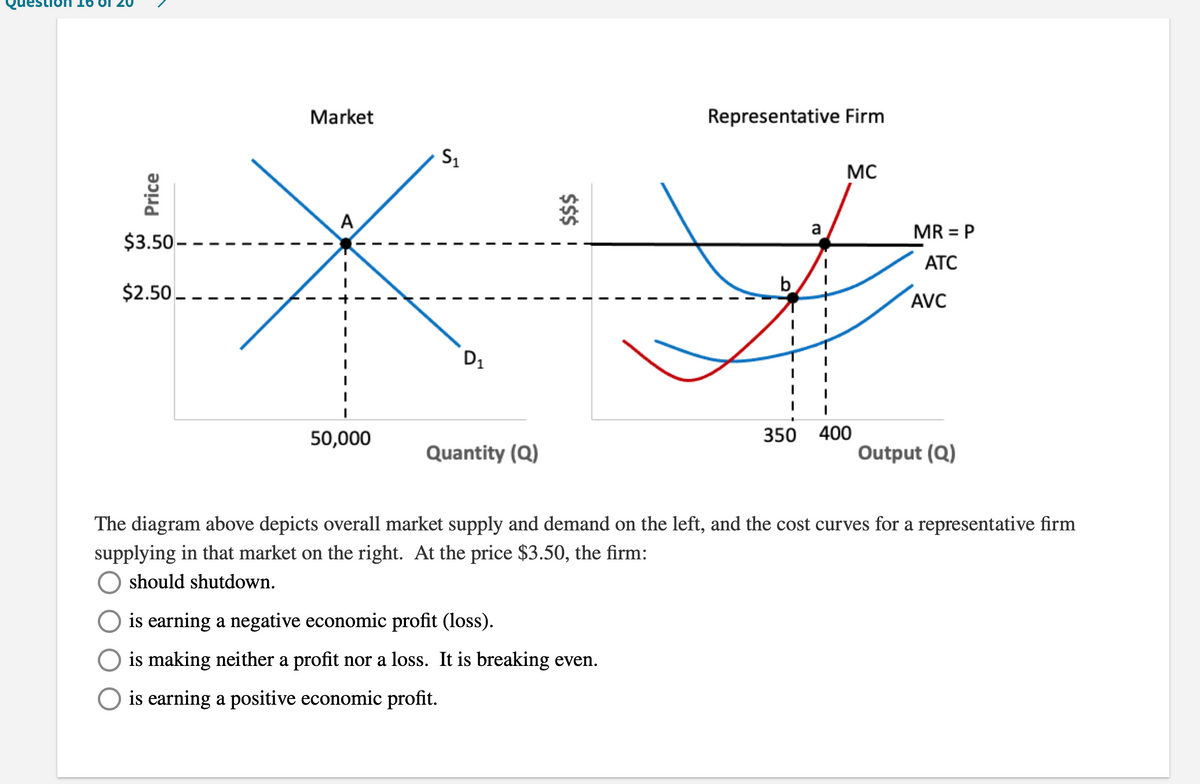

Market Representative Firm MC a MR = P $3.50– - АТС b $2.50. AVC 50,000 350 400 Quantity (Q) Output (Q) The diagram above depicts overall market supply and demand on the left, and the cost curves for a representative firm supplying in that market on the right. At the price $3.50, the firm: should shutdown. is earning a negative economic profit (loss). O is making neither a profit nor a loss. It is breaking even. O is earning a positive economic profit. Price $$

Q: Total Variable Cost Output (Q) 0. Total Fixed Cost 20 1 20 7 3S 10 3.3 15 3.75 21 42 20 20 20 20 The…

A: A perfectly competitive firm is a price taker and can sell any quantity of the commodity at the…

Q: If the market price for the perfectly competitive firm represented in Figure 1.5 is $4... Figure 1.5…

A: "In perfectly competitive market structure firms produce homogeneous products and are price taker.…

Q: Question 14 Questions 14-18 refer to Figure 5-1 below. Suppose a firm operating in a perfectly…

A: Here, the given graph shows the cost functions of a perfectly competitive market with current price…

Q: Market Representative Firm MC A a MR = P $3.50 - ATC $2.50 - AVC 50,000 350 400 Quantity (Q) Output…

A: At equilibrium, demand is equal to supply. So the equilibrium price is $ 3.50. At profit…

Q: The Market for Good X is perfectly competitive, with market supply and own-price demand curves given…

A: a. The equilibrium price and quantity is calculated by setting the demand and supply equal.…

Q: Consider the market for solar power. Assume the market is perfectly competitive and initially in…

A: Long-run competitive equilibrium condition holds if, 1. All firms in the industry are maximizing…

Q: Yann's bakery operates in a perfectly competitive market where the prevailing price for a baguette…

A: In a perfectly competitive market, the profit-maximizing quantity is at that at which price is equal…

Q: Draw 2graphs, one to represent the market (supply and demand), and one to represent a single firm…

A: "Since you have asked multiple parts, we will answer only first two parts for you. If you want other…

Q: 2. A competitive market is made up of 100 identical firms. Each firm has a short-run marginal cost…

A: A perfectly competitive firm produces at P=MC in short run. P=MC is the short run supply for an…

Q: The two figures below show (on the left) the industry supply and demand for wheat and (on the right)…

A: The firms will exit the industry when they face losses i.e. the price is below the average total…

Q: Market Representative Firm MC АТС b $8 AVC $6 MR = P D1 20,000 100 125 Quantity (Q) Output (Q) The…

A: Market has equilibrium price = $6, a competitive firm produce output = 100 units. But at this price…

Q: Suppose Malik is one of the many sellers of milk in Karachi who owns his business with the title…

A: In order to minimize the costs, a firm produces at its lowest average cost quantity. This is a given…

Q: How much milk will Malik as an individual firm would supply in the market at the price of Rs. 14 per…

A:

Q: 4. Cost functions and profit maximization Caution: This problem has the same values as the previous…

A: Disclaimer :- As you posted multipart questions we are supposed to solve the first 3 questions only…

Q: A company that sells beef to consumers and producers of beef jerky. The firm's demand function D and…

A: To draw the graph of company, we derive values of demand function and MR , MC P D1 D2 MR1 MR2…

Q: The Canadian canola industry is perfectly competitive with identical farms exhibiting the long-run…

A: In competitive market, long run equilibrium determined by the long run average total cost.

Q: Figure 14-3 Suppose a firm operating in a competitive market has the following cost curves: PRICE a…

A: In a perfectly competitive market, there are many buyers and sellers. Firms produce identical goods…

Q: A juice producing company operates in a perfectly competitive market and is therefore a price taker.…

A: A perfectly competitive firm is a price taker and can sell any quantity of the commodity at the…

Q: Assume Robbie's Robots operates in a perfectly competitive market producing 3,000 robots per day. At…

A: In perfection competition, we know that P=MR=AR. The profit is maximized at a point when MR=MC.…

Q: Total cost: TC=50 + 1/2q^2 Marginal cost: MC=q where q is an individual firm's quantity produced The…

A: Variable costs vary based on the amount of output produced. Variable costs may include labor,…

Q: Revenue and cost (dollars per unit) 50 MC ATC AVC 40 30 20 10 10 20 30 40 50 Output (units per day)…

A: The firms and businesses tend to operate with the motive of earning maximum amount of profits. The…

Q: Assume a competitive firm faces a market price of $80, a cost curve of: C = 0.004g + 50g + 1000, and…

A: Answer - Given in the question- C = 0.004q2 + 50q +1000 MC = 0.012q2 + 50 Price = $80 At profit…

Q: Donald is a producer in the perfectly competitive market for cronuts - a pastry that is half…

A: Here we calculate the market price per coconut at when Donald profit is maximized so by using the…

Q: Figure 9.2 shows the cost structure of a firm in a perfectly competitive market. If the market price…

A: A perfectly competitive market is one in which many firms offer identical product or services to the…

Q: Peg repairs transmissions. Her fixed costs are $300 a month and it costs her $24 of labor to repair…

A: A firm maximises profit at the level of output where marginal revenue (MR) equals marginal cost…

Q: The figure to the right represents the cost structure for a perfectly competitive firm with its…

A: A perfectly competitive firm is one of many firms producing identical goods in the market.

Q: Yann's bakery operates in a perfectly competitive market where the prevailing price for a baguette…

A: A firm in perfect competition maximizes profit where: Price = Marginal Cost Producer Surplus is…

Q: The marginal cost of providing a taxi trip is $5.00. Each taxi has the ability to make 20 trips per…

A:

Q: Do all part to both question 1 and question 2 Question 1 (Q is quantity of production) TFC TVC TC…

A: Since the question has multiple sub-parts, we will solve first three sub parts for you. Repost the…

Q: Q -1: For an individual firm in a perfectly competitive market, let its cost function be c(y) = 8y2…

A: Definition: Perfect competition leads to the Pareto-productive allocation of financial assets. On…

Q: PROBLEM (4) The market for plastic toys is perfectly competitive, and it is composed of many…

A: Hello. Since your question has multiple sub-parts, we will solve first three sub-parts for you. If…

Q: Market Representative Firm MC АТС b. $8 AVC $6 a MR = P D1 20,000 100 125 Quantity (Q) Output (Q)…

A: In a perfectly competitive market there are large number of firms producing similar and identical…

Q: Suppose you are a perfectly competitive firm producing computer memory chips. Your production…

A: Answer a) The market price of the chip is $5, and the marginal cost of producing each chip is $10,…

Q: Assume that the price on the market right now is SEK 50. a) How much profit or loss does the…

A: (Note: Since there are multiple parts, the first three have been solved). (a) The LR…

Q: A firm in a competitive market receives $500 in total revenue and has marginal revenue of $10. What…

A: Perfect competition is a market structure featuring more number of sellers and buyers in the market,…

Q: Lily's bakery operates in a perfectly competitive market where the prevailing price for a pumpkin…

A: Perfect competition is a market arrangement in which all businesses or enterprises offer the same…

Q: A perfectly competitive firm's total cost function is TC = 200 + 4q + 2q2. where q is the firm's…

A: A cost function consists of two types of costs:-fixed costs and variable costs. Fixed costs are…

Q: A firm sells its product in a perfectly competitive market where other firms charge a price of $90…

A: We are authorized to answer three subparts at a time since you have not mentioned which part you are…

Q: Suppose that a perfectly competitive industry consists of 192 firms and fixed cost of an individual…

A: Total cost is the sum of Fixed cost and variable cost. Average variable cost is the variable cost…

Q: Given the cost data in the table below, the firm will shut down and produce zero output if the…

A: The firm incurs loss if total revenue earned is less than total cost. It implies that firm is not…

Q: Consider the following cost curves faced by each firm: TC = 60 + 0.5q and MC = q, where q is the…

A: In perfectly competitive market, price is constant so price is equal to marginal revenue. Profit is…

Q: Natural-ExP is a unique company that is dedicated to making day trips to the Nevado de Toluca. The…

A: Here, the cost of new customer is given, which is also known as marginal cost, such that: Cmg=20g…

Q: A firm sells its product in a perfectly competitive market where other firms charge a price of $100…

A: (a) A perfectly competitive firm produces at P=MC in short run. C = 60 + 12Q + 2Q2 Differentiate C…

Q: In a perfectly competitive market demand function of a good is QD = -30P + 5490 = 20P + 1140 and…

A: Given : Qd = -30 P + 5490 Qd = 20 p + 1140 TC = Q3 - 12 Q2 + 60 Q

Q: (a) A firm operates in a market of pure competition where the market price for a product is…

A: TC = 13Q3 - 6Q2 + 44Q MC = Q2 - 12Q + 44 Price = $15

Q: There are 80 firms of type A and 60 firms of type B in a perfectly competitive market. On one hand,…

A: Correct : q= 3, profit = $6 Market supply is the summation of 80*marginal cost of each firm A +…

Q: The table provides data on a market demand schedule (top two rows) and a firm's average and…

A: Hi, thank you for the question. As per the guidelines, we are allowed to attempt only first…

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 1 images

- A firm’s profit is given by the following function, which maps output q ≥ 0 onto profit (revenue minus cost). π(q) = 11q − (q 2 + 2q + 10) = −q 2 + 9q − 10, The firm is constrained by a quota such that output q cannot be greater than a value Q. (a) What is the domain of this profit function? 1 of 2 ECON10071/20071 - 2020/21 (b) Given this, what is (global) profit maximising output when (i) Q = 6, and when (ii) Q = 2.c) Assume that the market price for bagel services is 42 and store produces 30 units of the bagel. Calculate theprofit level. Is the store profit maximizing? Explain your answer. d) Go back to part c) and assume that there are 100 identical bagel store in the market. Determine the market supply curve. (You will obtain total market quantity, Q, as a function of price,P). Are elasticities of individual firm supply and market supply curves different? e) Given the market supply curve you have calculated in part d), now assume that market demand forhairdressers are given by Q=2900-50P. Find the equilibrium price and quantity in the market. Does the marketequilibrium correspond to long-run equilibrium? ExplainA price-taking firm in a competitive industry of a good that is continuously divisible (like sand) has a total cost function TC(Q) = 3.5Q^2 + 100Q + 500. The market price for the good is p = $240. a: Carefully write out this firm’s profit maximization problem, using the particulars of thisproblem. b: Give the marginal condition (equation) that characterizes the solution to this problem. Solvethis condition for the firm’s optimal quantity Q*. c: Calculate the firm’s maximized profit. d: On a graph with quantity on the horizontal axis, neatly plot the marginal revenue curve andmarginal cost curve. Show Q* on your graph. e: Label areas on your graph using a, b, c, etc. and indicate the areas that correspond to totalrevenue and variable cost.

