From pages 5-1 and 5-3 of the LVN, match the term with its explanation. Put the answers in the right order *The amount of the A/R expected to be collected. * The cost of credit * The amount of the A/R not expected to be collected. * The account recognized when credit sales are recorded. Net Accounts Receivable______ Allowance for Uncollectible Accounts_______ Bad debt expense______ Accounts Receivable______

From pages 5-1 and 5-3 of the LVN, match the term with its explanation. Put the answers in the right order *The amount of the A/R expected to be collected. * The cost of credit * The amount of the A/R not expected to be collected. * The account recognized when credit sales are recorded. Net Accounts Receivable______ Allowance for Uncollectible Accounts_______ Bad debt expense______ Accounts Receivable______

From pages 5-1 and 5-3 of the LVN, match the term with its explanation. Put the answers in the right order *The amount of the A/R expected to be collected. * The cost of credit * The amount of the A/R not expected to be collected. * The account recognized when credit sales are recorded. Net Accounts Receivable______ Allowance for Uncollectible Accounts_______ Bad debt expense______ Accounts Receivable______

From pages 5-1 and 5-3 of the LVN, match the term with its explanation.

Put the answers in the right order

*The amount of the A/R expected to be collected.

* The cost of credit

* The amount of the A/R not expected to be collected.

* The account recognized when credit sales are recorded.

Net Accounts Receivable______

Allowance for Uncollectible Accounts_______

Bad debt expense______

Accounts Receivable______

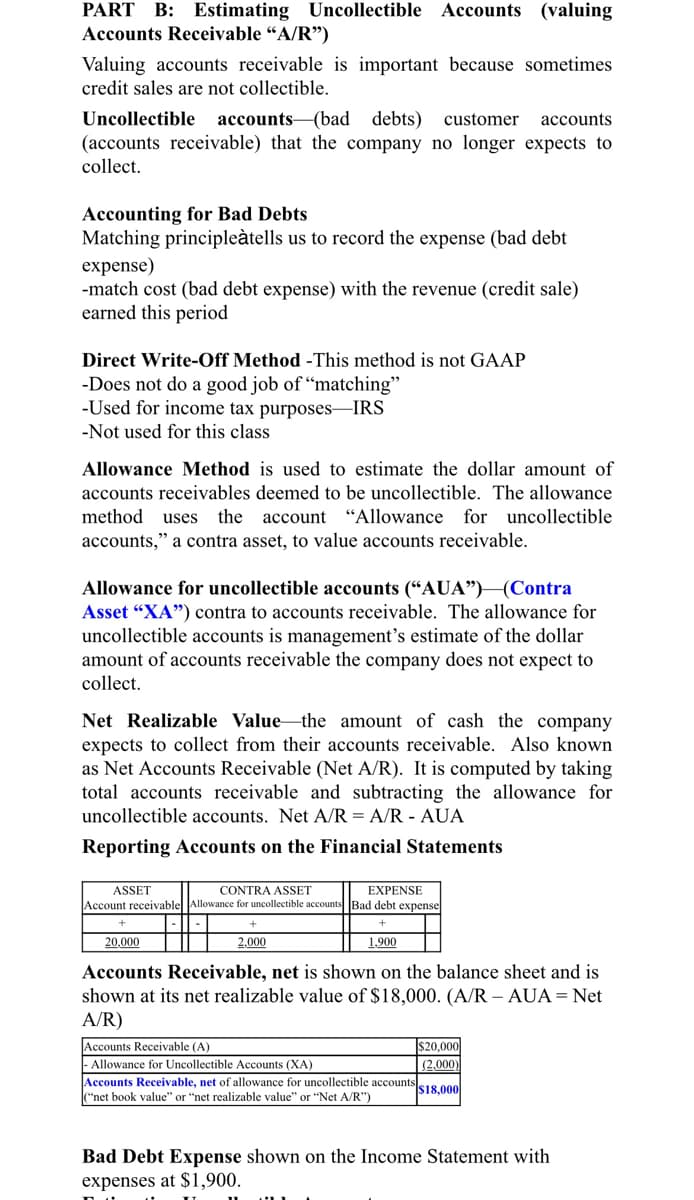

Transcribed Image Text:PART B: Estimating Uncollectible Accounts (valuing

Accounts Receivable “A/R")

Valuing accounts receivable is important because sometimes

credit sales are not collectible.

Uncollectible accounts-(bad

(accounts receivable) that the company no longer expects to

debts)

customer

accounts

collect.

Accounting for Bad Debts

Matching principleàtells us to record the expense (bad debt

expense)

-match cost (bad debt expense) with the revenue (credit sale)

earned this period

Direct Write-Off Method -This method is not GAAP

-Does not do a good job of “matching"

-Used for income tax purposes–IRS

-Not used for this class

Allowance Method is used to estimate the dollar amount of

accounts receivables deemed to be uncollectible. The allowance

method

uses the

account "Allowance for uncollectible

accounts," a contra asset, to value accounts receivable.

Allowance for uncollectible accounts (“AUA")(Contra

Asset “XA") contra to accounts receivable. The allowance for

uncollectible accounts is management's estimate of the dollar

amount of accounts receivable the company does not expect to

collect.

