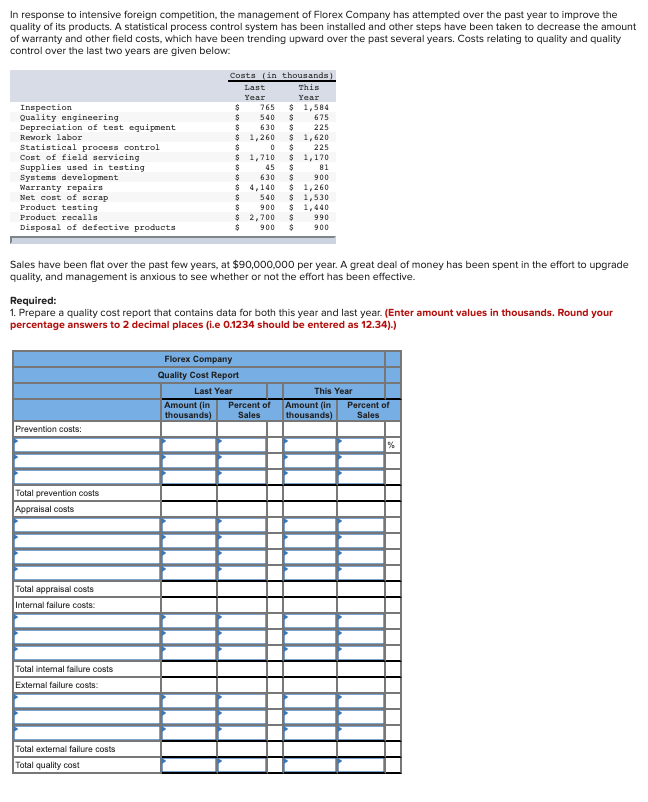

In response to intensive foreign competition, the management of Florex Company has attempted over the past year to improve the quality of its products. A statistical process control system has been installed and other steps have been taken to decrease the amount of warranty and other field costs, which have been trending upward over the past several years. Costs relating to quality and quality control over the last two years are given below. Costs (in thousands) Last This Year Year 765 $ 1,584 540 $ Inspection Quality engineering Depreciation of test equipment Revork labor Statistical process control Cost of field servicing 675 $ 630 $ 225 $ 1,260 $ 1,620 225 $ 1,710 $ 1,170 Supplies used in testing Systems development Warranty repairs Net cost of scrap Product testing 45 81 900 630 $ 4,140 540 $ 1,260 $ 1,530 $ 1,440 990 900 $ 2,700 $ 900 Product recalls Disposal of defective products 900 Sales have been flat over the past few years, at $90,000,000 per year. A great deal of money has been spent in the effort to upgrade quality, and management is anxious to see whether or not the effort has been effective.

In response to intensive foreign competition, the management of Florex Company has attempted over the past year to improve the quality of its products. A statistical process control system has been installed and other steps have been taken to decrease the amount of warranty and other field costs, which have been trending upward over the past several years. Costs relating to quality and quality control over the last two years are given below. Costs (in thousands) Last This Year Year 765 $ 1,584 540 $ Inspection Quality engineering Depreciation of test equipment Revork labor Statistical process control Cost of field servicing 675 $ 630 $ 225 $ 1,260 $ 1,620 225 $ 1,710 $ 1,170 Supplies used in testing Systems development Warranty repairs Net cost of scrap Product testing 45 81 900 630 $ 4,140 540 $ 1,260 $ 1,530 $ 1,440 990 900 $ 2,700 $ 900 Product recalls Disposal of defective products 900 Sales have been flat over the past few years, at $90,000,000 per year. A great deal of money has been spent in the effort to upgrade quality, and management is anxious to see whether or not the effort has been effective.

Managerial Accounting: The Cornerstone of Business Decision-Making

7th Edition

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Chapter13: Emerging Topics In Managerial Accounting

Section: Chapter Questions

Problem 56P: In 20X1, Don Blackburn, president of Price Electronics, received a report indicating that quality...

Related questions

Question

Transcribed Image Text:In response to intensive foreign competition, the management of Florex Company has attempted over the past year to improve the

quality of its products. A statistical process control system has been installed and other steps have been taken to decrease the amount

of warranty and other field costs, which have been trending upward over the past several years. Costs relating to quality and quality

control over the last two years are given below:

Costs (in thousands)

Last

This

Year

Year

$ 1,584

Inspection

Quality engineering

Depreciation of test eguipment

765

540

675

630

225

$ 1,260

$ 1,620

225

Rework labor

Statistical process control

Cost of field servicing

$ 1,710

1,170

81

Supplies used in testing

Systems development

Warranty repairs

Net cost of scrap

Product testing

Product recalls

45

630

900

1,260

24

4,140

1,530

$ 1,440

990

540

900

$ 2,700

900

Disposal of defective products

900

Sales have been flat over the past few years, at $90,000,000 per year. A great deal of money has been spent in the effort to upgrade

quality, and management is anxious to see whether or not the effort has been effective.

Required:

1. Prepare a quality cost report that contains data for both this year and last year. (Enter amount values in thousands. Round your

percentage answers to 2 decimal places (i.e 0.1234 should be entered as 12.34).)

Florex Company

Quality Cost Report

Last Year

This Year

Amount (in

thousands)

Percent of

Sales

Amount (in

thousands)

Percent of

Sales

Prevention costs:

Total prevention costs

Appraisal costs

Total appraisal costs

Internal failure costs:

Total intemal failure costs

External failure costs:

Total external failure costs

Total quality cost

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning