For each of the wages listed in the following table, determine the quantity of labor demanded, the quantity of labor supplied, and the direction of pressure exerted on wages in the absence of any price controls. Wage Labor Demanded Labor Supplied (Dollars per hour) (Thousands of workers) (Thousands of workers) 8 12 Surplus or Shortage of Labor O True Pressure on Wages Upward True or False: A minimum wage below $10 per hour is a binding minimum wage in this market. (Hint: Economists call a n Downward that prevents the labor market from reaching equilibrium a binding minimum wage.)

For each of the wages listed in the following table, determine the quantity of labor demanded, the quantity of labor supplied, and the direction of pressure exerted on wages in the absence of any price controls. Wage Labor Demanded Labor Supplied (Dollars per hour) (Thousands of workers) (Thousands of workers) 8 12 Surplus or Shortage of Labor O True Pressure on Wages Upward True or False: A minimum wage below $10 per hour is a binding minimum wage in this market. (Hint: Economists call a n Downward that prevents the labor market from reaching equilibrium a binding minimum wage.)

Chapter11: Labor Markets

Section: Chapter Questions

Problem 1SQP

Related questions

Question

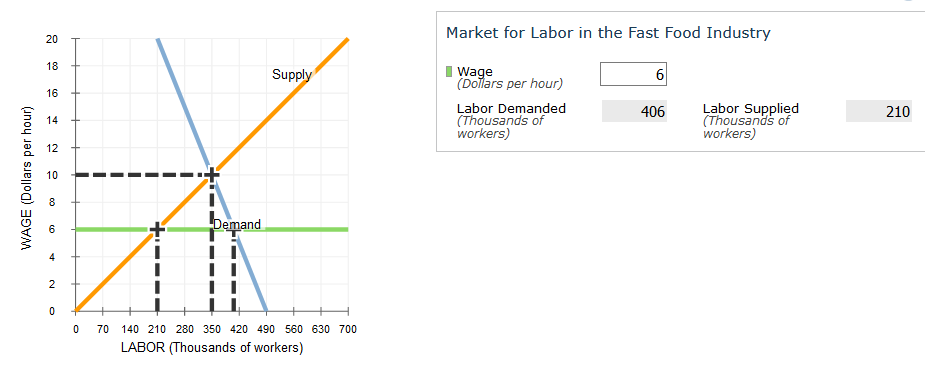

The following graph shows the labor market in the fast-food industry in the fictional town of Supersize City. In a labor market, workers supply their labor to the market in exchange for wages, and their behavior is represented by the supply curve. Similarly, firms pay wages to obtain labor, and thus their behavior is represented by the demand curve. In this way, wages are the price of labor.

(c).

For each of the wages listed in the following table, determine the quantity of labor demanded, the quantity of labor supplied, and the direction of pressure exerted on wages in the absence of any price controls.

(d).

True or False: A minimum wage below $10 per hour is a binding minimum wage in this market. (Hint: Economists call a minimum wage that prevents the labor market from reaching equilibrium a binding minimum wage.)

Transcribed Image Text:For each of the wages listed in the following table, determine the quantity of labor demanded, the quantity of labor supplied, and the direction of

pressure exerted on wages in the absence of any price controls.

Wage

Labor Demanded

Labor Supplied

(Dollars per hour)

(Thousands of workers)

(Thousands of workers)

Surplus or Shortage of Labor

Pressure on Wages

8.

12

Upward

True or False: A minimum wage below $10 per hour is a binding minimum wage in this market. (Hint: Economists callan Downward

that prevents

the labor market from reaching equilibrium a binding minimum wage.)

O True

O False

O O

Transcribed Image Text:Market for Labor in the Fast Food Industry

20

18

I Wage

(Dollars per hour)

Supply

6

16

Labor Demanded

(Thousands of

workers)

Labor Supplied

(Thousands of

workers)

406

210

14

12

10

8

Demand

6

4

2

70

140 210 280 350 420 490 560 630 700

LABOR (Thousands of workers)

WAGE (Dollars per hour)

Expert Solution

Step 1

Equilibrium is set where demand is equal to supply in an economy. A surplus is a situation when the quantity demanded is lower than the quantity supplied in the market. A shortage is a situation when the quantity supplied is less than the quantity demanded.

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Economics Today and Tomorrow, Student Edition

Economics

ISBN:

9780078747663

Author:

McGraw-Hill

Publisher:

Glencoe/McGraw-Hill School Pub Co