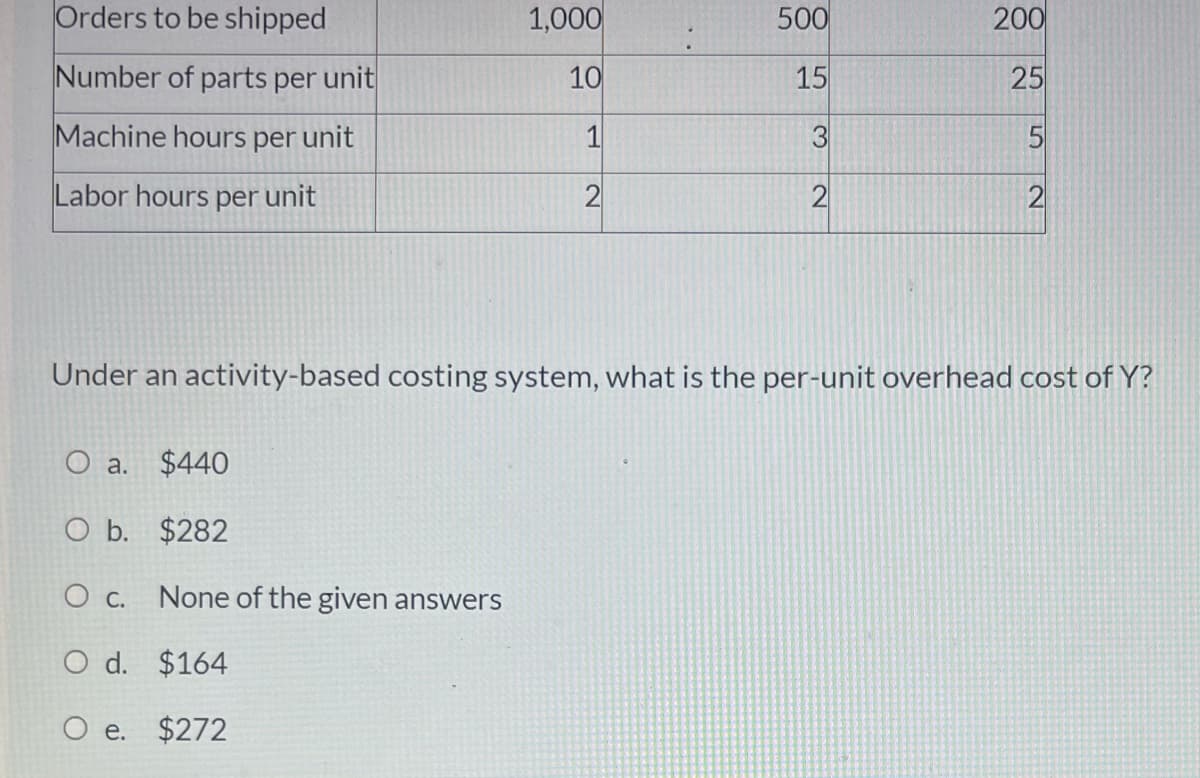

Orders to be shipped 1,000 500 200 Number of parts per unit 10 15 25 Machine hours per unit 1 5 Labor hours per unit 2 Under an activity-based costing system, what is the per-unit overhead cost of Y? a. $440 O b. $282 Oc. None of the given answers O d. $164 21 2)

Q: Standard Price or Rate P6.00 per meter Direct Materials Direct Labor Variable Factory Overhead P3.00…

A: Note: “Since you have posted a question with multiple sub-parts, we will solve first three sub-parts…

Q: Q-5. A company manufactures three products A, B, and C using the same equipment and processes. Data…

A: ABC: It is a costing method. Under this method, the costing of each activity is recorded…

Q: Total Direct Direct Labor- Hours Labor-Hours Expected Production Per Unit Product H2 130 6.3 819…

A: OAR stands for Overhead absorption rate refers to the rate which is charged to the cost unit that is…

Q: Required: 1. As shown above, overhead costs in July amounted to P246,000. Determine how much of this…

A:

Q: 1. Javier Industries manufactures two products: A and B. A review of the company's accounting…

A: In activity based costing, the costs are allocated on the basis of cost driver volume for each…

Q: Administration (MVR) Production Packing (MVR) (MVR) Overheads 6500 5120.7 1201.28 Administration…

A: Under activity based costing, overhead absorption done based on appropriate cost pool base /cost…

Q: Direct labor Direct materials Overhead Total variable overhead Total fixed overhead Expected units…

A: Absorption costing also known as full costing, takes into consideration all the fixed and variable…

Q: Compute conversion costs given the following data: direct materials, $350,600; direct labor,…

A: Conversion cost includes those expenses which are incurred to convert raw material into finished…

Q: PROBLEM 1 ABC Company's total overhead costs at various levels of activity are presented below:…

A: The costs incurred in the production are classified as variable, fixed and mixed cost. The variable…

Q: Using ABC to compute product costs per unit Spectrum Corp. makes two products: C and D. The…

A: 1. Total overhead allocated to product C= (no. of setup x Predetermined overhead rate for setup) +…

Q: allocates manufacturing overhead based on machine hours estimated 10,000 machine hours and $88,000…

A: The question is based on the concept of cost accouting.

Q: Company Dept. A Dept B. Estimated manufacturing overhead $500,000 S338,000 S162,000 Estimated direct…

A: Cost Accounting: It is the process of collecting, recording, analyzing the cost, summarizing cost,…

Q: T2-7 Assign costs to completed units and ending Work in Process Inventory (LO 4) Monk, Inc. reported…

A: Compute the equivalent units for material Beginning inventory $5,900 Added to production…

Q: Factory overhead costs for a given period were 1.5 times as much as the direct material costs. Prime…

A: Conversion Costs = Direct Labor Costs+Factory Overhead Costs

Q: 25. A manufacturing company had actual manufacturing overhead costing of PS00,000 and predetermined…

A: Overhead applied = Actual hours worked x predetermined overhead rate = 200,000 hours x P3 = P600,000

Q: $6 per yard $? ? $3 per direct labor-hour $? the basis of direct labor-hours. During March, 1,C…

A: Solution 1: Computation of Standard cost of a Single Backpack Standard cost for March…

Q: Compute conversion costs given the following data: direct materials, $366,300; direct labor,…