- 1- Suppose that the total cost function of a firm is given as follows;TC = 500 + 2Q2And the price of the firm’s product is determined by the market equilibrium at $100.a- Set the profit maximizing condition . Find the profit maximizing output level for this firm .b- What is the total revenue ?c- What is the total cost ?d- What is the profit earned by the firm ?e- Illustrate your answer by using a well-labeled graph .f- Denote the break even price level with Pb on the same graph .g- Denote the shut down price level with Ps on the same graph.h- Show the firm’s supply curve on the same graph .i- Does the firm function in short-run or long-run ? Why ?Demand and Supply equations of a particular market are as follows.Qd = 2100 – 7PQs = – 1200 + 5PWhere, Qd is the quantity demanded, Qs is the quantity supplied and P is the market price. By all means, this market is considered as a perfectly competitive market. The average cost information of a selected firm in this market is given below.AFC = 450/QAVC = (155Q + 2Q2)/Q a) Calculate the profit maximizing output level of the firm based on Marginal approach.b) Calculate the profit (in Rupees) at the profit maximizing output level.Faye is an entrepreneur considering whether to enter the market for providing websites to universities offering online learning. The market is currently perfectly competitive, and the market-clearing price is $10,000 per client. Her marginal cost is given by the equation MC = 200Q. a. In this market, what is Faye’s marginal revenue function? b. If Faye enters the market, how many website clients will she have, and what will her profit be? You can assume no fixed cost. Now imagine Faye asks you for advice. She knows you have just taken this course, and you learned about market power. c. Explain two ways Faye can achieve greater market power in this market. Faye takes your advice, and she is now the monopolist in a new market, where the demand curve is given by Q = 300,000 – 1,000P d. What is Faye’s new marginal revenue curve? e. In this new market, how clients will she have, and at what price will she sell her services? Now imagine you see all the profits Faye is making and you decide…

- A firm has the following total costs, where Q is output and TC is total cost: QTC0$ 1001110213031604200525063107380846095501065011760 Say the firm is in a perfectly competitive market. If the current market (equilibrium) price is $ 70, at what output level will the firm as a profit maximizer produce at? Say the market price rises to $ 100. At what output level (as a perfect competitor) will this produce at? How much profit is the firm making at a price of $90? Based on this calculation, do you expect firms to enter or leave this market? Say instead this firm is a monopoly. If the firm maximizes profit at an output level where marginal revenue equals $ 80, what output level will this be?If supply curve of firms in competitive market is P = 120 - 60Q1. Obtain supply curve of market, for a total of:(a) 250 producers(b) 170 producersSunrise Juice Company sells its output in a perfectly competitive market. The firm's total cost function is given in the following schedule: Output Total Cost (Units) ($) 0 50 10 120 20 170 30 210 40 260 50 330 60 430 Total costs include a "normal" return on the time (labor services) and capital that the owner has invested in the firm. The prevailing market price is $7 per unit. (a) Prepare (i) marginal cost and (ii) average total cost schedules for the firm. (b) What is the firm's profit maximizing output level? (c) Is the industry in long-run equilibrium? Justify your answer.

- PakMonoG’s inverse demand function is P = 100 – 2Q and cost function is TC = 10 + 2Q, where Q is quantity in units and P price in PKR. (need answers of 2 & 3) 1. Given your calculations in (a), illustrate the demand, marginal revenue and marginal cost curves of the firm in a graph. 2. If we were to compare PakMonoG with a perfect competitive firm in the market, are there differences in characteristics of the two structures? 3. What are welfare implications? Is total societal welfare of the firm higher or lower than that of a competitive firm? Support your answer using the graph in (b) above.Start from a market with perfect competition. For a representative producer, the long-term marginal cost is given by LMC=9Q2−20Q+50LMC=9Q2−20Q+50 and the long-term total cost function is LTC=3Q3−10Q2+50QLTC=3Q3−10Q2+50Q Assume that the price on the market right now is SEK 50. a) How much profit or loss does the producer make in the initial situation? b) Describe in detail what will happen in the market and why c) What will the equilibrium price be? d) how much will our producer produce at market equilibrium?Only typed answer You’ve been given a firm’s production and cost functions: p = 132 − 2q MC = 12 + 4q Assume this firm is in a perfectly competitive market. Calculate the equilibrium price and quantity. What is the firm’s profit here? Assume this firm is in a monopoly market. Calculate the equilibrium price and quantity. What is the firm’s profit here?