Principles of Cost Accounting

17th Edition

ISBN: 9781305087408

Author: Edward J. Vanderbeck, Maria R. Mitchell

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 7, Problem 8P

Preparing a performance report

Use the flexible budget prepared in P7-6 for the 29,000-unit level of activity and the actual operating results listed below for the 29,000- unit level.

Required:

- 1. Prepare a performance report.

- 2. List the major reasons why the actual operating income at 29,000 units differs from the

master budget operating income at 30,000 units in Figure 7-12. - 3. Given the level at which the company operated, how was its cost control?

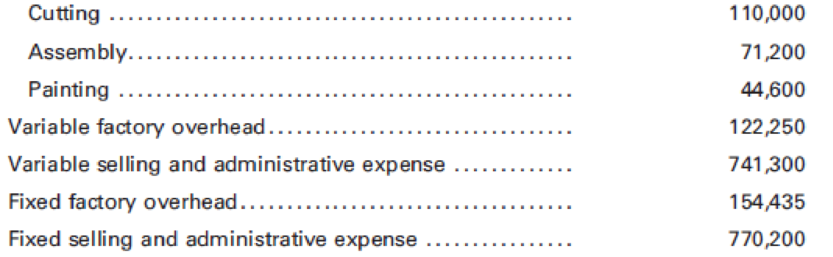

Item

Direct materials:

Direct labor:

Expert Solution & Answer

Trending nowThis is a popular solution!

Chapter 7 Solutions

Principles of Cost Accounting

Ch. 7 - Prob. 1QCh. 7 - Prob. 2QCh. 7 - Prob. 3QCh. 7 - Prob. 4QCh. 7 - Explain zero-based budgeting and how it differs...Ch. 7 - Prob. 6QCh. 7 - Which operating budget must be prepared before the...Ch. 7 - Prob. 8QCh. 7 - Why is it important to have front-line managers...Ch. 7 - If the sales forecast estimates that 50,000 units...

Ch. 7 - What are the advantages and disadvantages of each...Ch. 7 - What three operating budgets can be prepared...Ch. 7 - Prob. 13QCh. 7 - What are the three budgets that are needed in...Ch. 7 - Why might Web-based budgeting be more useful than...Ch. 7 - What is a flexible budget?Ch. 7 - Why is a flexible budget better than a master...Ch. 7 - Why is it important to distinguish between...Ch. 7 - Why is the concept of relevant range important...Ch. 7 - In comparing actual sales revenue to flexible...Ch. 7 - How would you define the following? a. Theoretical...Ch. 7 - Is it possible for a factory to operate at more...Ch. 7 - If a factory operates at 100% of capacity one...Ch. 7 - How is the standard cost per unit for factory...Ch. 7 - When allocating service department costs to...Ch. 7 - The sales department of Macro Manufacturing Co....Ch. 7 - The sales department of F. Pollard Manufacturing...Ch. 7 - Barnes Manufacturing Co. forecast October sales to...Ch. 7 - Prepare a cost of goods sold budget for the Crest...Ch. 7 - Prepare a cost of goods sold budget for MacLaren...Ch. 7 - Roman Inc. has the following totals from its...Ch. 7 - Starburst Inc. has the following items and amounts...Ch. 7 - Using the following per-unit and total amounts,...Ch. 7 - Cortez Manufacturing, Inc. has the following...Ch. 7 - Prob. 10ECh. 7 - Prob. 11ECh. 7 - Prob. 12ECh. 7 - Prob. 13ECh. 7 - Calculating factory overhead The normal capacity...Ch. 7 - The Sales Department of Minimus Inc. has forecast...Ch. 7 - Sales, production, direct materials, direct labor,...Ch. 7 - Budgeted selling and administrative expenses for...Ch. 7 - Prob. 4PCh. 7 - Selling and administrative expense budget and...Ch. 7 - Preparing a flexible budget Use the information in...Ch. 7 - Preparing a performance report Use the flexible...Ch. 7 - Preparing a performance report Use the flexible...Ch. 7 - Flexible budget for factory overhead Presented...Ch. 7 - Prob. 10PCh. 7 - Overhead application rate Creole Manufacturing...Ch. 7 - Overhead application rate Roll Tide Manufacturing...Ch. 7 - Flexible budgeting, performance measurement, and...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Preparing a performance report Use the flexible budget prepared in P7-6 for the 31,000-unit level and the actual operating results listed below for the 31,000-unit level. Required: 1. Prepare a performance report. 2. List the major reasons why the actual operating income at 31,000 units differs from the master budget operating income at 30,000 units in Figure 7-12. 3. Given the level at which the company operated, how was its cost control? Item Direct materials: Direct labor:arrow_forwardPerformance Report Based on Budgeted and Actual Levels of Production Balboa Company budgeted production of 4,500 units with the following amounts: At the end of the year, Balboa had the following actual costs for production of 4,700 units: Required: 1. Calculate the budgeted amounts for each cost category listed above for the 4,500 budgeted units. 2. Prepare a performance report using a budget based on expected (budgeted) production of 4,500 units. 3. Prepare a performance report using a budget based on the actual level of production of 4,700 units.arrow_forwardPerformance Report Based on Budgeted and Actual Levels of Production Bowling Company budgeted the following amounts: At the end of the year, Bowling had the following actual costs for production of 3,800 units: Required: 1. Calculate the budgeted amounts for each cost category listed above for the 4,000 budgeted units. 2. Prepare a performance report using a budget based on expected production of 4,000 units. 3. Prepare a performance report using a budget based on the actual level of production of 3,800 units.arrow_forward

