Third Quarter Unit Cost Report, Activity-Based Costing-CenterPoint Manufacturing Facility Sport $1,500,000 Pro $2,400,000 Direct material Direct labor Assembly Packaging Total direct labor Direct costs Overhead Assembly building Assembling (@ $30 per MH) Setting up machine (@ $900 per setup hour) Handling material (@ $3, 000 per run) Packaging building Inspecting and packing (@ $5_per direct labor-hour) Shipping (@ $1,320 per shipment) Total ABC overhead $ 750,000 990,000 $1,740,000 $3,240,000 600,000 360,000 $ 960,000 $3,360,000 $ $ 180,000 36,000 24,000 $ 900,000 360,000 120,000 300,000 132,000 $ 672,000 114,000 264,000 $1,758,000 $5,118,000 40,000 $ Total ABC cost $3,912,000 100,000 Number of units Unit cost $ 39.12 127.95 Required: a. Compute the amount of overhead allocated to the Sport and the Pro drones for the first quarter using activity-based costing. Assume that all events are the same in the first quarter as in the third quarter except for the number of setup hours. Assume the cost of a setup hour remains at $900. Total ABC Model Overhead Sport Pro

Third Quarter Unit Cost Report, Activity-Based Costing-CenterPoint Manufacturing Facility Sport $1,500,000 Pro $2,400,000 Direct material Direct labor Assembly Packaging Total direct labor Direct costs Overhead Assembly building Assembling (@ $30 per MH) Setting up machine (@ $900 per setup hour) Handling material (@ $3, 000 per run) Packaging building Inspecting and packing (@ $5_per direct labor-hour) Shipping (@ $1,320 per shipment) Total ABC overhead $ 750,000 990,000 $1,740,000 $3,240,000 600,000 360,000 $ 960,000 $3,360,000 $ $ 180,000 36,000 24,000 $ 900,000 360,000 120,000 300,000 132,000 $ 672,000 114,000 264,000 $1,758,000 $5,118,000 40,000 $ Total ABC cost $3,912,000 100,000 Number of units Unit cost $ 39.12 127.95 Required: a. Compute the amount of overhead allocated to the Sport and the Pro drones for the first quarter using activity-based costing. Assume that all events are the same in the first quarter as in the third quarter except for the number of setup hours. Assume the cost of a setup hour remains at $900. Total ABC Model Overhead Sport Pro

Financial And Managerial Accounting

15th Edition

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:WARREN, Carl S.

Chapter18: Activity-based Costing

Section: Chapter Questions

Problem 13E: Handbrain Inc. is considering a change to activity-based product costing. The company produces two...

Related questions

Question

Hello question is attached, thanks.

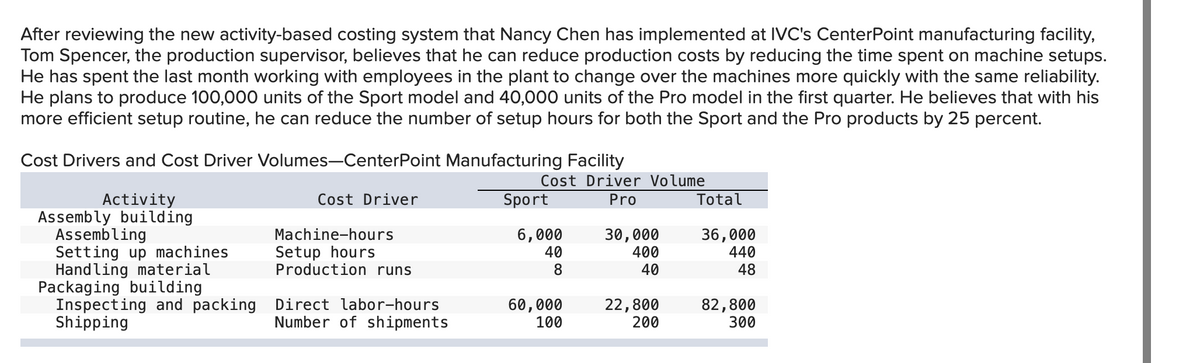

Transcribed Image Text:After reviewing the new activity-based costing system that Nancy Chen has implemented at IVC's CenterPoint manufacturing facility,

Tom Spencer, the production supervisor, believes that he can reduce production costs by reducing the time spent on machine setups.

He has spent the last month working with employees in the plant to change over the machines more quickly with the same reliability.

He plans to produce 100,000 units of the Sport model and 40,000 units of the Pro model in the first quarter. He believes that with his

more efficient setup routine, he can reduce the number of setup hours for both the Sport and the Pro products by 25 percent.

