The management of NUBDCorporation is considering dropping product D4. Data from the company's accounting system appear below: Sales "Variable expenses Fixed manufacturing expenses. Fixed selling and administrative expenses. P830,000 P390,000 P266,000 P232,000 All fixed expenses of the company are fully allocated to products in the company's accounting system. Further investigation has revealed that 50% of the fixed manufacturing expenses and P105,000 of the fixed selling and administrative expenses are avoidable if product D4 is discontinued.

The management of NUBDCorporation is considering dropping product D4. Data from the company's accounting system appear below: Sales "Variable expenses Fixed manufacturing expenses. Fixed selling and administrative expenses. P830,000 P390,000 P266,000 P232,000 All fixed expenses of the company are fully allocated to products in the company's accounting system. Further investigation has revealed that 50% of the fixed manufacturing expenses and P105,000 of the fixed selling and administrative expenses are avoidable if product D4 is discontinued.

Financial And Managerial Accounting

15th Edition

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:WARREN, Carl S.

Chapter21: Variable Costing For Management

analysis

Section: Chapter Questions

Problem 4CMA: Bethany Company has just completed the first month of producing a new product but has not yet...

Related questions

Question

What would be the effect on the company's overall net operating income if product D4 were dropped?

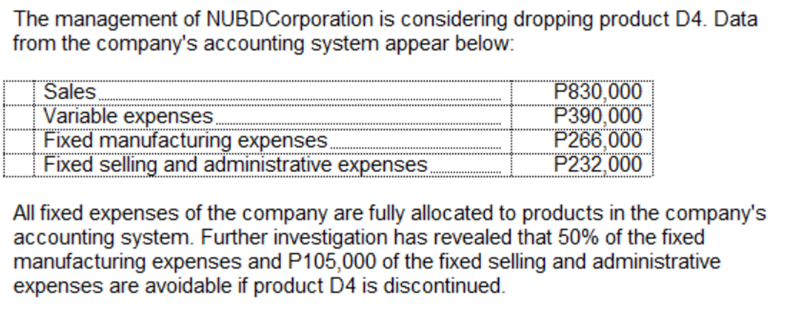

Transcribed Image Text:The management of NUBDCorporation is considering dropping product D4. Data

from the company's accounting system appear below:

Sales

Variable expenses.

Fixed manufacturing expenses.

Fixed selling and administrative expenses.

P830,000

P390,000

P266,000

P232,000

All fixed expenses of the company are fully allocated to products in the company's

accounting system. Further investigation has revealed that 50% of the fixed

manufacturing expenses and P105,000 of the fixed selling and administrative

expenses are avoidable if product D4 is discontinued.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning