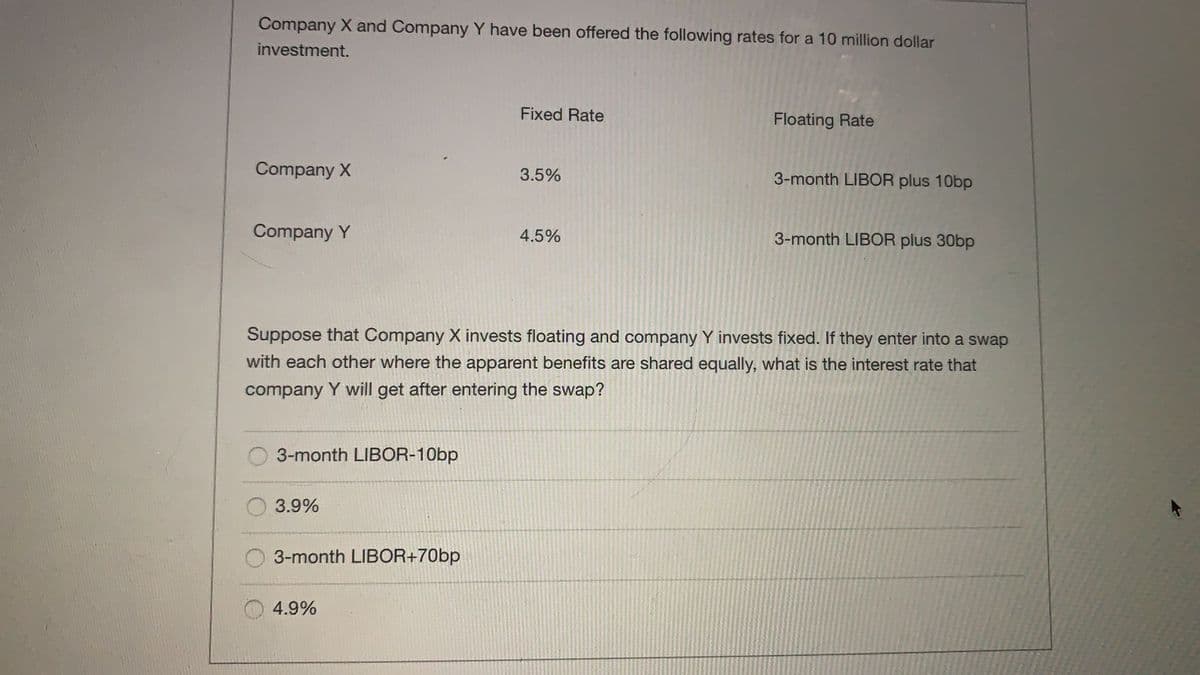

Company X and Company Y have been offered the following rates for a 10 million dollar investment. Fixed Rate Floating Rate Company X 3.5% 3-month LIBOR plus 10bp Company Y 4.5% 3-month LIBOR plus 30bp Suppose that Company X invests floating and company Y invests fixed. If they enter into a swap with each other where the apparent benefits are shared equally, what is the interest rate that company Y will get after entering the swap? 3-month LIBOR-10bp 3.9% 3-month LIBOR+70bp 4.9%

Company X and Company Y have been offered the following rates for a 10 million dollar investment. Fixed Rate Floating Rate Company X 3.5% 3-month LIBOR plus 10bp Company Y 4.5% 3-month LIBOR plus 30bp Suppose that Company X invests floating and company Y invests fixed. If they enter into a swap with each other where the apparent benefits are shared equally, what is the interest rate that company Y will get after entering the swap? 3-month LIBOR-10bp 3.9% 3-month LIBOR+70bp 4.9%

Chapter11: Managing Transaction Exposure

Section: Chapter Questions

Problem 6ST

Related questions

Question

Transcribed Image Text:Company X and Company Y have been offered the following rates for a 10 million dollar

investment.

Fixed Rate

Floating Rate

Company X

3.5%

3-month LIBOR plus 10bp

Company Y

4.5%

3-month LIBOR plus 30bp

Suppose that Company X invests floating and company Y invests fixed. If they enter into a swap

with each other where the apparent benefits are shared equally, what is the interest rate that

company Y will get after entering the swap?

3-month LIBOR-10bp

3.9%

3-month LIBOR+70bp

4.9%

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you