Consider the R output listed below. With this information, answer the following: model.fit=arima(data, order=c(1,0,0),method="ML") model.fit Coefficients: arl intercept 0.4796 179.4921 0.0565 0.4268 sigma2 estimated as 6.495: log likelihood = -126.24, aic= 296.48 s.e. What is the common name for this model? Write down this model. (Write theoretically and also the estimated time series regression from the output). What estimation method is used to estimate this model? Test the null that this series is mean zero (write down the null and alternative hypothesis, test statistic, and decision rule). .Test the null that this series is only a function of white noise sequences (write down the null and alternative hypothesis, test statistic, and decision rule). Suppose we believed these estimates to be the true parameters, draw the autocorrelation function.

Consider the R output listed below. With this information, answer the following: model.fit=arima(data, order=c(1,0,0),method="ML") model.fit Coefficients: arl intercept 0.4796 179.4921 0.0565 0.4268 sigma2 estimated as 6.495: log likelihood = -126.24, aic= 296.48 s.e. What is the common name for this model? Write down this model. (Write theoretically and also the estimated time series regression from the output). What estimation method is used to estimate this model? Test the null that this series is mean zero (write down the null and alternative hypothesis, test statistic, and decision rule). .Test the null that this series is only a function of white noise sequences (write down the null and alternative hypothesis, test statistic, and decision rule). Suppose we believed these estimates to be the true parameters, draw the autocorrelation function.

Managerial Economics: Applications, Strategies and Tactics (MindTap Course List)

14th Edition

ISBN:9781305506381

Author:James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Chapter5: Business And Economic Forecasting

Section: Chapter Questions

Problem 1.6CE: Estimate the double-log (log linear) time trend model for log cruise ship arrivals against log time....

Related questions

Question

Please solve and explain into detial

Q3

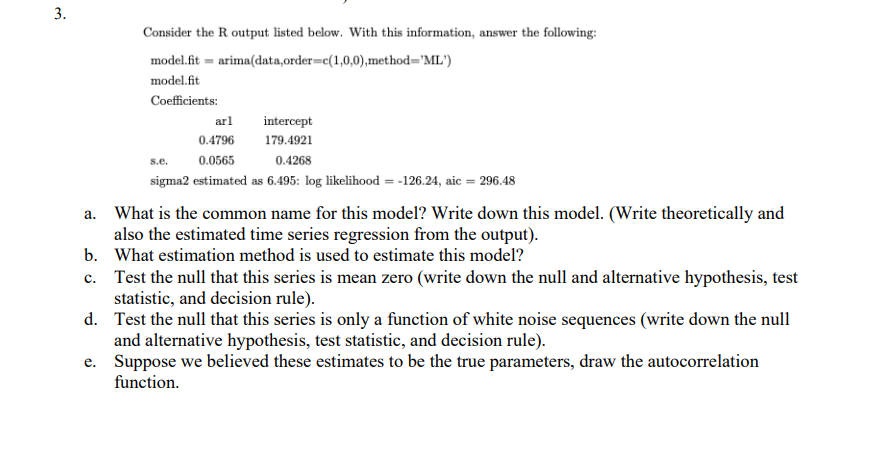

Transcribed Image Text:3.

Consider the R output listed below. With this information, answer the following:

model.fit=arima(data, order=c(1,0,0), method="ML')

model.fit

Coefficients:

arl

intercept

0.4796

179.4921

s.e.

0.0565

0.4268

sigma2 estimated as 6.495: log likelihood= -126.24, aic = 296.48

a. What is the common name for this model? Write down this model. (Write theoretically and

also the estimated time series regression from the output).

What estimation method is used to estimate this model?

b.

c. Test the null that this series is mean zero (write down the null and alternative hypothesis, test

statistic, and decision rule).

d.

Test the null that this series is only a function of white noise sequences (write down the null

and alternative hypothesis, test statistic, and decision rule).

e.

Suppose we believed these estimates to be the true parameters, draw the autocorrelation

function.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 5 steps

Follow-up Questions

Read through expert solutions to related follow-up questions below.

Follow-up Question

Please continue to solve from Part d to Part e. Thank you

Solution

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Managerial Economics: Applications, Strategies an…

Economics

ISBN:

9781305506381

Author:

James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:

Cengage Learning

Managerial Economics: Applications, Strategies an…

Economics

ISBN:

9781305506381

Author:

James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:

Cengage Learning