Consider total cost and total revenue, given in the following table: In the final column, enter profit for each quantity. (Note: If the firm suffers a loss, enter a negative number in the appropriate cell.) Marginal Cost (Dollars) Total Cost Total Revenue Marginal Revenue (Dollars) Profit Quantity (Dollars) (Dollars) (Dollars) 10 14 13 21 4 17 28 24 35 32 42 42 49 In order to maximize profit, how many units should the firm produce? Check all that apply. 6. In the previous table, enter marginal revenue and marginal cost for each quantity. On the following graph, use the green points (triangle symbol) to graph the marginal-revenue curve, then use the orange points (square symbol) to plot the marginal-cost curve. (Note: Be sure to plot from left to right and to plot between integers. For example, if the marginal cost of increasing production from 1 unit to 2 units is $5, then you would plot a point at (1.5, 5).) 10 Marginal Revenue 00 In the previous table, enter marginal revenue and marginal cost for each quantity. On the following graph, use the green points (triangle symbol) to graph the marginal-revenue curve, then use the orange points (square symbol) to plot the marginal-cost curve. (Note: Be sure to plot from left to right and to plot between integers. For example, if the marginal cost of increasing production from 1 unit to 2 units is $5, then you would plot a point at (1.5, 5).) 10 Marginal Revenue Marginal Cost 2 Quantity The marginal-revenue curve and the marginal-cost curve cross at a quantity This firm in a competitive industry, because marginal revenue is as quantity increases. True or False: The industry is in a long-run equilibrium. True False Revenue and C osts

Consider total cost and total revenue, given in the following table: In the final column, enter profit for each quantity. (Note: If the firm suffers a loss, enter a negative number in the appropriate cell.) Marginal Cost (Dollars) Total Cost Total Revenue Marginal Revenue (Dollars) Profit Quantity (Dollars) (Dollars) (Dollars) 10 14 13 21 4 17 28 24 35 32 42 42 49 In order to maximize profit, how many units should the firm produce? Check all that apply. 6. In the previous table, enter marginal revenue and marginal cost for each quantity. On the following graph, use the green points (triangle symbol) to graph the marginal-revenue curve, then use the orange points (square symbol) to plot the marginal-cost curve. (Note: Be sure to plot from left to right and to plot between integers. For example, if the marginal cost of increasing production from 1 unit to 2 units is $5, then you would plot a point at (1.5, 5).) 10 Marginal Revenue 00 In the previous table, enter marginal revenue and marginal cost for each quantity. On the following graph, use the green points (triangle symbol) to graph the marginal-revenue curve, then use the orange points (square symbol) to plot the marginal-cost curve. (Note: Be sure to plot from left to right and to plot between integers. For example, if the marginal cost of increasing production from 1 unit to 2 units is $5, then you would plot a point at (1.5, 5).) 10 Marginal Revenue Marginal Cost 2 Quantity The marginal-revenue curve and the marginal-cost curve cross at a quantity This firm in a competitive industry, because marginal revenue is as quantity increases. True or False: The industry is in a long-run equilibrium. True False Revenue and C osts

Managerial Economics: A Problem Solving Approach

5th Edition

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Chapter3: Benefits, Costs, And Decisions

Section: Chapter Questions

Problem 9MC

Related questions

Question

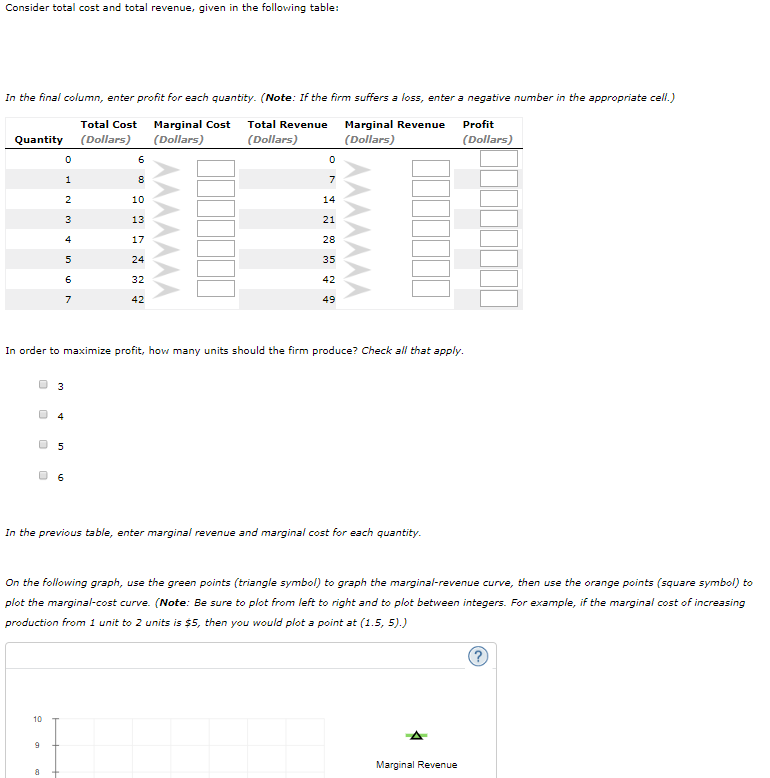

Transcribed Image Text:Consider total cost and total revenue, given in the following table:

In the final column, enter profit for each quantity. (Note: If the firm suffers a loss, enter a negative number in the appropriate cell.)

Marginal Cost

(Dollars)

Total Cost

Total Revenue

Marginal Revenue

(Dollars)

Profit

Quantity

(Dollars)

(Dollars)

(Dollars)

10

14

13

21

4

17

28

24

35

32

42

42

49

In order to maximize profit, how many units should the firm produce? Check all that apply.

6.

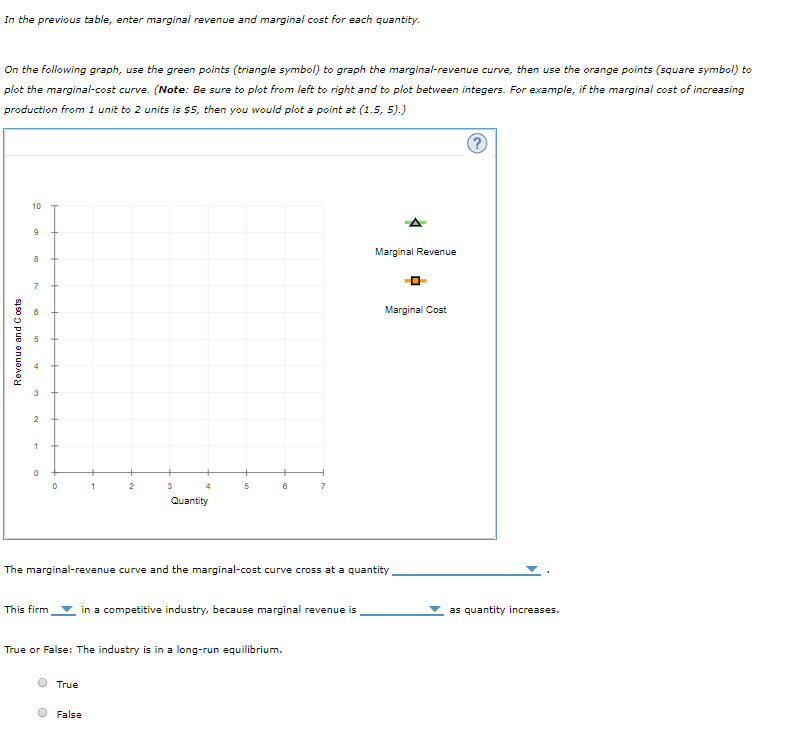

In the previous table, enter marginal revenue and marginal cost for each quantity.

On the following graph, use the green points (triangle symbol) to graph the marginal-revenue curve, then use the orange points (square symbol) to

plot the marginal-cost curve. (Note: Be sure to plot from left to right and to plot between integers. For example, if the marginal cost of increasing

production from 1 unit to 2 units is $5, then you would plot a point at (1.5, 5).)

10

Marginal Revenue

00

Transcribed Image Text:In the previous table, enter marginal revenue and marginal cost for each quantity.

On the following graph, use the green points (triangle symbol) to graph the marginal-revenue curve, then use the orange points (square symbol) to

plot the marginal-cost curve. (Note: Be sure to plot from left to right and to plot between integers. For example, if the marginal cost of increasing

production from 1 unit to 2 units is $5, then you would plot a point at (1.5, 5).)

10

Marginal Revenue

Marginal Cost

2

Quantity

The marginal-revenue curve and the marginal-cost curve cross at a quantity

This firm

in a competitive industry, because marginal revenue is

as quantity increases.

True or False: The industry is in a long-run equilibrium.

True

False

Revenue and C osts

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 3 images

Recommended textbooks for you

Managerial Economics: A Problem Solving Approach

Economics

ISBN:

9781337106665

Author:

Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:

Cengage Learning

Managerial Economics: Applications, Strategies an…

Economics

ISBN:

9781305506381

Author:

James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:

Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:

9781337106665

Author:

Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:

Cengage Learning

Managerial Economics: Applications, Strategies an…

Economics

ISBN:

9781305506381

Author:

James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:

Cengage Learning