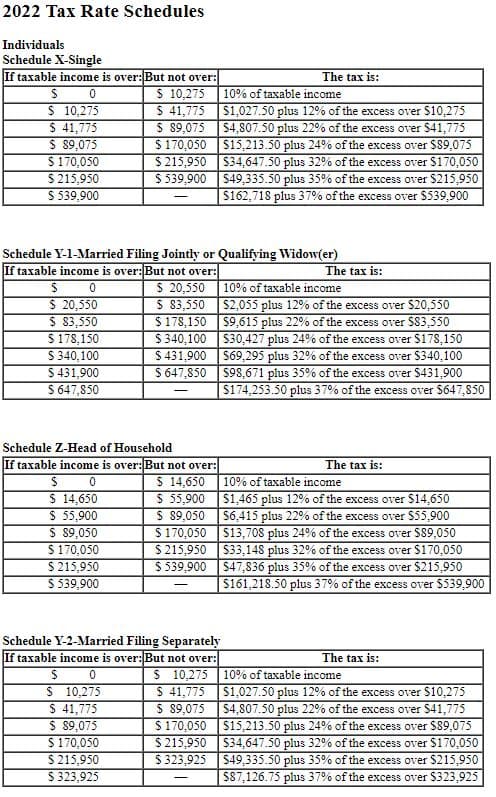

Eva received $72,000 in compensation payments from JAZZ Corporation during 2022. Eva incurred $10,500 in business expenses relating to her work for JAZZ Corporation JAZZ did not reimburse Eva for any of these expenses. Eva is single and deducts a standard deduction of $12,950. Based on these facts, answer the following questions: Use Tax Rate Schedule for reference. Note: Leave no answer blank. Enter zero if applicable. Round your intermediate and final answers to the nearest whole dollar amount. Required: Assume that Eva is considered to be an employee. What amount of FICA taxes is she required to pay for the year? Assume that Eva is considered to be an employee. What is her regular income tax liability for the year? Assume that Eva is considered to be a self-employed contractor. What are her self-employment tax liability and additional Medicare tax liability for the year? Assume that Eva is considered to be a self-employed contractor. What is her regular tax liability for the year?

Eva received $72,000 in compensation payments from JAZZ Corporation during 2022. Eva incurred $10,500 in business expenses relating to her work for JAZZ Corporation JAZZ did not reimburse Eva for any of these expenses. Eva is single and deducts a standard deduction of $12,950. Based on these facts, answer the following questions: Use Tax Rate Schedule for reference.

Note: Leave no answer blank. Enter zero if applicable. Round your intermediate and final answers to the nearest whole dollar amount.

Required:

- Assume that Eva is considered to be an employee. What amount of FICA taxes is she required to pay for the year?

- Assume that Eva is considered to be an employee. What is her regular income tax liability for the year?

- Assume that Eva is considered to be a self-employed contractor. What are her self-employment tax liability and additional Medicare tax liability for the year?

- Assume that Eva is considered to be a self-employed contractor. What is her regular tax liability for the year?

Trending now

This is a popular solution!

Step by step

Solved in 4 steps with 4 images

Reposing as Requested to answer subpart 4 only. Thank you. (Subpart is bolded and underlined.

Eva received $72,000 in compensation payments from JAZZ Corporation during 2022. Eva incurred $10,500 in business expenses relating to her work for JAZZ Corporation JAZZ did not reimburse Eva for any of these expenses. Eva is single and deducts a standard deduction of $12,950. Based on these facts, answer the following questions: Use Tax Rate Schedule for reference.

Note: Leave no answer blank. Enter zero if applicable. Round your intermediate and final answers to the nearest whole dollar amount.

Required:

- Assume that Eva is considered to be an employee. What amount of FICA taxes is she required to pay for the year?

- Assume that Eva is considered to be an employee. What is her regular income tax liability for the year?

- Assume that Eva is considered to be a self-employed contractor. What are her self-employment tax liability and additional Medicare tax liability for the year?

- Assume that Eva is considered to be a self-employed contractor. What is her regular tax liability for the year?