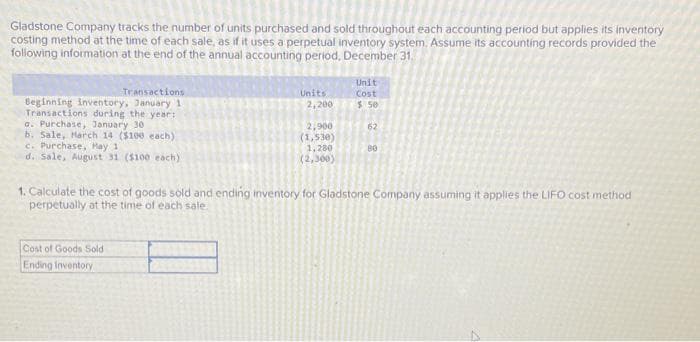

Gladstone Company tracks the number of units purchased and sold throughout each accounting period but applies its inventory costing method at the time of each sale, as if it uses a perpetual inventory system. Assume its accounting records provided the following information at the end of the annual accounting period, December 31 Unit Transactions Units Cost 2,200 $ 50 Beginning inventory, January 1 Transactions during the year: a. Purchase, January 30 2,900 62 b. Sale, March 14 ($100 each) c. Purchase, Hay 1 (1,530) 1,280 (2,300) BO d. Sale, August 31 ($100 each) 1. Calculate the cost of goods sold and ending inventory for Gladstone Company assuming it applies the LIFO cost method perpetually at the time of each sale

Gladstone Company tracks the number of units purchased and sold throughout each accounting period but applies its inventory costing method at the time of each sale, as if it uses a perpetual inventory system. Assume its accounting records provided the following information at the end of the annual accounting period, December 31 Unit Transactions Units Cost 2,200 $ 50 Beginning inventory, January 1 Transactions during the year: a. Purchase, January 30 2,900 62 b. Sale, March 14 ($100 each) c. Purchase, Hay 1 (1,530) 1,280 (2,300) BO d. Sale, August 31 ($100 each) 1. Calculate the cost of goods sold and ending inventory for Gladstone Company assuming it applies the LIFO cost method perpetually at the time of each sale

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter7: Inventories: Cost Measurement And Flow Assumptions

Section: Chapter Questions

Problem 12RE: Carla Company uses the perpetual inventory system. The following information is available for...

Related questions

Topic Video

Question

Transcribed Image Text:Gladstone Company tracks the number of units purchased and sold throughout each accounting period but applies its inventory

costing method at the time of each sale, as if it uses a perpetual inventory system. Assume its accounting records provided the

following information at the end of the annual accounting period, December 31.

Unit

Transactions

Units

Cost

2,200

$ 50

Beginning inventory, January 1

Transactions during the year:

a. Purchase, January 30

2,900

62

b. Sale, March 14 ($100 each)

c. Purchase, May 1

(1,530)

1,280

(2,300)

80

d. Sale, August 31 ($100 each)

1. Calculate the cost of goods sold and ending inventory for Gladstone Company assuming it applies the LIFO cost method

perpetually at the time of each sale.

Cost of Goods Sold

Ending Inventory

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781337272124

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781337272124

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

College Accounting (Book Only): A Career Approach

Accounting

ISBN:

9781337280570

Author:

Scott, Cathy J.

Publisher:

South-Western College Pub

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning