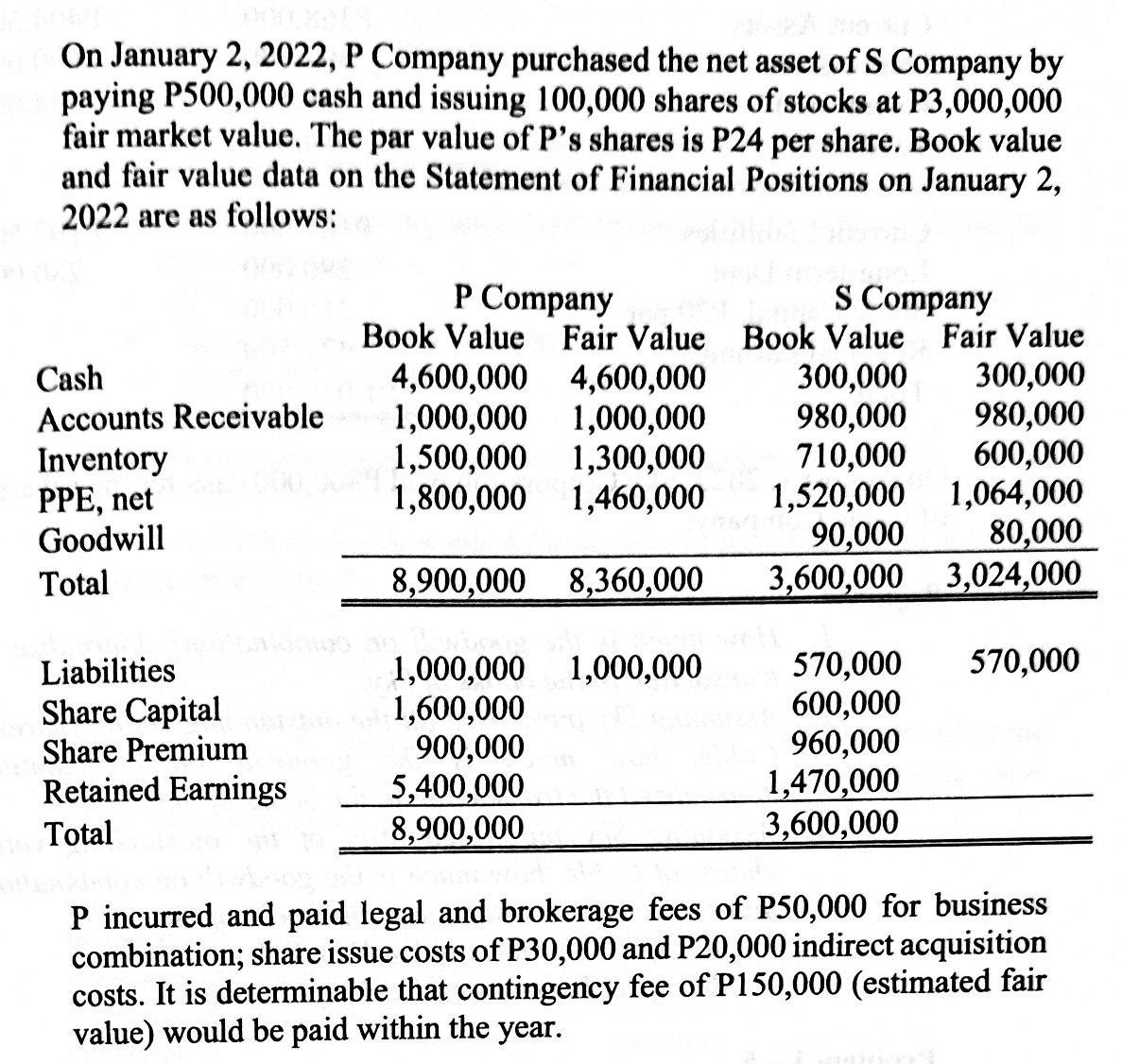

On January 2, 2022, P Company purchased the net asset of S Company by paying P500,000 cash and issuing 100,000 shares of stocks at P3,000,000 fair market value. The par value of P's shares is P24 per share. Book value and fair value data on the Statement of Financial Positions on January 2, 2022 are as follows: P Company Book Value Fair Value Book Value Fair Value 4,600,000 4,600,000 1,000,000 1,000,000 1,500,000 1,300,000 1,800,000 1,460,000 S Company Cash Accounts Receivable 300,000 980,000 710,000 1,520,000 1,064,000 90,000 3,600,000 3,024,000 300,000 980,000 600,000 Inventory PPE, net Goodwill 80,000 Total 8,900,000 8,360,000 570,000 Liabilities Share Capital Share Premium Retained Earnings 1,000,000 1,600,000 900,000 5,400,000 8,900,000 570,000 600,000 960,000 1,470,000 3,600,000 d1,000,000 Total P incurred and paid legal and brokerage fees of P50,000 for business combination; share issue costs of P30,000 and P20,000 indirect acquisition costs. It is determinable that contingency fee of P150,000 (estimated fair value) would be paid within the year.

On January 2, 2022, P Company purchased the net asset of S Company by paying P500,000 cash and issuing 100,000 shares of stocks at P3,000,000 fair market value. The par value of P's shares is P24 per share. Book value and fair value data on the Statement of Financial Positions on January 2, 2022 are as follows: P Company Book Value Fair Value Book Value Fair Value 4,600,000 4,600,000 1,000,000 1,000,000 1,500,000 1,300,000 1,800,000 1,460,000 S Company Cash Accounts Receivable 300,000 980,000 710,000 1,520,000 1,064,000 90,000 3,600,000 3,024,000 300,000 980,000 600,000 Inventory PPE, net Goodwill 80,000 Total 8,900,000 8,360,000 570,000 Liabilities Share Capital Share Premium Retained Earnings 1,000,000 1,600,000 900,000 5,400,000 8,900,000 570,000 600,000 960,000 1,470,000 3,600,000 d1,000,000 Total P incurred and paid legal and brokerage fees of P50,000 for business combination; share issue costs of P30,000 and P20,000 indirect acquisition costs. It is determinable that contingency fee of P150,000 (estimated fair value) would be paid within the year.

Financial Accounting

14th Edition

ISBN:9781305088436

Author:Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:Carl Warren, Jim Reeve, Jonathan Duchac

Chapter15: Investments And Fair Value Accounting

Section: Chapter Questions

Problem 28E

Related questions

Question

Determine:

1. Amount of consideration

2. Amount of

3. Assuming that P Company is an SME, how much is the goodwill or gain?

Transcribed Image Text:On January 2, 2022, P Company purchased the net asset of S Company by

paying P500,000 cash and issuing 100,000 shares of stocks at P3,000,000

fair market value. The par value of P's shares is P24 per share. Book value

and fair value data on the Statement of Financial Positions on January 2,

2022 are as follows:

P Company

Book Value Fair Value

S Company

Book Value Fair Value

Cash

Accounts Receivable

300,000

980,000

600,000

4,600,000

300,000

980,000

710,000

1,520,000 1,064,000

90,000

3,600,000 3,024,000

4,600,000

1,000,000

1,500,000 1,300,000

1,800,000

1,000,000

Inventory

PPE, net

Goodwill

1,460,000

80,000

Total

8,900,000 8,360,000

570,000

Liabilities

Share Capital

Share Premium

Retained Earnings

570,000

600,000

960,000

1,470,000

3,600,000

1,000,000

1,000,000

1,600,000

900,000

5,400,000

8,900,000

Total

P incurred and paid legal and brokerage fees of P50,000 for business

combination; share issue costs of P30,000 and P20,000 indirect acquisition

costs. It is determinable that contingency fee of P150,000 (estimated fair

value) would be paid within the year.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT