KITCHENS JUST FOR YOU Balance Sheet September 1, 20X9 Assets Cash 6,000 $ 39,000 Accounts Payable Receivables 68,000 Connie, Loan 14,000 Terry, Loan 8,000 Terry, Capital 11,500 (30%) Inventory 48,000 Phyllis, Capital 37,000 (60%) Goodwill 22,000 50,500 Connie, Capital (10%) Total Assets $ 152,000 $152,000 Total Liabilities & Equities Connie's loan was for working capital; the loan to Terry was for his unexpected personal medical bills. During September 20X9, the first month of liquidation, the partnership collected $43,000 in receivables and decided to write off $14,000 of the remaining receivables. Sales of one-half of the book value of the inventory realized a loss of $6,000. The partners estimate that the costs of liquidating the business (newspaper ads, signs, etc.), are expected to be $6,000 for the remainder of the liquidation process. Required: Prepare a schedule of safe payments to partners as of September 30, 20X9, to show how the available cash should be distributed to the partners. Please follow the practical guidelines when completing this worksheet. Liabilities and Equities $

KITCHENS JUST FOR YOU Balance Sheet September 1, 20X9 Assets Cash 6,000 $ 39,000 Accounts Payable Receivables 68,000 Connie, Loan 14,000 Terry, Loan 8,000 Terry, Capital 11,500 (30%) Inventory 48,000 Phyllis, Capital 37,000 (60%) Goodwill 22,000 50,500 Connie, Capital (10%) Total Assets $ 152,000 $152,000 Total Liabilities & Equities Connie's loan was for working capital; the loan to Terry was for his unexpected personal medical bills. During September 20X9, the first month of liquidation, the partnership collected $43,000 in receivables and decided to write off $14,000 of the remaining receivables. Sales of one-half of the book value of the inventory realized a loss of $6,000. The partners estimate that the costs of liquidating the business (newspaper ads, signs, etc.), are expected to be $6,000 for the remainder of the liquidation process. Required: Prepare a schedule of safe payments to partners as of September 30, 20X9, to show how the available cash should be distributed to the partners. Please follow the practical guidelines when completing this worksheet. Liabilities and Equities $

SWFT Essntl Tax Individ/Bus Entities 2020

23rd Edition

ISBN:9780357391266

Author:Nellen

Publisher:Nellen

Chapter1: Introductin To Taxation

Section: Chapter Questions

Problem 9P

Related questions

Question

Transcribed Image Text:After working for In the Kitchen remodeling business for several years, Terry

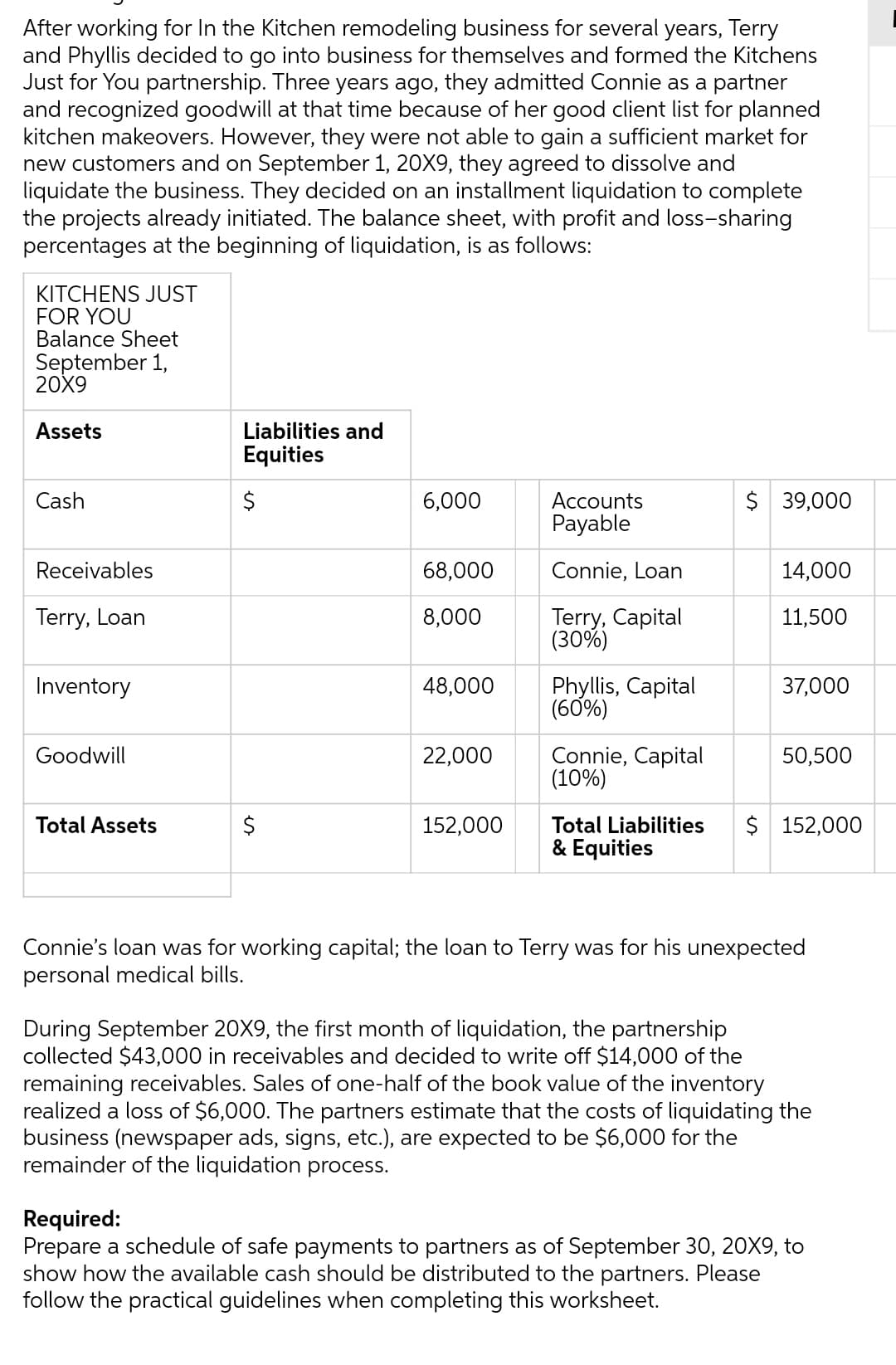

and Phyllis decided to go into business for themselves and formed the Kitchens

Just for You partnership. Three years ago, they admitted Connie as a partner

and recognized goodwill at that time because of her good client list for planned

kitchen makeovers. However, they were not able to gain a sufficient market for

new customers and on September 1, 20X9, they agreed to dissolve and

liquidate the business. They decided on an installment liquidation to complete

the projects already initiated. The balance sheet, with profit and loss-sharing

percentages at the beginning of liquidation, is as follows:

KITCHENS JUST

FOR YOU

Balance Sheet

September 1,

20X9

Assets

Liabilities and

Equities

Cash

$

6,000

$ 39,000

Accounts

Payable

Receivables

68,000

Connie, Loan

14,000

Terry, Loan

8,000

Terry, Capital

11,500

(30%)

Inventory

48,000

37,000

Phyllis, Capital

(60%)

Goodwill

22,000

50,500

Connie, Capital

(10%)

Total Assets

$

152,000

Total Liabilities $ 152,000

& Equities

Connie's loan was for working capital; the loan to Terry was for his unexpected

personal medical bills.

During September 20X9, the first month of liquidation, the partnership

collected $43,000 in receivables and decided to write off $14,000 of the

remaining receivables. Sales of one-half of the book value of the inventory

realized a loss of $6,000. The partners estimate that the costs of liquidating the

business (newspaper ads, signs, etc.), are expected to be $6,000 for the

remainder of the liquidation process.

Required:

Prepare a schedule of safe payments to partners as of September 30, 20X9, to

show how the available cash should be distributed to the partners. Please

follow the practical guidelines when completing this worksheet.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Business Its Legal Ethical & Global Environment

Accounting

ISBN:

9781305224414

Author:

JENNINGS

Publisher:

Cengage

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Business Its Legal Ethical & Global Environment

Accounting

ISBN:

9781305224414

Author:

JENNINGS

Publisher:

Cengage

College Accounting, Chapters 1-27 (New in Account…

Accounting

ISBN:

9781305666160

Author:

James A. Heintz, Robert W. Parry

Publisher:

Cengage Learning