Net Realizable Value the amount of cash the company

expects to collect from their accounts receivable. Also known

as Net Accounts Receivable (Net A/R). It is computed by taking

total accounts receivable and subtracting the allowance for

uncollectible accounts. Net A/R = A/R - AUA

Reporting Accounts on the Financial Statements

EXPENSE

Account receivable Allowance for uncollectible accounts Bad debt expense

ASSET

CONTRA ASSET

20,000

2,000

1,900

Accounts Receivable, net is shown on the balance sheet and is

shown at its net realizable value of $18,000. (A/R – AUA = Net

A/R)

Accounts Receivable (A)

|- Allowance for Uncollectible Accounts (XA)

Accounts Receivable, net of allowance for uncollectible accounts

"net book value" or "net realizable value" or "Net A/R")

$20,000

(2,000)

$18,000

Bad Debt Expense shown on the Income Statement with

expenses at $1,900.

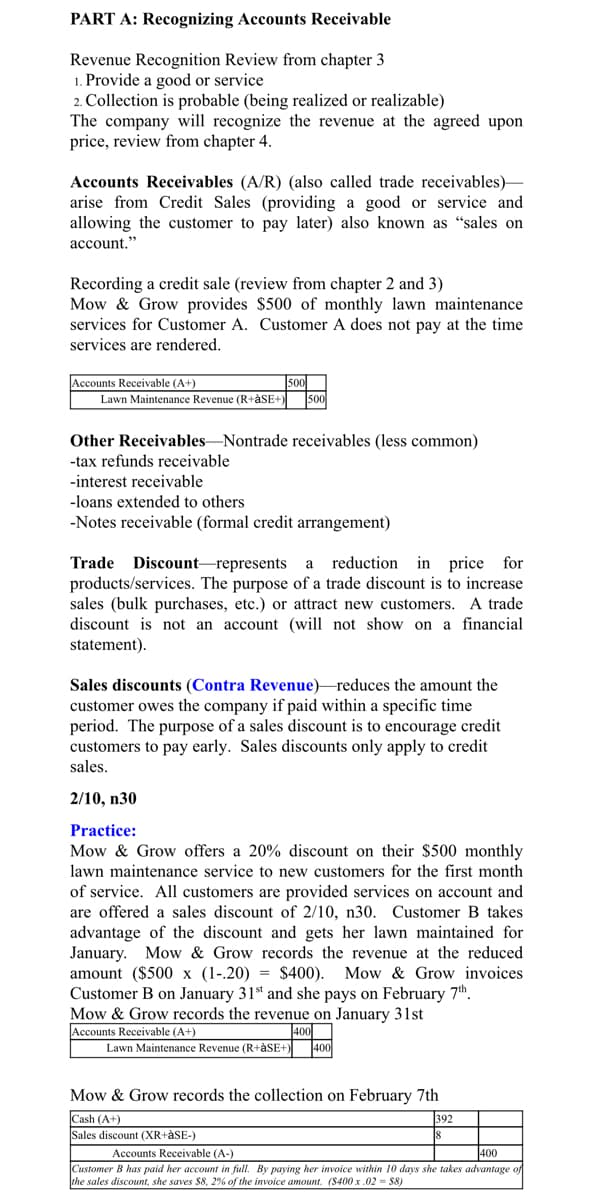

Transcribed Image Text:PART A: Recognizing Accounts Receivable

Revenue Recognition Review from chapter 3

1. Provide a good or service

2. Collection is probable (being realized or realizable)

The company will recognize the revenue at the agreed upon

price, review from chapter 4.

Accounts Receivables (A/R) (also called trade receivables)-

arise from Credit Sales (providing a good or service and

allowing the customer to pay later) also known as "sales on

account."

Recording a credit sale (review from chapter 2 and 3)

Mow & Grow provides $500 of monthly lawn maintenance

services for Customer A. Customer A does not pay at the time

services are rendered.

Accounts Receivable (A+)

Lawn Maintenance Revenue (R+àSE+)

500

500

Other Receivables-Nontrade receivables (less common)

-tax refunds receivable

-interest receivable

-loans extended to others

-Notes receivable (formal credit arrangement)

Trade Discount–represents

reduction in price for

a

products/services. The purpose of a trade discount is to increase

sales (bulk purchases, etc.) or attract new customers. A trade

discount is not an account (will not show on a financial

statement).

Sales discounts (Contra Revenue)-reduces the amount the

customer owes the company if paid within a specific time

period. The purpose of a sales discount is to encourage credit

customers to pay early. Sales discounts only apply to credit

sales.

2/10, n30

Practice:

Mow & Grow offers a 20% discount on their $500 monthly

lawn maintenance service to new customers for the first month

of service. All customers are provided services on account and

are offered a sales discount of 2/10, n30. Customer B takes

advantage of the discount and gets her lawn maintained for

January. Mow & Grow records the revenue at the reduced

amount ($500 x (1-.20) = $400). Mow & Grow invoices

Customer B on January 31st and she pays on February 7h.

Mow & Grow records the revenue on January 31st

Accounts Receivable (A+)

Lawn Maintenance Revenue (R+àSE+)

T400

Mow & Grow records the collection on February 7th

Cash (A+)

Sales discount (XR+àSE-)

392

Accounts Receivable (A-)

400

Customer B has paid her account in full. By paying her invoice within 10 days she takes advantage of

the sales discount, she saves $8, 2% of the invoice amount. (S400 x .02 = $8)

Definition Definition Receivable amount that a company is owed, but did not receive, and which may not be receivable in future.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.