A: Conversion cost = Direct labor cost + Factory overhead cost

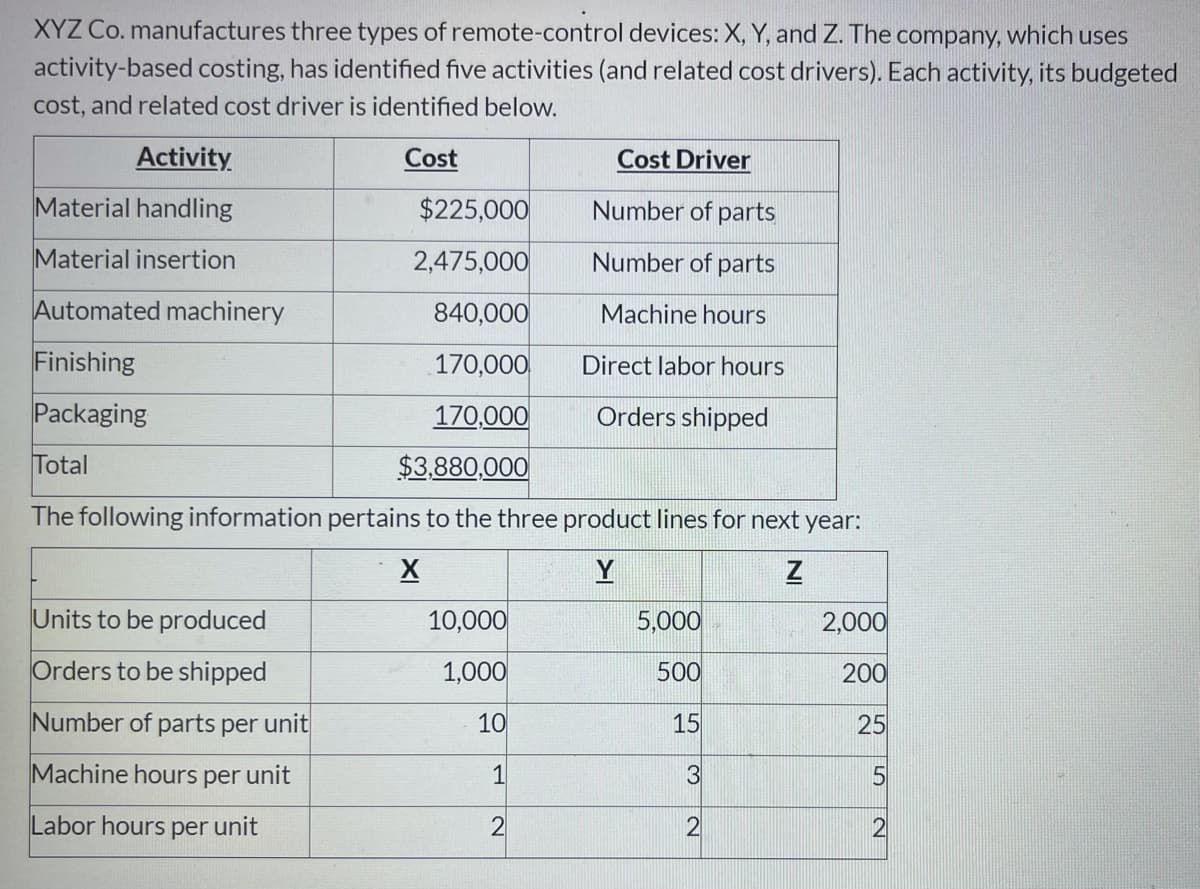

Q: Material handling Material insertion Automated machinery Number of parts Number of parts Finishing…

A: Activity-based costing is where overheads are allocated to various products on the basis of the…

Q: re activities (and related cost drivers). Each s identified below. Cost Driver 5,000 Number of parts…

A: Per unit overhead cost of Y e) $ 272 Activity-based costing (ABC) is a costing method that…

Q: 150 Cost Accounting Problem 9 Miracle Company provides you with the following information January 1…

A: Hi student Since there are multiple questions, we will answer only first question. Cost of goods…

Q: 1. Cost of goods manui ed; prime and converslon costs. Mat Company's Purchases of materials during…

A:

Q: ompany XYZ uses direct labor hours to allocate its manufacturing overhead. Manufacturing overhead…

A: Predetermined overhead allocation rate = Total estimated manufacturing overhead costs / Total…

Q: (a) Direct material cost=90,000 (b) Direct labour is =50,000 (c) Factory overhead=85,000 (d)…

A: Cost of goods sold: =Cost of the production + opening stock - closing stock

Q: Attempts: 1 of1 used (b2) The total estimated manufacturing overhead of $260,000 was comprised of…

A: Predetermined overhead rate: Estimated overhead/ Estimated direct labor hours

Q: Direct materials used OMR 24,000 Direct labor OMR 36,800 Sales salaries OMR 19,200 Indirect labor…

A: Total manufacturing overheads are the sum of all indirect costs incurred in the process of…

Q: 2-Blue Diamond LLC company manufacturing and selling product A & B. Order handling is one of the…

A: Overhead means the cost incurred indirect in factory for the production of goods. Manufacturing…

Q: Standard Price or Rate P6.00 per meter Direct Materials Direct Labor Variable Factory Overhead P3.00…

A: Disclaimer: “Since you have posted a question with multiple sub-parts, we will solve first three…

Q: Direct labor 17 per unit 11 per unit 24 Direct materials Overhead Total variable overhead Total…

A: Formula: Product cost under absorption costing = Direct materials + Direct labor + Variable overhead…

Q: Natio What are the fixed overhead costs of making the component? Do not use money sign. Sample…

A: Solution: Buying cost = P104,000 Avoidable cost to make if company is indifferent making or buying…

Q: Problem No. 2 Below are partial data for overhead costs and activity levels for three different…

A: Lets understand the meaning of under or over applied overhead. When applied overhead more than…

Q: (a) Determine the missing amounts for three different situations. Direct Materials Used Direct Labor…

A: (1) Thus, the total manufacturing cost is $157,300

Q: Standard Quantity Standard Price Standard or Hours ? or Rate $5.00 per yard Cost Direct materials $…

A: Since we only answer up to 3 sub-parts, we’ll answer the first 3. Please resubmit the question and…

Q: Product Volume Material cost per unit (R) Direct Labour Cost per unit (R) Machine Time per unit…

A: Activity based costing (ABC) is the costing method which allocates the overheads on the basis of…

Q: Direct labor Direct materials 17 per unit $4 11 per unit Overhead Total variable overhead Total…

A: Formula: Product cost per unit = Direct materials + Direct labor + Total variable overhead

