role that benchmarking played in the effort of the Tulsa plant to protect and improve its competitive position.Tonya Martin, CMA and controller or the Parts Division of Gunderson Inc., was meeting with Doug Adams, manager of the division. The topic of discussion was the assignment of overhead costs to jobs and their impact on the divisions pricing decisions. Their conversation was as follows: Tonya: Doug, as you know, about 25% of our business is based on government contracts, with the other 75% based on jobs from private sources won through bidding. During the last several years, our private business has declined. We have been losing more bids than usual. After some careful investigation, I have concluded that we are overpricing some jobs because of improper assignment of overhead costs. Some jobs are also being underpriced. Unfortunately, the jobs being overpriced are coming from our higher-volume, labor-intensive products, so we are losing business. Dong: I think I understand. Jobs associated with our high-volume products are being assigned more overhead than they should be receiving. Then when we add our standard 40% markup, we end up with a higher price than our competitors, who assign costs more accurately. Tonya: Exactly. We have two producing departments, one labor-intensive and the other machine-intensive. The labor-intensive department generates much less overhead than the machine-intensive department. Furthermore, virtually all of our high-volume jobs are labor-intensive. We have been using a plantwide rate based on direct labor hours to assign overhead to all jobs. As a result, the high-volume, labor-intensive jobs receive a greater share of the machine-intensive departments overhead than they deserve. This problem can be greatly alleviated by switching to departmental overhead rates. For example, an average high-volume job would be assigned 100,000 of overhead using a plantwide rate and only 70,000 using departmental rates. The change would lower our bidding price on high-volume jobs by an average of 42,000 per job. By increasing the accuracy of our product costing, we can make better pricing decisions and win back much of our private-sector business. Doug: Sounds good. When can you implement the change in overhead rates? Tonya: It wont take long. I can have the new system working within four to six weekscertainly by the start of the new fiscal year. Doug: Hold it. I just thought of a possible complication. As I recall, most of our government contract work is done in the labor-intensive department. This new overhead assignment scheme will push down the cost on the government jobs, and we will lose revenues. They pay us full cost plus our standard markup. This business is not threatened by our current costing procedures, but we cant switch our rates for only the private business. Government auditors would question the lack of consistency in our costing procedures. Tonya: You do have a point. I thought of this issue also. According to my estimates, we will gain more revenues from the private sector than we will lose from our government contracts. Besides, the costs of our government jobs are distorted. In effect, we are overcharging the government. Doug: They dont know that and never would unless we switch our overhead assignment procedures. I think I have the solution. Officially, lets keep our plantwide overhead rate. All of the official records will reflect this overhead costing approach for both our private and government business. Unofficially. I want you to develop a separate set of books that can be used to generate the information we need to prepare competitive bids for our private-sector business. Required: 1. Do you believe that the solution proposed by Doug is ethical? Explain. 2. Suppose that Tonya decides that Dougs solution is not right and objects strongly. Further suppose that, despite Tonyas objections, Doug insists strongly on implementing the action. What should Tonya do?

