Data table Static budget variable overhead 7,800 Static budget fixed overhead %24 3,900 Static budget direct labor hours 1,300 hours Static budget number of units 5,200 units Watson allocates manufacturing overhead to production based on standard direct labor hours. Last month, Watson reported the following actual results: actual variable overhead, $10,500; actual fixed overhead, $2,770; actual production of 6,800 units at 0.30 direct labor hours per unit. The standard direct labor time is 0.25 direct labor hours per unit (1,300 static direct labor hours / 5,200 static units). %24

Data table Static budget variable overhead 7,800 Static budget fixed overhead %24 3,900 Static budget direct labor hours 1,300 hours Static budget number of units 5,200 units Watson allocates manufacturing overhead to production based on standard direct labor hours. Last month, Watson reported the following actual results: actual variable overhead, $10,500; actual fixed overhead, $2,770; actual production of 6,800 units at 0.30 direct labor hours per unit. The standard direct labor time is 0.25 direct labor hours per unit (1,300 static direct labor hours / 5,200 static units). %24

Managerial Accounting

15th Edition

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:Carl Warren, Ph.d. Cma William B. Tayler

Chapter9: Evaluating Variances From Standard Costs

Section: Chapter Questions

Problem 3PB: Direct materials, direct labor, and factory overhead cost variance analysis Road Gripper Tire Co....

Related questions

Concept explainers

Variance Analysis

In layman's terms, variance analysis is an analysis of a difference between planned and actual behavior. Variance analysis is mainly used by the companies to maintain a control over a business. After analyzing differences, companies find the reasons for the variance so that the necessary steps should be taken to correct that variance.

Standard Costing

The standard cost system is the expected cost per unit product manufactured and it helps in estimating the deviations and controlling them as well as fixing the selling price of the product. For example, it helps to plan the cost for the coming year on the various expenses.

Topic Video

Question

Transcribed Image Text:Requirements

1.

Compute the overhead variances for the month: variable overhead cost variance, variable overhead efficiency variance, fixed overhead cost variance, and fixed overhead volume variance.

Explain why the variances are favorable or unfavorable.

2.

Requirement 1. Compute the overhead variances for the month: variable overhead cost variance, variable overhead efficiency variance, foxed overhead cost variance, and foxed overhead volume variance.

Begin by selecting the formulas needed to compute the variable overhead (VOH) and fioxed overhead (FOH) variances, and then compute each variance amount.

Actual overhead - (Actual hours x Standard price)

(Actual hours - Standard hours allowed) x Standard price

Actual overhead - Budgeted overhead

Budgeted overhead - Allocated overhead

= VOH cost variance

%3D

Data Table

= VOH efficiency variance

%3D

|= FOH cost variance

= FOH volume variance

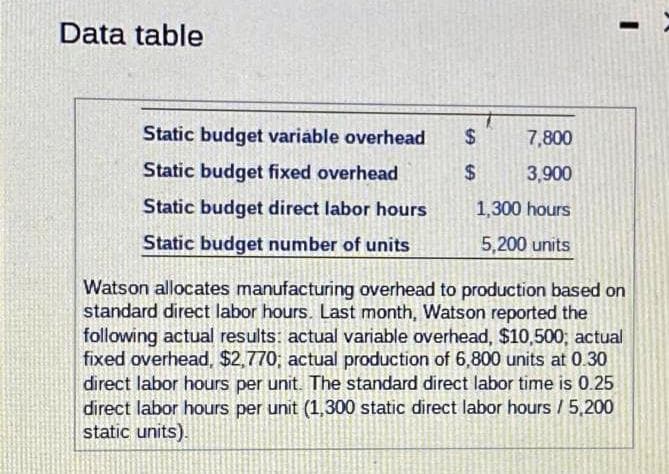

Transcribed Image Text:Data table

Static budget variáble overhead

7,800

Static budget fixed overhead

$4

3,900

Static budget direct labor hours

1,300 hours

Static budget number of units

5,200 units

Watson allocates manufacturing overhead to production based on

standard direct labor hours. Last month, Watson reported the

following actual results: actual variable overhead, $10,500; actual

fixed overhead, $2,770; actual production of 6,800 units at 0.30

direct labor hours per unit. The standard direct labor time is 0.25

direct labor hours per unit (1,300 static direct labor hours / 5,200

static units).

%24

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Excel Applications for Accounting Principles

Accounting

ISBN:

9781111581565

Author:

Gaylord N. Smith

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College