Q: 150 Cost Accounting Problem 9 Miracle Company provides you with the following information January 1…

A: The question is related to Cost Sheet. The details for the month of January is given. The question…

Q: a. The following data relates to Process Material Input 1,000 units co Labour costs Ghc10…

A: Average Cost per unit = ( Total Cost of inputs - Scrap Value of normal loss)/ ( Units input - Normal…

Q: Manufacturing overhead applied $ 150,000 Actual amount of manufacturing overhead costs 120,000…

A: Overheads are known as the expenses that are incurred to produce the goods. The applied overhead is…

Q: %24 Kesterson Corporation has provided the following information: Cost Cost per Period per Unit…

A: Direct costs are the cost that directly related in manufacturing of goods and services. Indirect…

Q: Determine the missing amounts for three different situations. Direct Materials Direct Total Labor…

A: Manufacturing Costs = Direct Materials + Direct Labour + Factory Overheds Cost of goods manufactured…

Q: Problem 3 plant-wide overhead rate is used based on direct labor hours as cost allocation base.…

A: By dividing the production overhead cost by the activity driver, the predetermined overhead rate is…

Q: Integrity Company uses standard costing for each specialized product. The following information is…

A: When direct materials are purchased, their cost is debited to Raw Materials inventory and the…

Q: Direct Labor = $2.25 Materials =…

A: Incremental analysis or differential analysis is a technique in decision making which identifies the…

Q: Direct materials used OMR 24,000 Direct labor OMR 36,800 Sales salaries OMR 19,200 Indirect labor…

A: The manufacturing cost includes all the expenses that are related in the process of manufacturing.

Q: Subject: Cost management & accounting Q.9) Compute: i) Factory Overhead ii) Conversion Cost…

A: Factory overhead is the indirect expense and can be calculated by deducting the prime cost from the…

Q: $10,000 Sales (100 units at $100 a unit). Manufacturing cost of good sold Direct Labor. . Direct…

A: The Break-even point represents the situation where the company does not earn a profit or incur a…

Q: Prob 3. Mabini company uses a standard cost system for its machine paced production of telephone…

A: In the above question, we have to calculate different variances using the given data.

Q: Number of Number of Number of Setups Components Direct Labor Hours Product 13 10 290 Sandard 32 18…

A: Using traditional method, the predetermined overhead rate is calculated as estimated overhead cost…

Step by step

Solved in 3 steps

- Lonsdale Inc. manufactures entry and dining room lighting fixtures. Five activities are used in manufacturing the fixtures. These activities and their associated budgeted activity costs and activity bases are as follows: Corporate records were obtained to estimate the amount of activity to be used by the two products. The estimated activity-base usage quantities and units produced follow: a. Determine the activity rate for each activity. b. Use the activity rates in (a) to determine the total and per-unit activity costs associated with each product. Round to the nearest cent.Evans, Inc., has a unit-based costing system. Evanss Miami plant produces 10 different electronic products. The demand for each product is about the same. Although they differ in complexity, each product uses about the same labor time and materials. The plant has used direct labor hours for years to assign overhead to products. To help design engineers understand the assumed cost relationships, the Cost Accounting Department developed the following cost equation. (The equation describes the relationship between total manufacturing costs and direct labor hours; the equation is supported by a coefficient of determination of 60 percent.) Y=5,000,000+30X,whereX=directlaborhours The variable rate of 30 is broken down as follows: Because of competitive pressures, product engineering was given the charge to redesign products to reduce the total cost of manufacturing. Using the above cost relationships, product engineering adopted the strategy of redesigning to reduce direct labor content. As each design was completed, an engineering change order was cut, triggering a series of events such as design approval, vendor selection, bill of materials update, redrawing of schematic, test runs, changes in setup procedures, development of new inspection procedures, and so on. After one year of design changes, the normal volume of direct labor was reduced from 250,000 hours to 200,000 hours, with the same number of products being produced. Although each product differs in its labor content, the redesign efforts reduced the labor content for all products. On average, the labor content per unit of product dropped from 1.25 hours per unit to one hour per unit. Fixed overhead, however, increased from 5,000,000 to 6,600,000 per year. Suppose that a consultant was hired to explain the increase in fixed overhead costs. The consultants study revealed that the 30 per hour rate captured the unit-level variable costs; however, the cost behavior of other activities was quite different. For example, setting up equipment is a step-fixed cost, where each step is 2,000 setup hours, costing 90,000. The study also revealed that the cost of receiving goods is a function of the number of different components. This activity has a variable cost of 2,000 per component type and a fixed cost that follows a step-cost pattern. The step is defined by 20 components with a cost of 50,000 per step. Assume also that the consultant indicated that the design adopted by the engineers increased the demand for setups from 20,000 setup hours to 40,000 setup hours and the number of different components from 100 to 250. The demand for other non-unit-level activities remained unchanged. The consultant also recommended that management take a look at a rejected design for its products. This rejected design increased direct labor content from 250,000 hours to 260,000 hours, decreased the demand for setups from 20,000 hours to 10,000 hours, and decreased the demand for purchasing from 100 component types to 75 component types, while the demand for all other activities remained unchanged. Required: 1. Using normal volume, compute the manufacturing cost per labor hour before the year of design changes. What is the cost per unit of an average product? 2. Using normal volume after the one year of design changes, compute the manufacturing cost per hour. What is the cost per unit of an average product? 3. Before considering the consultants study, what do you think is the most likely explanation for the failure of the design changes to reduce manufacturing costs? Now use the information from the consultants study to explain the increase in the average cost per unit of product. What changes would you suggest to improve Evanss efforts to reduce costs? 4. Explain why the consultant recommended a second look at a rejected design. Provide computational support. What does this tell you about the strategic importance of cost management?Eclipse Motor Company manufactures two types of specialty electric motors, a commercial motor and a residential motor, through two production departments, Assembly and Testing. Presently, the company uses a single plantwide factory overhead rate for allocating factory overhead to the two products. However, management is considering using the multiple production department factory overhead rate method. The following factory overhead was budgeted for Eclipse: Direct machine hours were estimated as follows: In addition, the direct machine hours (dmh) used to produce a unit of each product in each department were determined from engineering records, as follows: a. Determine the per-unit factory overhead allocated to the commercial and residential motors under the single plantwide factory overhead rate method, using direct machine hours as the allocation base. b. Determine the per-unit factory overhead allocated to the commercial and residential motors under the multiple production department factory overhead rate method, using direct machine hours as the allocation base for each department. c. Recommend to management a product costing approach, based on your analyses in (a) and (b). Support your recommendation.

- Pelder Products Company manufactures two types of engineering diagnostic equipment used in construction. The two products are based upon different technologies, X-ray and ultrasound, but are manufactured in the same factory. Pelder has computed the manufacturing cost of the X-ray and ultrasound products by adding together direct materials, direct labor, and overhead cost applied based on the number of direct labor hours. The factory has three overhead departments that support the single production line that makes both products. Budgeted overhead spending for the departments is as follows: Pelders budgeted manufacturing activities and costs for the period are as follows: The budgeted cost to manufacture one ultrasound machine using the activity-based costing method is: a. 225. b. 264. c. 293. d. 305.Firenza Company manufactures specialty tools to customer order. Budgeted overhead for the coming year is: Previously, Sanjay Bhatt, Firenza Companys controller, had applied overhead on the basis of machine hours. Expected machine hours for the coming year are 50,000. Sanjay has been reading about activity-based costing, and he wonders whether or not it might offer some advantages to his company. He decided that appropriate drivers for overhead activities are purchase orders for purchasing, number of setups for setup cost, engineering hours for engineering cost, and machine hours for other. Budgeted amounts for these drivers are 5,000 purchase orders, 500 setups, and 2,500 engineering hours. Sanjay has been asked to prepare bids for two jobs with the following information: The typical bid price includes a 40 percent markup over full manufacturing cost. Required: 1. Calculate a plantwide rate for Firenza Company based on machine hours. What is the bid price of each job using this rate? 2. Calculate activity rates for the four overhead activities. What is the bid price of each job using these rates? 3. Which bids are more accurate? Why?Douglas Davis, controller for Marston, Inc., prepared the following budget for manufacturing costs at two different levels of activity for 20X1: During 20X1, Marston worked a total of 80,000 direct labor hours, used 250,000 machine hours, made 32,000 moves, and performed 120 batch inspections. The following actual costs were incurred: Marston applies overhead using rates based on direct labor hours, machine hours, number of moves, and number of batches. The second level of activity (the right column in the preceding table) is the practical level of activity (the available activity for resources acquired in advance of usage) and is used to compute predetermined overhead pool rates. Required: 1. Prepare a performance report for Marstons manufacturing costs in the current year. 2. Assume that one of the products produced by Marston is budgeted to use 10,000 direct labor hours, 15,000 machine hours, and 500 moves and will be produced in five batches. A total of 10,000 units will be produced during the year. Calculate the budgeted unit manufacturing cost. 3. One of Marstons managers said the following: Budgeting at the activity level makes a lot of sense. It really helps us manage costs better. But the previous budget really needs to provide more detailed information. For example, I know that the moving materials activity involves the use of forklifts and operators, and this information is lost when only the total cost of the activity for various levels of output is reported. We have four forklifts, each capable of providing 10,000 moves per year. We lease these forklifts for five years, at 10,000 per year. Furthermore, for our two shifts, we need up to eight operators if we run all four forklifts. Each operator is paid a salary of 30,000 per year. Also, I know that fuel costs about 0.25 per move. Assuming that these are the only three items, expand the detail of the flexible budget for moving materials to reveal the cost of these three resource items for 20,000 moves and 40,000 moves, respectively. Based on these comments, explain how this additional information can help Marston better manage its costs. (Especially consider how activity-based budgeting may provide useful information for non-value-added activities.)

