Review Figure 3.4. Suppose the

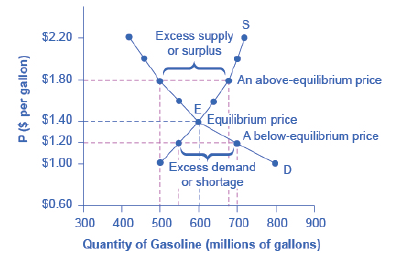

Figure 3.4 Demand and Supply of Gasoline

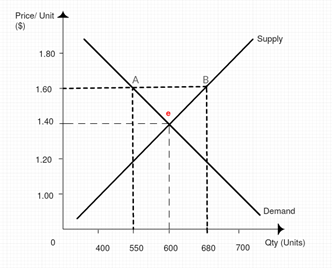

If the price of gasoline is $1.60 per gallon and the equilibrium price is $1.40 per gallon. Comment whether the quantity demanded and supplied is higher or lower at $1.60 per gallon. Is there a shortage or surplus?

Explanation of Solution

As per the diagram, the equilibrium price is $1.40 per gallon in the market. Any price above the equilibrium price level in the market creates surplus of the product in the market and any price below the equilibrium price creates a shortage of the product in the market.

In the above figure, at price level $1.60 per gallon, the quantity demand is 550 millions of gallons and quantity supply is 680 million gallons, represented by point A and B in the diagram. Clearly, we can see that quantity supply is more than quantity demand and there is a surplus of the product.

If the price is below the equilibrium price, then there will be shortage of the product.

Equilibrium Price: It is that level of price where demand of a product is equal to the supply of a product.

Want to see more full solutions like this?

Chapter 3 Solutions

Principles of Economics 2e

Additional Business Textbook Solutions

Principles of Accounting Volume 2

Cost Accounting (15th Edition)

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

Managerial Accounting (5th Edition)

Financial Accounting (12th Edition) (What's New in Accounting)

Construction Accounting And Financial Management (4th Edition)

- Only typed answer and please answer correctlyarrow_forwardThe table shows the quantity of tablets that is demanded and supplied at various prices. Quantity Demanded Quantity Supplied Price 50 75 100 125 120,000 112,500 105,000 97,500 100,000 102,500 105,000 107,500 Assume that the new equilibrium price is $50. How much would quantity supplied need to increase at each price to reach this equilibrium? A) 2550 B) 5050 C) 20,000 D) 112,499arrow_forwardThe table gives the demand and supply schedules for milkshakes. What is the equilibrium price of a milkshake and the equilibrium quantity of milkshakes per day? The equilibrium quantity of milkshakes is The equilibrium price is $ a milkshake. a day. This question: 1 point(s) possible Price (dollars per milkshake) 4 5 6 Quantity demanded (per day) 120 120 105 90 75 60 45 Quantity supplied (per day) 30 45 60 75 90 105arrow_forward

- Suppose the price of gasoline is $1.60 per gallon. Is the quantity demanded higher or lower than at the equilibrium price of $1.40 per gallon? What about the quantity supplied? Is there a shortage or a surplus in the market? If so, how much?arrow_forwardUsing the following schedule, (5) find the equilibrium price and quantity. (6) Describe the situation at a price of $10. What will occur to price? (7) Describe the situation at a price of $2. What will occur to price? price Quantity demanded Quantity supplied $ 1 500 100 $2 400 120 $3 350 150 $4 320 200 $5 300 300 $6 275 410 $7 260 500 $8 230 650 $9 200 800 $10 150 975arrow_forward1. Demand terminology Complete the following table by selecting the term that matches each definition. Definition The claim that, with other things being equal, the quantity demanded of a good falls when the price of that good rises A table showing the relationship between the price of a good and the amount that buyers are willing and able to purchase at various prices A graphical object showing the relationship between the price of a good and the amount of the good that buyers are willing and able to purchase at various prices The amount of a good that buyers are willing and able to purchase at a given price Law of Quantity Demand Demand Demanded Curve Schedule Demand O O O O O O O O O Apply your understanding of the previous key terms by completing the following scenario with the appropriate terminology. Your friend Bob struggles with understanding graphs. He shows you the following illustration and asks for your help interpreting it: O O Oarrow_forward

- Draw a supply and demand graph for the market for air travel. Analyze the impact of an increase in the cost of jet fuel. Be sure to use just one graph, shifting either the demand curve or the supply curve the correct direction. Show the impact on equilibrium price and equilibrium quantity.arrow_forwardPlease don't give an handmade diagram. Make diagram with a digital tool.arrow_forwardFind the equilibrium price and quantity for a product that has the following supply and demand curves, where p is the price in 100's of dollars and q is quantities in 1,000's of units demand: 1/3q + 1/3p - 4=0 Supply: q-p-2=0 If the product is currently priced at $400, what is the quantity supplied and the quantity demanded? Is there a surplus (More supplied than demanded) or a shortage (More demanded than supplied)arrow_forward

- What happen if Demand of petrol is higher than Supply. Make answer in 1 paragrapharrow_forwardQ4 Which of the following statements about the consumers’ responses to rising gasoline prices is correct? Because gasoline is a necessity, consumers do not decrease their quantity demanded in either the short run or the long run. About 10 percent of the long-run reduction in quantity demanded arises because people drive less and about 90 percent arises because they switch to more fuel-efficient cars. About 90 percent of the long-run reduction in quantity demanded arises because people drive less and about 10 percent arises because they switch to more fuel-efficient cars. About half of the long-run reduction in quantity demanded arises because people drive less and about half arises because they switch to more fuel-efficient cars.arrow_forwardSuppose the price of gasoline is $1.00. Will the quantity demanded be lower or higher than at the equilibrium price of $1.40 per gallon? Will the quantity supplied be lower or higher? Is there a shortage or a surplus in the market? If so, of how much?arrow_forward

Principles of Economics 2eEconomicsISBN:9781947172364Author:Steven A. Greenlaw; David ShapiroPublisher:OpenStax

Principles of Economics 2eEconomicsISBN:9781947172364Author:Steven A. Greenlaw; David ShapiroPublisher:OpenStax Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning

Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning

Principles of MicroeconomicsEconomicsISBN:9781305156050Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of MicroeconomicsEconomicsISBN:9781305156050Author:N. Gregory MankiwPublisher:Cengage Learning Brief Principles of Macroeconomics (MindTap Cours...EconomicsISBN:9781337091985Author:N. Gregory MankiwPublisher:Cengage Learning

Brief Principles of Macroeconomics (MindTap Cours...EconomicsISBN:9781337091985Author:N. Gregory MankiwPublisher:Cengage Learning