- Danna Wise, president of Tidwell Company, recently returned from a conference on quality and productivity. At the conference, she was told that many American firms have quality costs totaling 20 to 30% of sales. The quality experts at the conference convinced her that a company could increase its profitability by improving quality. However, she was of the opinion that the quality of Tidwell Company was much less than 20%probably more in the 4 to 6% range. However, because the potential for increasing profits was so great if she was wrong, she decided to request a preliminary estimate of the total quality costs currently being incurred. She asked her controller for a summary of quality costs, with the costs classified into four categories: prevention, appraisal, internal failure, or external failure. She also wanted the costs expressed as a percentage of both sales and profits. The controller had his staff assemble the following information from the past year, 20X1: a. Sales revenue, 37,240,000; net income, 4,000,000. b. During the year, customers returned 40,000 units needing repair. Repair cost averages 9 per unit. c. Twelve inspectors are employed, each earning an annual salary of 80,000. The inspectors are involved only with final inspection (product acceptance). d. Total scrap is 200,000 units. Of this total, ninety percent is quality related. The cost of scrap is about 10 per unit. e. Each year, approximately 800,000 units are rejected in final inspection. Of these units, seventy-five percent can be recovered through rework. The cost of rework is 1.80 per I unit. f. A customer cancelled an order that would have increased profits by 600,000. The customers reason for cancellation was poor product performance. g. The company employs 10 full-time employees in its complaint department. Each earns 48,600 a year. h. The company gave sales allowances totaling 180,000 due to substandard products being sent to the customer. i. The company requires all new employees to take its 4-hour quality training program. The estimated annual cost of the program is 120,000. Required: 1. Prepare a simple quality cost report classifying costs by category. 2. Compute the quality cost-sales ratio. Also, compare the total quality costs with total profits. Should Danna be concerned with the level of quality costs? 3. Prepare a pie chart for the quality costs. Discuss the distribution of quality costs among the four categories. Are they properly distributed? Explain. 4. Discuss how the company can improve its overall quality and at the same time reduce total quality costs. 5. By how much will profits increase if quality costs are reduced to 3% of sales?Bannister Company, an electronics firm, buys circuit boards and manually inserts various electronic devices into the printed circuit board. Bannister sells its products to original equipment manufacturers. Profits for the last two years have been less than expected. Mandy Confer, owner of Bannister, was convinced that her firm needed to adopt a revenue growth and cost reduction strategy to increase overall profits. After a careful review of her firms condition, Mandy realized that the main obstacle for increasing revenues and reducing costs was the high defect rate of her products (a 6 percent reject rate). She was certain that revenues would grow if the defect rate was reduced dramatically. Costs would also decline as there would be fewer rejects and less rework. By decreasing the defect rate, customer satisfaction would increase, causing, in turn, an increase in market share. Mandy also felt that the following actions were needed to help ensure the success of the revenue growth and cost reduction strategy: a. Improve the soldering capabilities by sending employees to an outside course. b. Redesign the insertion process to eliminate some of the common mistakes. c. Improve the procurement process by selecting suppliers that provide higher-quality circuit boards. Required: 1. State the revenue growth and cost reduction strategy using a series of cause-and-effect relationships expressed as if-then statements. 2. Illustrate the strategy using a strategy map. 3. Explain how the revenue growth strategy can be tested. In your explanation, discuss the role of lead and lag measures, targets, and double-loop feedback.Jolene Askew, manager of Feagan Company, has committed her company to a strategically sound cost reduction program. Emphasizing life-cycle cost management is a major part of this effort. Jolene is convinced that production costs can be reduced by paying more attention to the relationships between design and manufacturing. Design engineers need to know what causes manufacturing costs. She instructed her controller to develop a manufacturing cost formula for a newly proposed product. Marketing had already projected sales of 25,000 units for the new product. (The life cycle was estimated to be 18 months. The company expected to have 50 percent of the market and priced its product to achieve this goal.) The projected selling price was 20 per unit. The following cost formula was developed: Y=200,000+10X1 where X1=Machinehours(Theproductisexpectedtouseonemachinehourforeveryunitproduced.) Upon seeing the cost formula, Jolene quickly calculated the projected gross profit to be 50,000. This produced a gross profit of 2 per unit, well below the targeted gross profit of 4 per unit. Jolene then sent a memo to the Engineering Department, instructing them to search for a new design that would lower the costs of production by at least 50,000 so that the target profit could be met. Within two days, the Engineering Department proposed a new design that would reduce unit-variable cost from 10 per machine hour to 8 per machine hour (Design Z). The chief engineer, upon reviewing the design, questioned the validity of the controllers cost formula. He suggested a more careful assessment of the proposed designs effect on activities other than machining. Based on this suggestion, the following revised cost formula was developed. This cost formula reflected the cost relationships of the most recent design (Design Z). Y=140,000+8X1+5,000X2+2,000X3 where X1=MachinehoursX2=NumberofbatchesX3=Numberofengineeringchangeorders Based on scheduling and inventory considerations, the product would be produced in batches of 1,000; thus, 25 batches would be needed over the products life cycle. Furthermore, based on past experience, the product would likely generate about 20 engineering change orders. This new insight into the linkage of the product with its underlying activities led to a different design (Design W). This second design also lowered the unit-level cost by 2 per unit but decreased the number of design support requirements from 20 orders to 10 orders. Attention was also given to the setup activity, and the design engineer assigned to the product created a design that reduced setup time and lowered variable setup costs from 5,000 to 3,000 per setup. Furthermore, Design W also creates excess activity capacity for the setup activity, and resource spending for setup activity capacity can be decreased by 40,000, reducing the fixed cost component in the equation by this amount. Design W was recommended and accepted. As prototypes of the design were tested, an additional benefit emerged. Based on test results, the post-purchase costs dropped from an estimated 0.70 per unit sold to 0.40 per unit sold. Using this information, the Marketing Department revised the projected market share upward from 50 percent to 60 percent (with no price decrease). Required: 1. Calculate the expected gross profit per unit for Design Z using the controllers original cost formula. According to this outcome, does Design Z reach the targeted unit profit? Repeat, using the engineers revised cost formula. Explain why Design Z failed to meet the targeted profit. What does this say about the use of unit-based costing for life-cycle cost management? 2. Calculate the expected profit per unit using Design W. Comment on the value of activity information for life-cycle cost management. 3. The benefit of the post-purchase cost reduction of Design W was discovered in testing. What direct benefit did it create for Feagan Company (in dollars)? Reducing post-purchase costs was not a specific design objective. Should it have been? Are there any other design objectives that should have been considered?

- Kelson Sporting Equipment, Inc., makes two types of baseball gloves: a regular model and a catchers model. The firm has 900 hours of production time available in its cutting and sewing department, 300 hours available in its finishing department, and 100 hours available in its packaging and shipping department. The production time requirements and the profit contribution per glove are given in the following table: Assuming that the company is interested in maximizing the total profit contribution, answer the following: a. What is the linear programming model for this problem? b. Develop a spreadsheet model and find the optimal solution using Excel Solver. How many of each model should Kelson manufacture? c. What is the total profit contribution Kelson can earn with the optimal production quantities? d. How many hours of production time will be scheduled in each department? e. What is the slack time in each department?Jadlow Company produces handcrafted leather purses. Virtually all of the manufacturing cost consists of materials and labor. Over the past several years, profits have been declining because the cost of the two major inputs has been increasing. Janice Jadlow, the president of the company, has indicated that the price of the purses cannot be increased; thus, the only way to improve or at least stabilize profits is to increase overall productivity. At the beginning of 20x2, Janice implemented a new cutting and assembly process that promised less materials waste and a faster production time. At the end of 20x2, Janice wants to know how much profits have changed from the prior year because of the new process. In order to provide this information to Janice, the controller of the company gathered the following data: Required: 1. Compute the productivity profile for each year. Comment on the effectiveness of the new production process. 2. Compute the increase in profits attributable to increased productivity. 3. Calculate the price-recovery component, and comment on its meaning.Boston Executive. Inc., produces executive limousines and currently manufactures the mini-bar inset at these costs: The company received an offer from Elite Mini-Bars to produce the insets for $2,100 per Unit and supply 1,000 mini-bars for the coming years estimated production. If the company accepts this offer and shuts down production of this part of the business, production workers and supervisors will be reassigned to other areas. Assume that for the short-term decision-making process demonstrated in this problem, the companys total labor costs (direct labor and supervisor salaries) will remain the same if the bar inserts are purchased. The specialized equipment cannot be used and has no market value. However, the space occupied by the mini bar production can be used by a different production group that will lease it for $55,000 per year. Should the company make or buy the mini-bar insert?