- Bach Instruments Inc. makes three musical instruments: flutes, clarinets, and oboes. The budgeted factory overhead cost is 2,948,125. Overhead is allocated to the three products on the basis of direct labor hours. The products have the following budgeted production volume and direct labor hours per unit: a. Determine the single plant wide overhead rate. b. Use the overhead rate in (a) to determine the amount of total and per-unit overhead allocated to each of the three products, rounded to the nearest dollar.Young Company is beginning operations and is considering three alternatives to allocate manufacturing overhead to individual units produced. Young can use a plantwide rate, departmental rates, or activity-based costing. Young will produce many types of products in its single plant, and not all products will be processed through all departments. In which one of the following independent situations would reported net income for the first year be the same regardless of which overhead allocation method had been selected? a. All production costs approach those costs that were budgeted. b. The sales mix does not vary from the mix that was budgeted. c. All manufacturing overhead is a fixed cost. d. All ending inventory balances are zero.Botella Company produces plastic bottles. The unit for costing purposes is a case of 18 bottles. The following standards for producing one case of bottles have been established: During December, 78,000 pounds of materials were purchased and used in production. There were 15,000 cases produced, with the following actual prime costs: Required: 1. Compute the materials variances. 2. Compute the labor variances. 3. CONCEPTUAL CONNECTION What are the advantages and disadvantages that can result from the use of a standard costing system?

- Sanford, Inc., has developed value-added standards for four activities: purchasing parts, receiving parts, moving parts, and setting up equipment. The activities, the activity drivers, the standard and actual quantities, and the price standards for 20x1 are as follows: The actual prices paid per unit of each activity driver were equal to the standard prices. Required: 1. Prepare a cost report that lists the value-added, non-value-added, and actual costs for each activity. 2. Which activities are non-value-added? Explain why. Also, explain why value-added activities can have non-value-added costs.Stacks manufactures two different levels of hockey sticks: the Standard and the Slap Shot. The total overhead of $600,000 has traditionally been allocated by direct labor hours, with 400,000 hours for the Standard and 200.000 hours for the Slap Shot. After analyzing and assigning costs to two cost pools, it was determined that machine hours is estimated to have $450.000 of overhead, with 30,000 hours used on the Standard product and 15,000 hours used on the Slap Shot product. It was also estimated that the inspection cost pool would have $150,000 of overhead, with 25,000 hours for the Standard and 5,000 hours for the Slap Shot. What is the overhead rate per product, under traditional and under ABC costing?Minor Co. has a job order cost system and applies overhead based on departmental rates. Service Department 1 has total budgeted costs of 168,000 for next year. Service Department 2 has total budgeted costs of 280,000 for next year. Minor allocates service department costs solely to the producing departments. Service Department 1 cost is allocated to producing departments on the basis of machine hours. Service Department 2 cost is allocated to producing departments on the basis of direct labor hours. Producing Department 1 has budgeted 8,000 machine hours and 12,000 direct labor hours. Producing Department 2 has budgeted 2,000 machine hours and 12,000 direct labor hours. What is the total cost allocation from the two service departments to Producing Department 1? a. 173,600 b. 140,000 c. 134,400 d. 274,400