QUESTION 7 Review the following figure. Suppose the price of gasoline is $1.60 per gallon. . What would happen to the quantity demanded? . What would happen to the quantity supplied? . At $1.60, is the market in equilibrium, a shortage, or a surplus? P ($ per gallon) $2.20 $1.80 $1.40 $1.20 $1.00 50.60 Excess supply or surplus S An above-equilibrium price Equilibrium price A below equilibrium price Excess demand or shortage D 300 400 500 600 700 800 900 Quantity of Gasoline (millions of gallons) rise fall surplus shortage no change a shift in demand a shift in supply

QUESTION 7 Review the following figure. Suppose the price of gasoline is $1.60 per gallon. . What would happen to the quantity demanded? . What would happen to the quantity supplied? . At $1.60, is the market in equilibrium, a shortage, or a surplus? P ($ per gallon) $2.20 $1.80 $1.40 $1.20 $1.00 50.60 Excess supply or surplus S An above-equilibrium price Equilibrium price A below equilibrium price Excess demand or shortage D 300 400 500 600 700 800 900 Quantity of Gasoline (millions of gallons) rise fall surplus shortage no change a shift in demand a shift in supply

Principles of Economics 2e

2nd Edition

ISBN:9781947172364

Author:Steven A. Greenlaw; David Shapiro

Publisher:Steven A. Greenlaw; David Shapiro

Chapter3: Demand And Supply

Section: Chapter Questions

Problem 53P: Table 3.8 shows information on the demand and supply for bicycles, where the quantities of bicycles...

Related questions

Question

Q7.

Select 1 answer for each question.

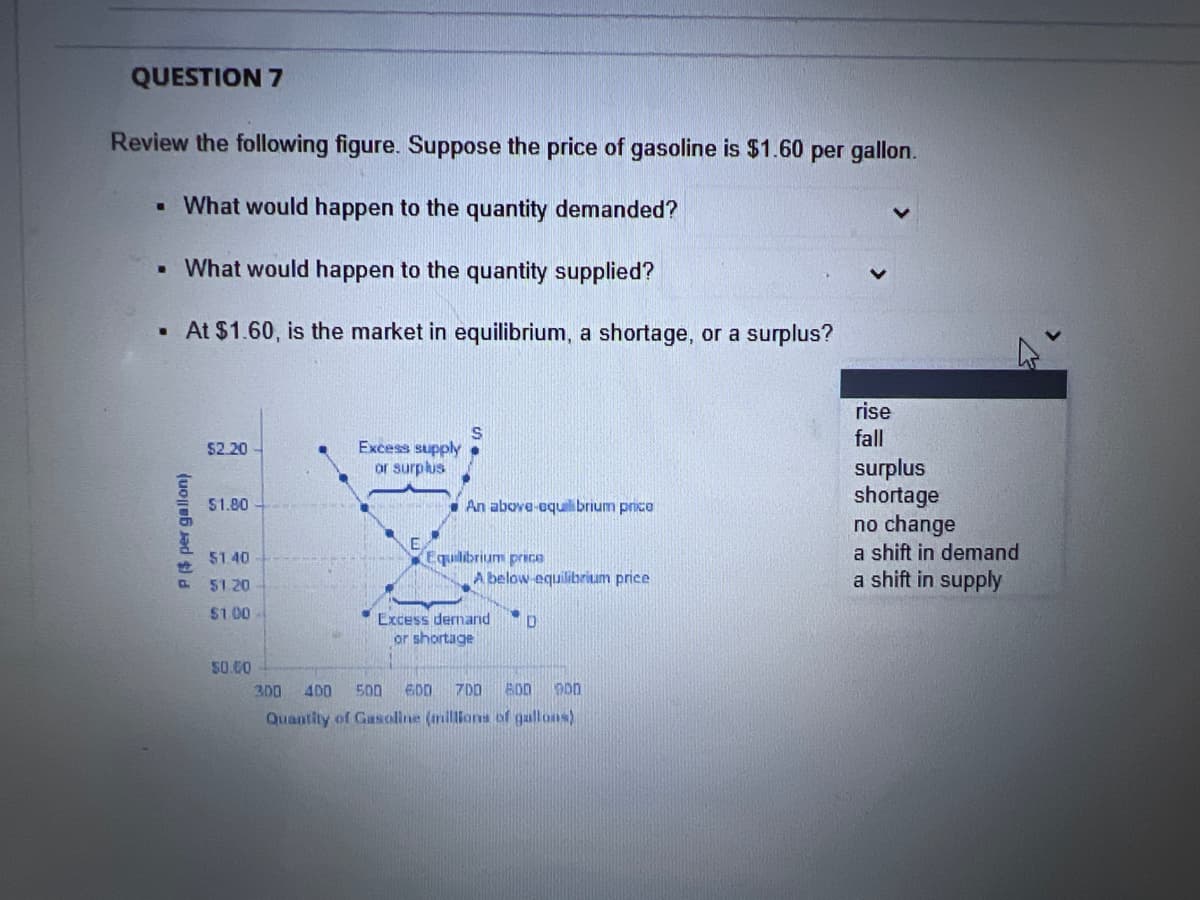

Transcribed Image Text:QUESTION 7

Review the following figure. Suppose the price of gasoline is $1.60 per gallon.

▪ What would happen to the quantity demanded?

. What would happen to the quantity supplied?

. At $1.60, is the market in equilibrium, a shortage, or a surplus?

P ($ per gallon)

$2.20

$1.80

$1.40

$1.20

$1.00

50.60

Excess supply

or surplus

An above-aquilibrium price

Equilibrium price

A below-equilibrium price

Excess demand D

or shortage

300 400 500 600 700 800 900

Quantity of Gasoline (millions of gallons)

rise

fall

surplus

shortage

no change

a shift in demand

a shift in supply

Expert Solution

Introduction

Market equilibrium: At the market equilibrium we have demand equals to supply. Or at market equilibrium point the maximum price which the consumers are willing to pay is exactly equals the minimum price at which the sellers are willing to sell.

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Economics 2e

Economics

ISBN:

9781947172364

Author:

Steven A. Greenlaw; David Shapiro

Publisher:

OpenStax

Principles of Microeconomics

Economics

ISBN:

9781305156050

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Brief Principles of Macroeconomics (MindTap Cours…

Economics

ISBN:

9781337091985

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Principles of Economics 2e

Economics

ISBN:

9781947172364

Author:

Steven A. Greenlaw; David Shapiro

Publisher:

OpenStax

Principles of Microeconomics

Economics

ISBN:

9781305156050

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Brief Principles of Macroeconomics (MindTap Cours…

Economics

ISBN:

9781337091985

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Microeconomics: Principles & Policy

Economics

ISBN:

9781337794992

Author:

William J. Baumol, Alan S. Blinder, John L. Solow

Publisher:

Cengage Learning

Exploring Economics

Economics

ISBN:

9781544336329

Author:

Robert L. Sexton

Publisher:

SAGE Publications, Inc