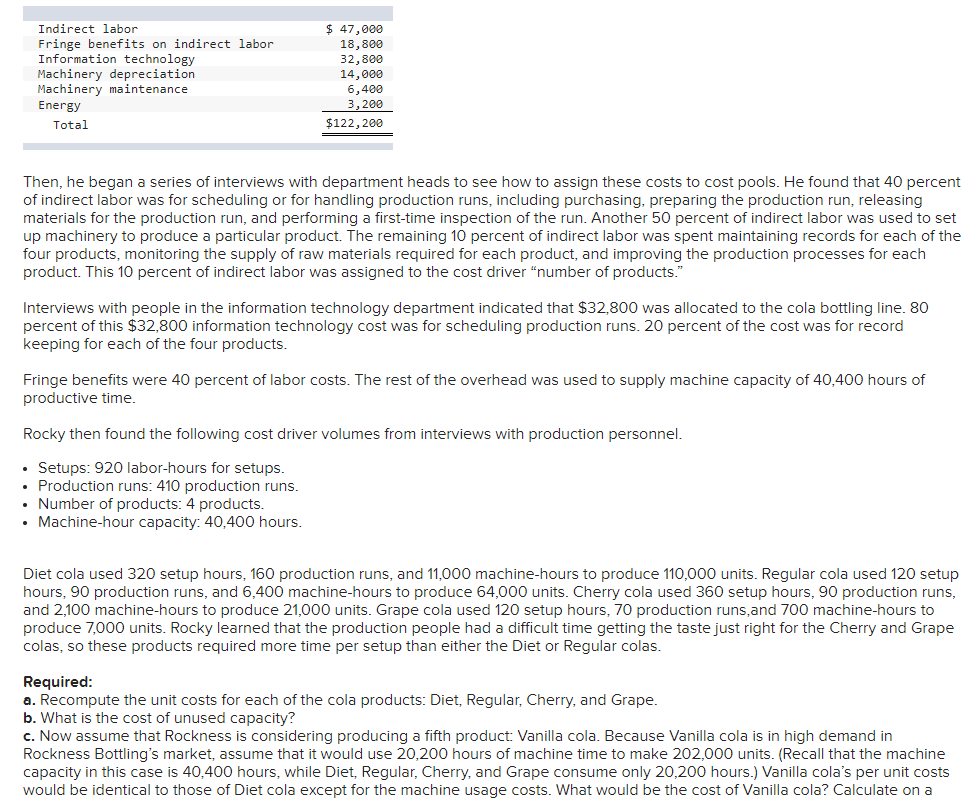

Howard Rockness was worried. His company, Rockness Bottling, showed declining profits over the past several years despite an increase in revenues. With profits declining and revenues increasing, Rockness knew there must be a problem with costs. Rockness sent an e-mail to his executive team under the subject heading, "How do we get Rockness Bottling back on track?" Meeting in Rockness's spacious office, the team began brainstorming solutions to the declining profits problem. Some members of the team wanted to add products. (These were marketing people.) Some wanted to fire the least efficient workers. (These were finance people.) Some wanted to empower the workers. (These people worked in the human resources department.) And some people wanted to install a new computer system. (It should be obvious who these people were.) Rockness listened patiently. When all participants had made their cases, Rockness said, "We made money when we were a smaller, simpler company. We have grown, added new product lines, and added new products to old product lines. Now we are going downhill. What's wrong with this picture?" Rockness continued, "Here, look at this report. This is last month's report on the cola bottling line. What do you see here?" He handed copies of the following report to the people assembled in his office. Monthly Report on Cola Bottling Line Diet $297,000 Regular $172,800 Cherry $57,750 Grape $19,950 Total Sales $547,500 Less: Materials Direct labor Fringe benefits on direct labor Indirect costs (@260% of direct labor) Gross margin Return on sales (see note [a]) Volume Unit price Unit cost 141,000 28,000 11, 200 72,800 $ 44,000 14.8% 91, 200 14,000 5,600 36,400 $ 25,600 31,920 4,200 1,680 10,920 $ 9,030 15.6% 21,000 $ 2.75 $ 2.32 13,250 800 320 2,080 $ 3,500 277,370 47,000 18,800 122,200 $ 82,130 110,000 2.70 14.8% 64, 000 2.70 17.5% 7,000 %24 15.0% 202,000 24 2.85 $4 24 2.71 2.30 2.30 2.35 2.30 Return on sales before considering selling, general and administrative expenses. Rockness asked, "Do you see any problems here? Should we drop any of these products? Should we reprice any of these products?" The room was silent for a moment, and then everybody started talking at once. Nobody could see any problems based on the data in the report, but they all made suggestions to Rockness ranging from “add another cola product" to "cut costs across the board" to "we need a new computer system so that managers can get this information more quickly." A not-so-patient Rockness stopped the discussion abruptly and adjourned the meeting. He then turned to the quietest person in the room-his son, Rocky-and said, “I am suspicious of these cost data, Rocky. Here we are assigning indirect costs to these products using a 260 percent rate. I really wonder whether that rate is accurate for all products. I want you to dig into the indirect cost data, figure out what drives those costs, and see whether you can give me more accurate cost numbers for these products." Rocky first learned from production that the process required four activities: (1) setting up production runs, (2) managing production runs, and (3) managing products. The fourth activity did not require labor; it was simply the operation of machinery. Next, he went to the accounting records to get a breakdown of indirect costs. Here is what he found:

Process Costing

Process costing is a sort of operation costing which is employed to determine the value of a product at each process or stage of producing process, applicable where goods produced from a series of continuous operations or procedure.

Job Costing

Job costing is adhesive costs of each and every job involved in the production processes. It is an accounting measure. It is a method which determines the cost of specific jobs, which are performed according to the consumer’s specifications. Job costing is possible only in businesses where the production is done as per the customer’s requirement. For example, some customers order to manufacture furniture as per their needs.

ABC Costing

Cost Accounting is a form of managerial accounting that helps the company in assessing the total variable cost so as to compute the cost of production. Cost accounting is generally used by the management so as to ensure better decision-making. In comparison to financial accounting, cost accounting has to follow a set standard ad can be used flexibly by the management as per their needs. The types of Cost Accounting include – Lean Accounting, Standard Costing, Marginal Costing and Activity Based Costing.

PLEASE SEE ATTACHED, please answer all questions.

Required:

a. Recompute the unit costs for each of the cola products: Diet, Regular, Cherry, and Grape.

b. What is the cost of unused capacity?

c. Now assume that Rockness is considering producing a fifth product: Vanilla cola. Because Vanilla cola is in high demand in Rockness Bottling’s market, assume that it would use 20,200 hours of machine time to make 202,000 units. (Recall that the machine capacity in this case is 40,400 hours, while Diet, Regular, Cherry, and Grape consume only 20,200 hours.) Vanilla cola’s per unit costs would be identical to those of Diet cola except for the machine usage costs. What would be the cost of Vanilla cola? Calculate on a per-unit basis, and then in total.

![Howard Rockness was worried. His company, Rockness Bottling, showed declining profits over the past several years despite an

increase in revenues. With profits declining and revenues increasing, Rockness knew there must be a problem with costs.

Rockness sent an e-mail to his executive team under the subject heading, “How do we get Rockness Bottling back on track?" Meeting

in Rockness's spacious office, the team began brainstorming solutions to the declining profits problem. Some members of the team

wanted to add products. (These were marketing people.) Some wanted to fire the least efficient workers. (These were finance people.)

Some wanted to empower the workers. (These people worked in the human resources department.) And some people wanted to

install a new computer system. (It should be obvious who these people were.)

Rockness listened patiently. When all participants had made their cases, Rockness said, "We made money when we were a smaller,

simpler company. We have grown, added new product lines, and added new products to old product lines. Now we are going

downhill. What's wrong with this picture?"

Rockness continued, "Here, look at this report. This is last month's report on the cola bottling line. What do you see here?" He handed

copies of the following report to the people assembled in his office.

Monthly Report on Cola Bottling Line

Diet

$297,000

Regular

$172, 800

Cherry

$57,750

Total

Grape

$19,950

Sales

$547,500

Less:

91, 200

14,000

5,600

36,400

$ 25,600

14.8%

64, 000

31,920

4,200

1,680

Materials

141,000

28,000

11, 200

13,250

277,370

Direct labor

800

47,000

Fringe benefits on direct labor

Indirect costs (@260% of direct labor)

Gross margin

Return on sales (see note [a])

Volume

320

18,800

72,800

$ 44, 000

10,920

$ 9,030

15.6%

2,080

$ 3,500

122, 200

$ 82,130

14.8%

110,000

$4

17.5%

15.0%

Unit price

Unit cost

21,000

$ 2.75

7,000

$ 2.85

202,000

%24

$4

2.70

2.70

2.71

2.30

2$

2.30

$4

2.32

$4

2.35

2.30

a Return on sales before considering selling, general and administrative expenses.

Rockness asked, "Do you see any problems here? Should we drop any of these products? Should we reprice any of these products?"

The room was silent for a moment, and then everybody started talking at once. Nobody could see any problems based on the data in

the report, but they all made suggestions to Rockness ranging from "add another cola product" to "cut costs across the board" to "we

need a new computer system so that managers can get this information more quickly." A not-so-patient Rockness stopped the

discussion abruptly and adjourned the meeting.

He then turned to the quietest person in the room-his son, Rocky-and said, "I am suspicious of these cost data, Rocky. Here we are

assigning indirect costs to these products using a 260 percent rate. I really wonder whether that rate is accurate for all products. I want

you to dig into the indirect cost data, figure out what drives those costs, and see whether you can give me more accurate cost

numbers for these products."

Rocky first learned from production that the process required four activities: (1) setting up production runs, (2) managing production

runs, and (3) managing products. The fourth activity did not require labor; it was simply the operation of machinery. Next, he went to

the accounting records to get a breakdown of indirect costs. Here is what he found:](/v2/_next/image?url=https%3A%2F%2Fcontent.bartleby.com%2Fqna-images%2Fquestion%2F61ae5430-25ae-4fd0-9dbe-872050663ccf%2F5fc7ec7b-d062-447a-aa05-a75bc4bd06b7%2Fk450vv_processed.png&w=3840&q=75)

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 6 images