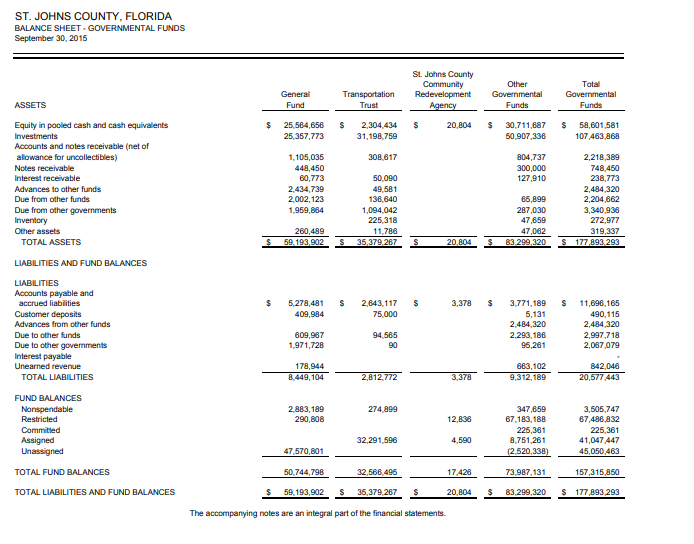

ST. JOHNS COUNTY, FLORIDA BALANCE SHEET-GOVERNMENTAL FUNDS September 30, 2015 St. Johns County Transportation Redevelopment Governmental Govenmental Equity in pooled cash and cash equivalents $25,584,658 2,304,434 S 20,804 30,711,687 58,601,581 107,463,868 Accounts and notes receivable (net of Advances to ather funds LIABILITIES AND FUND BALANCES $5,278,481 2,843,117 S 3,378 3,771,189 11,696,165 Advances from other funds 8.449,1042,812,7723,378 9312,18920,577443 274,899 2,838 Committed 4,590 41,047 447 32,568 496 17,428 TOTAL LIABILITIES AND FUND BALANCES 59,193,902 35,379,267 S 20,804 83,299,320 177,893 293 The accompanying notes are an integral part of the financial statements.

Using the Balance Sheet in the St. Johns County, Florida 2015 CAFR calculate the following ratios for each of the five (5) funds shown and for the “Total Governmental Funds:”

a. Current Ratio

b. Net Working Capital

c. Debt Ratio 1

d. Debt Ratio 2

e. Unrestricted Net Assets Ratio

f. Response Ratio

Reconciliation of the Governmental Funds Balance Sheet

to the Statement of Net Position September 30, 2015

Total fund balances- governmental funds $ 157,315,850

Amounts reported for governmental activities in the statement of net

position are different because:

Capital assets used in governmental activities are not current financial

resources and therefore are not reported in the governmental funds. 1,241,213,205

Net OPEB obligations are created through the estimated calculation of the county's

employer contribution toward the retiree's benefits. The amount greater or less than the 5,549,497

annual required contribution is posted as an asset/(liability).

Deferred outflows for bond refunding losses are not reported in the governmental funds. 10,107,759

Deferred pension outflows are not reported in the governmental funds. 38,159,262

Bonds and notes payable ($201,892,655); unamortized bond premiums and

discounts (14,487,603); lease obligations ($4,811,609); compensated absences for

governmental funds ($10,170,840); and net pension liabilities ($87,159,647) are not due

and payable in the current period and therefore are not reported in the funds. (318,522,354)

Accrued interest payable is not reported in the governmental funds. (1,308,354)

Deferred pension inflows are not reported in the governmental funds. (37,379,857)

Internal service funds are used by management to charge the costs of certain activities,

such as insurance, to individual funds. The assets and liabilities of internal service

funds are included in governmental activities in the statement of net assets. 8,330,909

Net position of governmental activities $ 1,103,465,917

Step by step

Solved in 2 steps with 2 images