On 1 January 2019 Big Ltd acquired all the assets and liabilities of Small Ltd instead of Small Ltd's issued shares. Details of the consideration paid: Cash of $380,000, half to be paid on 1 January 2019, with the balance due on 1 January 2020. The incremental borrowing rate for Big Ltd is 10% 100,000 shares in Big Ltd were issued. The share price on 1 January 2019 was $1.50 per share. This price was a six-month high. Cost of issuing the shares was $1,500. Owing to the doubts whether the share price would remain at $1.50, Big Ltd agreed to pay cash equal to value of any decrease in the share price below $1.50. This guarantee was valid for 3 months (to 31 March 2019). Big Ltd believed that there was a 75% chance that the share price would remain at or above $1.50 until 31 March 2019 and a 25% chance that it would fall to $1.40. Supply of a patent to Small Ltd. The fair value of the patent is $60,000. As the patent was internally generated by Big Ltd, it has not been recognised in Big Ltd's books. Legal fees and associated costs with the acquisition totalled $4,000. Further, Small Ltd's assets and liabilities acquired by Big Ltd are as follows: Carrying Amount Plant and equipment Land Inventory Accounts receivable Accounts payable Bank overdraft $360 000 260 000 24 000 18 000 (35 000) (55 000) Fair Value $367 000 257 000 30 000 16 000 (35 000) (55 000) Besides, Small Ltd had an unrecorded contingent liability of $10 000 at that time. It was an existing obligation that failed the probable occurrence test. Required: As Big Ltd's company accountant, you are asked to: (1) Provide a calculation to find out Big Ltd's total cost of acquisition and the associated goodwill or a gain on bargain purchase; (2) Prepare all the necessary journal entries to record Big Ltd's purchase of Small Ltd's assets and liabilities.

On 1 January 2019 Big Ltd acquired all the assets and liabilities of Small Ltd instead of Small Ltd's issued shares. Details of the consideration paid: Cash of $380,000, half to be paid on 1 January 2019, with the balance due on 1 January 2020. The incremental borrowing rate for Big Ltd is 10% 100,000 shares in Big Ltd were issued. The share price on 1 January 2019 was $1.50 per share. This price was a six-month high. Cost of issuing the shares was $1,500. Owing to the doubts whether the share price would remain at $1.50, Big Ltd agreed to pay cash equal to value of any decrease in the share price below $1.50. This guarantee was valid for 3 months (to 31 March 2019). Big Ltd believed that there was a 75% chance that the share price would remain at or above $1.50 until 31 March 2019 and a 25% chance that it would fall to $1.40. Supply of a patent to Small Ltd. The fair value of the patent is $60,000. As the patent was internally generated by Big Ltd, it has not been recognised in Big Ltd's books. Legal fees and associated costs with the acquisition totalled $4,000. Further, Small Ltd's assets and liabilities acquired by Big Ltd are as follows: Carrying Amount Plant and equipment Land Inventory Accounts receivable Accounts payable Bank overdraft $360 000 260 000 24 000 18 000 (35 000) (55 000) Fair Value $367 000 257 000 30 000 16 000 (35 000) (55 000) Besides, Small Ltd had an unrecorded contingent liability of $10 000 at that time. It was an existing obligation that failed the probable occurrence test. Required: As Big Ltd's company accountant, you are asked to: (1) Provide a calculation to find out Big Ltd's total cost of acquisition and the associated goodwill or a gain on bargain purchase; (2) Prepare all the necessary journal entries to record Big Ltd's purchase of Small Ltd's assets and liabilities.

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter14: Financing Liabilities: Bonds And Long-term Notes Payable

Section: Chapter Questions

Problem 29E

Related questions

Question

Transcribed Image Text:On 1 January 2019 Big Ltd acquired all the assets and liabilities of Small Ltd instead of

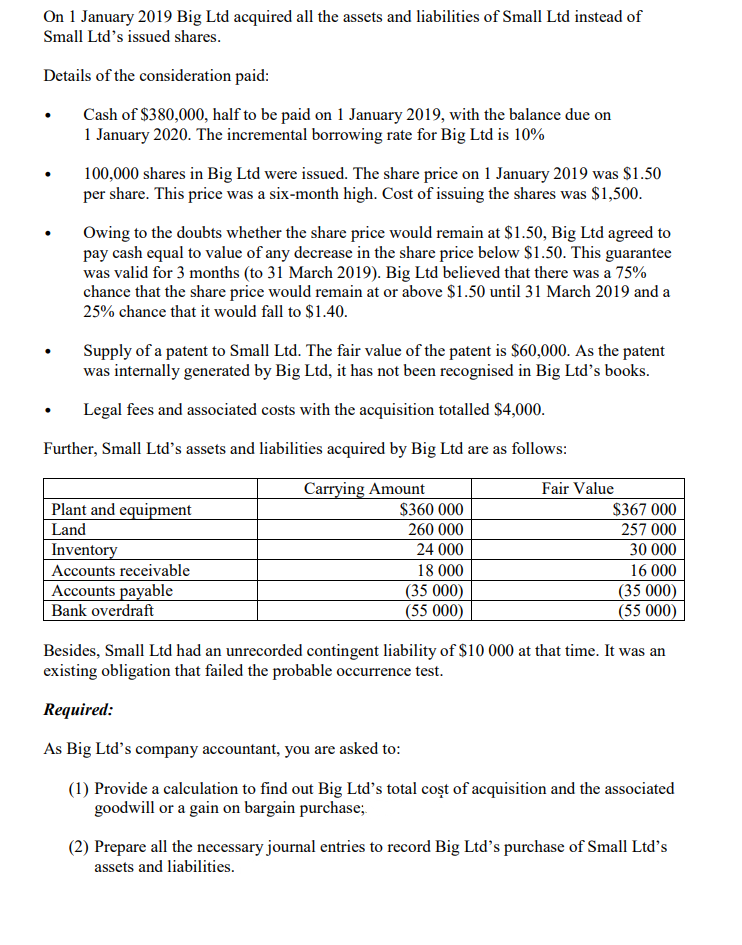

Small Ltd's issued shares.

Details of the consideration paid:

Cash of $380,000, half to be paid on 1 January 2019, with the balance due on

1 January 2020. The incremental borrowing rate for Big Ltd is 10%

.

100,000 shares in Big Ltd were issued. The share price on 1 January 2019 was $1.50

per share. This price was a six-month high. Cost of issuing the shares was $1,500.

Owing to the doubts whether the share price would remain at $1.50, Big Ltd agreed to

pay cash equal to value of any decrease in the share price below $1.50. This guarantee

was valid for 3 months (to 31 March 2019). Big Ltd believed that there was a 75%

chance that the share price would remain at or above $1.50 until 31 March 2019 and a

25% chance that it would fall to $1.40.

Supply of a patent to Small Ltd. The fair value of the patent is $60,000. As the patent

was internally generated by Big Ltd, it has not been recognised in Big Ltd's books.

Legal fees and associated costs with the acquisition totalled $4,000.

Further, Small Ltd's assets and liabilities acquired by Big Ltd are as follows:

Carrying Amount

Plant and equipment

Land

Inventory

Accounts receivable

Accounts payable

Bank overdraft

$360 000

260 000

24 000

18 000

(35 000)

(55 000)

Fair Value

$367 000

257 000

30 000

16 000

(35 000)

(55 000)

Besides, Small Ltd had an unrecorded contingent liability of $10 000 at that time. It was an

existing obligation that failed the probable occurrence test.

Required:

As Big Ltd's company accountant, you are asked to:

(1) Provide a calculation to find out Big Ltd's total cost of acquisition and the associated

goodwill or a gain on bargain purchase;

(2) Prepare all the necessary journal entries to record Big Ltd's purchase of Small Ltd's

assets and liabilities.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning