If the portfolio is 500,000, with the significance level of 1%, what would be the absolute value of the portfolio with the 99% confidence level? Refer to table above.

If the portfolio is 500,000, with the significance level of 1%, what would be the absolute value of the portfolio with the 99% confidence level? Refer to table above.

MATLAB: An Introduction with Applications

6th Edition

ISBN:9781119256830

Author:Amos Gilat

Publisher:Amos Gilat

Chapter1: Starting With Matlab

Section: Chapter Questions

Problem 1P

Related questions

Question

Type only the answers please. Do not handwritten.

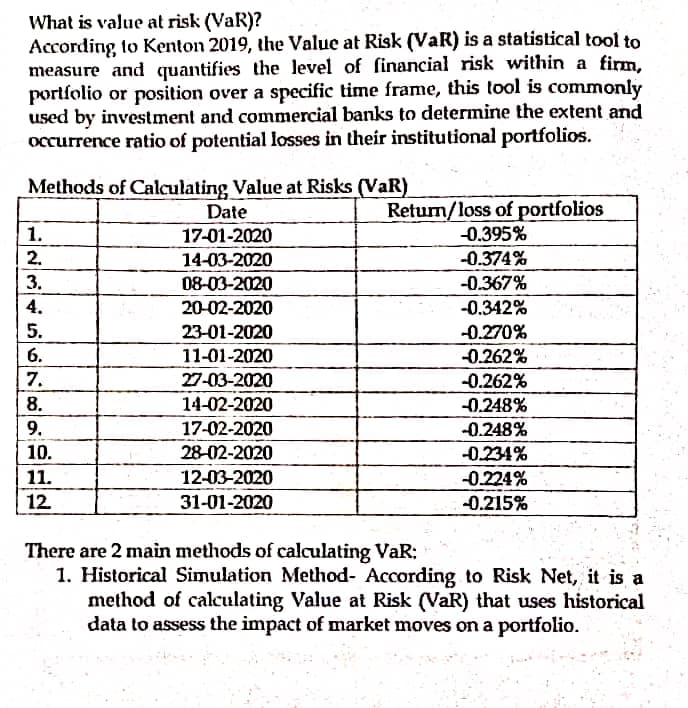

Transcribed Image Text:What is value at risk (VaR)?

According to Kenton 2019, the Value at Risk (VaR) is a statistical tool to

measure and quantifies the level of financial risk within a firm,

portfolio or position over a specific time frame, this tool is commonly

used by investment and commercial banks to determine the extent and

occurrence ratio of potential losses in their institutional portfolios.

Methods of Calculating Value at Risks (VaR)

Date

17-01-2020

Return/loss of portfolios

1.

-0.395%

2.

14-03-2020

-0.374%

3.

08-03-2020

-0.367%

4.

20-02-2020

-0.342%

5.

23-01-2020

-0.270%

6.

11-01-2020

-0.262%

7.

27-03-2020

-0.262%

8.

14-02-2020

-0.248%

9.

17-02-2020

-0.248%

10.

28-02-2020

-0.234%

11.

12-03-2020

-0.224%

12.

31-01-2020

-0.215%

There are 2 main methods of calculating VaR;

1. Historical Simulation Method- According to Risk Net, it is a

method of calculating Value at Risk (VaR) that uses historical

data to assess the impact of market moves on a portfolio.

Transcribed Image Text:If the portfolio is 500,000, with the significance level of 1%, what would

be the absolute value of the portfolio with the 99% confidence level?

Refer to table above.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Recommended textbooks for you

MATLAB: An Introduction with Applications

Statistics

ISBN:

9781119256830

Author:

Amos Gilat

Publisher:

John Wiley & Sons Inc

Probability and Statistics for Engineering and th…

Statistics

ISBN:

9781305251809

Author:

Jay L. Devore

Publisher:

Cengage Learning

Statistics for The Behavioral Sciences (MindTap C…

Statistics

ISBN:

9781305504912

Author:

Frederick J Gravetter, Larry B. Wallnau

Publisher:

Cengage Learning

MATLAB: An Introduction with Applications

Statistics

ISBN:

9781119256830

Author:

Amos Gilat

Publisher:

John Wiley & Sons Inc

Probability and Statistics for Engineering and th…

Statistics

ISBN:

9781305251809

Author:

Jay L. Devore

Publisher:

Cengage Learning

Statistics for The Behavioral Sciences (MindTap C…

Statistics

ISBN:

9781305504912

Author:

Frederick J Gravetter, Larry B. Wallnau

Publisher:

Cengage Learning

Elementary Statistics: Picturing the World (7th E…

Statistics

ISBN:

9780134683416

Author:

Ron Larson, Betsy Farber

Publisher:

PEARSON

The Basic Practice of Statistics

Statistics

ISBN:

9781319042578

Author:

David S. Moore, William I. Notz, Michael A. Fligner

Publisher:

W. H. Freeman

Introduction to the Practice of Statistics

Statistics

ISBN:

9781319013387

Author:

David S. Moore, George P. McCabe, Bruce A. Craig

Publisher:

W. H. Freeman