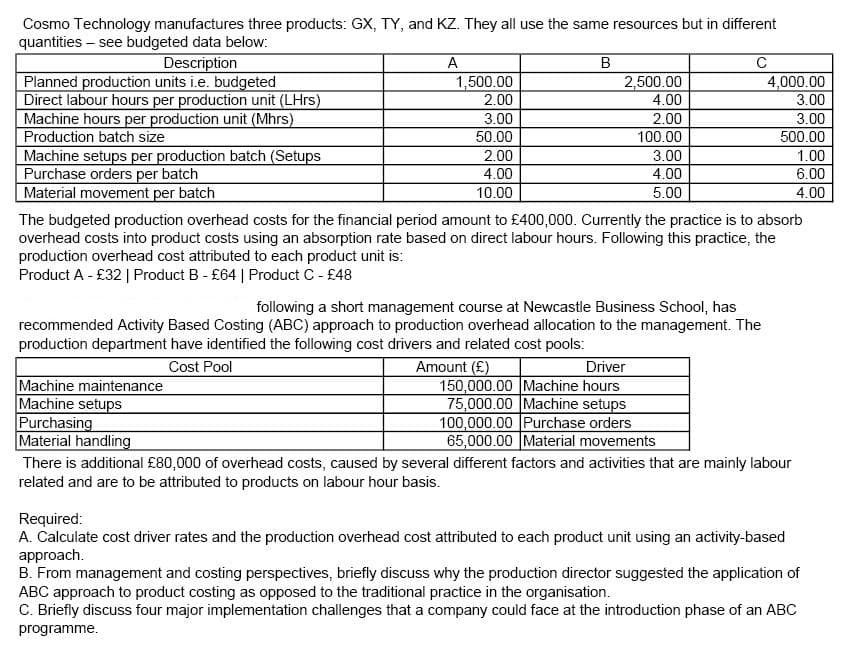

Cosmo Technology manufactures three products: GX, TY, and KZ. They all use the same resources but in different quantities – see budgeted data below: Description B 2,500.00 4.00 C 4,000.00 3.00 3.00 500.00 A Planned production units i.e. budgeted Direct labour hours per production unit (LHrs) Machine hours per production unit (Mhrs) Production batch size Machine setups per production batch (Setups Purchase orders per batch Material movement per batch 1,500.00 2.00 3.00 50.00 2.00 4.00 2.00 100.00 3.00 4.00 5.00 1.00 6.00 10.00 4.00 The budgeted production overhead costs for the financial period amount to £400,000. Currently the practice is to absorb overhead costs into product costs using an absorption rate based on direct labour hours. Following this practice, the production overhead cost attributed to each product unit is: Product A - £32 | Product B - £64 | Product C - £48 following a short management course at Newcastle Business School, has recommended Activity Based Costing (ABC) approach to production overhead allocation to the management. The production department have identified the following cost drivers and related cost pools: Driver 150,000.00 Machine hours 75,000.00 Machine setups 100,000.00 Purchase orders 65,000.00 Material movements Cost Pool Amount (£) Machine maintenance Machine setups Purchasing Material handling There is additional £80,000 of overhead costs, caused by several different factors and activities that are mainly labour related and are to be attributed to products on labour hour basis. Required: A. Calculate cost driver rates and the production overhead cost attributed to each product unit using an activity-based approach. B. From management and costing perspectives, briefly discuss why the production director suggested the application of ABC approach to product costing as opposed to the traditional practice in the organisation. C. Briefly discuss four major implementation challenges that a company could face at the introduction phase of an ABC programme.

Master Budget

A master budget can be defined as an estimation of the revenue earned or expenses incurred over a specified period of time in the future and it is generally prepared on a periodic basis which can be either monthly, quarterly, half-yearly, or annually. It helps a business, an organization, or even an individual to manage the money effectively. A budget also helps in monitoring the performance of the people in the organization and helps in better decision-making.

Sales Budget and Selling

A budget is a financial plan designed by an undertaking for a definite period in future which acts as a major contributor towards enhancing the financial success of the business undertaking. The budget generally takes into account both current and future income and expenses.

Step by step

Solved in 5 steps