- Determining Budgeted Overhead The overhead application rate for a company is 10 per unit, made up of 6 per unit of fixed overhead and 4 per unit of variable overhead. Normal capacity is 10,000 units. In one month there was a favorable flexible budget variance of 2,500. Actual overhead for the month was 110,000 and actual units produced were 13,125. Based on this information, determine the amount of the budgeted overhead for the actual level of production.arrow_forwardFlexible budget for factory overhead Presented below are the monthly factory overhead cost budget (at normal capacity of 5,000 units or 20,000 direct labor hours) and the production and cost data for a month. The predetermined overhead rate is based on normal capacity. Required: 1. Assuming that variable costs will vary in direct proportion to the change in volume, prepare a flexible budget for production levels of 80%, 90%, and 110% of normal capacity. Also determine the predetermined factory overhead rate at each level of volume in both units and direct labor hours. 2. Prepare a flexible budget for production levels of 80%, 90%, and 110%, assuming that variable costs will vary in direct proportion to the change in volume, but with the following exceptions. (Hint: Set up a third category for semi-variable expenses.) a. At 110% of capacity, another supervisor will be needed at a salary of 24,000 annually. b. At 80% of capacity, the repairs expense will drop to one-half of the amount at 100% capacity. c. At 80% of capacity, one part-time maintenance worker, earning 10,000 a year, will be laid off. d. At 110% of capacity, a machine not normally in use and on which no depreciation is normally recorded will be used in production. Its cost was 12,000, it has a 10-year life, and straight-line depreciation will be taken.arrow_forwardAt the beginning of the period, the Fabricating Department budgeted direct labor of 72,000 and equipment depreciation of 18,500 for 2,400 hours of production. The department actually completed 2,350 hours of production. Determine the budget for the department, assuming that it uses flexible budgeting.arrow_forward

- Prepare a flexible budgeted income statement for 47,000 units using the following information from a static budget for 45,000 units:arrow_forwardPrepare a flexible budgeted income for 120,000 units using the following information from a static budget for 100,000 units:arrow_forwardBefore the year began, the following static budget was developed for the estimated sales of 100,000. Sales are sluggish and management needs to revise its budget. Use this information to prepare a flexible budget for 80,000 and 90,000 units of sales.arrow_forward

- Static budget versus flexible budget The production supervisor of the Machining Department for Hagerstown Company agreed to the following monthly static budget for the upcoming year: The actual amount spent and the actual units produced in the first three months in the Machining Department were as follows: The Machining Department supervisor has been very pleased with this performance because actual expenditures for May-July have been significantly less than the monthly static budget of2,358,000. However, the plant manager believes that the budget should not remain fixed for every month but should flex or adjust to the volume of work that is produced in the Machining Department. Additional budget information for the Machining Department is as follows: a. Prepare a flexible budget for the actual units produced for May, June, and July in the MachiningDepartment. Assume depreciation is a fixed cost. b. Compare the flexible budget with the actual expenditures for the first three months.What does this comparison suggest?arrow_forwardJudges Gavel uses this information when preparing their flexible budget: direct materials of $3 per unit, direct labor of $2.50 per unit, and manufacturing overhead of $1.25 per unit. Fixed costs are $49,000. What would be the budgeted amounts for 33,000 and 35,000 units?arrow_forwardBudgeted income statement and supporting budgets The budget director of Jupiter Helmets Inc., with the assistance of the controller, treasurer, production manager, and sales manager, has gathered the following data for use in developing the budgeted income statement for May: Prepare a cost of goods sold budget for May. Work in process at the beginning of May is estimated to be $4200. and work in process at the end of May is desired to be $3800.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Survey of Accounting (Accounting I)

Accounting

ISBN:9781305961883

Author:Carl Warren

Publisher:Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:9781947172609

Author:OpenStax

Publisher:OpenStax College

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

Cost control, Why cost control is necessary for a business?; Author: Educationleaves;https://www.youtube.com/watch?v=yMg3gJx48Fg;License: Standard youtube license