Cost Drivers and Cost Driver Volumes-CenterPoint Manufacturing Facility

Cost Driver Volume

Activity

Cost Driver

Sport

Pro

Total

Assembly building

Assembling

Setting up machines

Handling material

Packaging building

Inspecting and packing Direct labor-hours

Shipping

6,000

40

30,000

400

40

36,000

440

Machine-hours

Setup hours

Production runs

48

60,000

100

22,800

200

82,800

300

Number of shipments

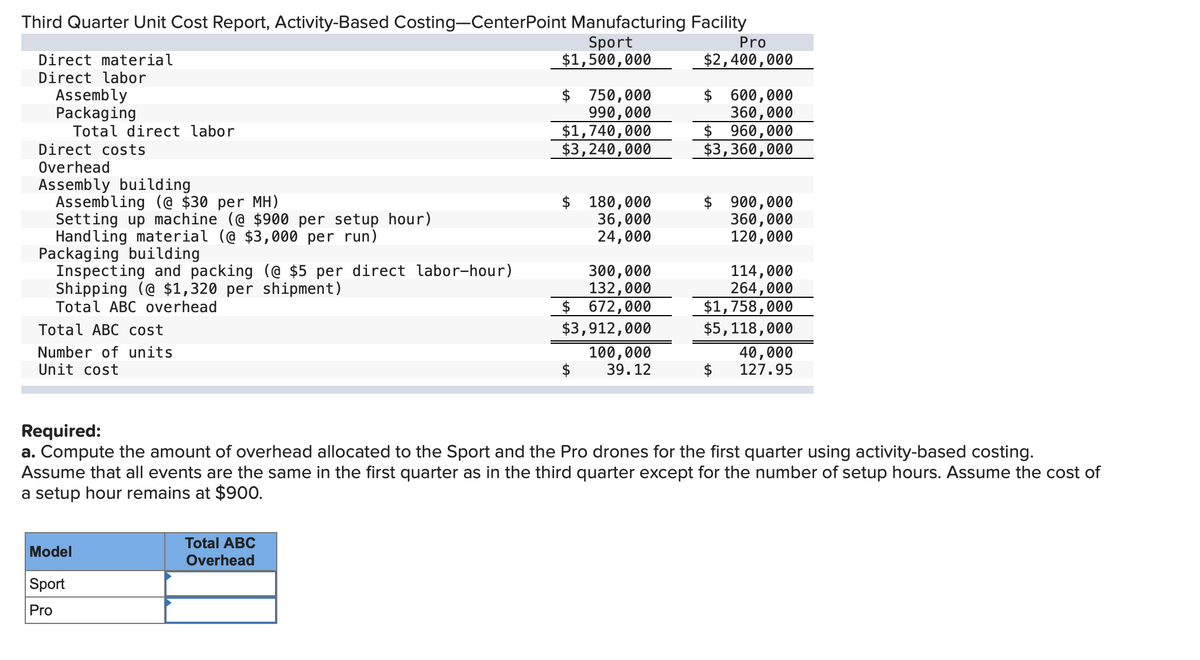

Transcribed Image Text:Third Quarter Unit Cost Report, Activity-Based Costing-CenterPoint Manufacturing Facility

Sport

$1,500,000

Pro

Direct material

$2,400,000

Direct labor

Assembly

Packaging

Total direct labor

$ 750,000

990,000

$1,740,000

$3,240,000

$ 600,000

360,000

$ 960,000

$3,360,000

Direct costs

Overhead

Assembly building

Assembling (@ $30 per MH)

Setting up machine (@ $900 per setup hour)

Handling material (@ $3,000 per run)

Packaging building

Inspecting and packing (@ $5_per direct labor-hour)

Shipping (@ $1,320 per shipment)

Total ABC overhead

$ 180,000

36,000

24,000

$ 900,000

360,000

120,000

300,000

132,000

$ 672,000

114,000

264,000

$1,758,000

$5,118,000

Total ABC cost

$3,912,000

Number of units

100,000

39.12

40,000

127.95

Unit cost

Required:

a. Compute the amount of overhead allocated to the Sport and the Pro drones for the first quarter using activity-based costing.

Assume that all events are the same in the first quarter as in the third quarter except for the number of setup hours. Assume the cost of

a setup hour remains at $900.

Total ABC

Model

Overhead

Sport

Pro

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Excel Applications for Accounting Principles

Accounting

ISBN:

9781111581565

Author:

Gaylord N. Smith

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning