Georgia's Interest in the equal GFH Partnership is liquidated when the GFH Partnership makes a Liquidating Distribution to Georgia and the remaining Partners assume Georgia's share of the Partnership Liabilities. Georgia receives $12,000 in Cash, Accounts Receivable of $21,000 (Fair Market Value) and Equipment worth (Fair Market Value) of $47,000. On the date of the Liquidation, the Partnership's Cash Basis Balance Sheet reflected the following: Cash (Adjusted Basis- $60,000; Fair Market Value - $60,000); Unrealized Receivable (Adjusted Basis-$-0-; Fair Market Value $63,000); Equipment (Adjusted Basis- $72,000; Fair Market Value - $141,000) (Total Assets: Adjusted Basis- $132,000; Fair Market Value - $264,000); Notes Payable (Adjusted Basis - $24,000; Fair Market Value - $24,000); Capital Accounts: Georgia Capital (Adjusted Basis - $36,000, Fair Market Value - $80,000); Freddie Capital (Adjusted Basis - $36,000; Fair Market Value - $80,000); Helen Capital (Adjusted Basis - $36,000; Fair Market Value-$80,000) (Total Liabilities And Equity (Capital)): Adjusted Basis- $132,000; Fair Market Value - $264,000). As a result of this Liquidation, Georgia has: O No Recognized Gain or Loss. O $20,000 Ordinary Income and $24,000 Capital Gain. $44,000 Ordinary Income and $-0- Capital Gain. O $24,000 Ordinary Income and $20,000 Capital Gain,

Georgia's Interest in the equal GFH Partnership is liquidated when the GFH Partnership makes a Liquidating Distribution to Georgia and the remaining Partners assume Georgia's share of the Partnership Liabilities. Georgia receives $12,000 in Cash, Accounts Receivable of $21,000 (Fair Market Value) and Equipment worth (Fair Market Value) of $47,000. On the date of the Liquidation, the Partnership's Cash Basis Balance Sheet reflected the following: Cash (Adjusted Basis- $60,000; Fair Market Value - $60,000); Unrealized Receivable (Adjusted Basis-$-0-; Fair Market Value $63,000); Equipment (Adjusted Basis- $72,000; Fair Market Value - $141,000) (Total Assets: Adjusted Basis- $132,000; Fair Market Value - $264,000); Notes Payable (Adjusted Basis - $24,000; Fair Market Value - $24,000); Capital Accounts: Georgia Capital (Adjusted Basis - $36,000, Fair Market Value - $80,000); Freddie Capital (Adjusted Basis - $36,000; Fair Market Value - $80,000); Helen Capital (Adjusted Basis - $36,000; Fair Market Value-$80,000) (Total Liabilities And Equity (Capital)): Adjusted Basis- $132,000; Fair Market Value - $264,000). As a result of this Liquidation, Georgia has: O No Recognized Gain or Loss. O $20,000 Ordinary Income and $24,000 Capital Gain. $44,000 Ordinary Income and $-0- Capital Gain. O $24,000 Ordinary Income and $20,000 Capital Gain,

SWFT Essntl Tax Individ/Bus Entities 2020

23rd Edition

ISBN:9780357391266

Author:Nellen

Publisher:Nellen

Chapter14: Partnerships And Limited Liability Entities

Section: Chapter Questions

Problem 2BD

Related questions

Question

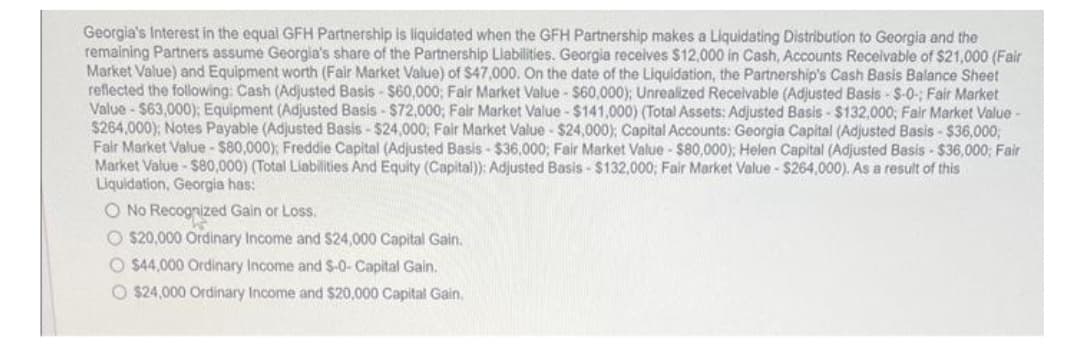

Transcribed Image Text:Georgia's Interest in the equal GFH Partnership is liquidated when the GFH Partnership makes a Liquidating Distribution to Georgia and the

remaining Partners assume Georgia's share of the Partnership Liabilities. Georgia receives $12,000 in Cash, Accounts Receivable of $21,000 (Fair

Market Value) and Equipment worth (Fair Market Value) of $47,000. On the date of the Liquidation, the Partnership's Cash Basis Balance Sheet

reflected the following: Cash (Adjusted Basis- $60,000; Fair Market Value - $60,000); Unrealized Receivable (Adjusted Basis-S-0-; Fair Market

Value - $63,000); Equipment (Adjusted Basis- $72,000; Fair Market Value - $141,000) (Total Assets: Adjusted Basis- $132,000; Fair Market Value -

$264,000); Notes Payable (Adjusted Basis - $24,000; Fair Market Value - $24,000); Capital Accounts: Georgia Capital (Adjusted Basis - $36,000,

Fair Market Value - $80,000); Freddie Capital (Adjusted Basis- $36,000; Fair Market Value - $80,000); Helen Capital (Adjusted Basis- $36,000; Fair

Market Value - $80,000) (Total Liabilities And Equity (Capital)): Adjusted Basis- $132,000; Fair Market Value - $264,000). As a result of this

Liquidation, Georgia has:

O No Recognized Gain or Loss.

O $20,000 Ordinary Income and $24,000 Capital Gain.

O$44,000 Ordinary Income and $-0- Capital Gain.

O $24,000 Ordinary Income and $20,000 Capital Gain.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT