Concept explainers

Videos

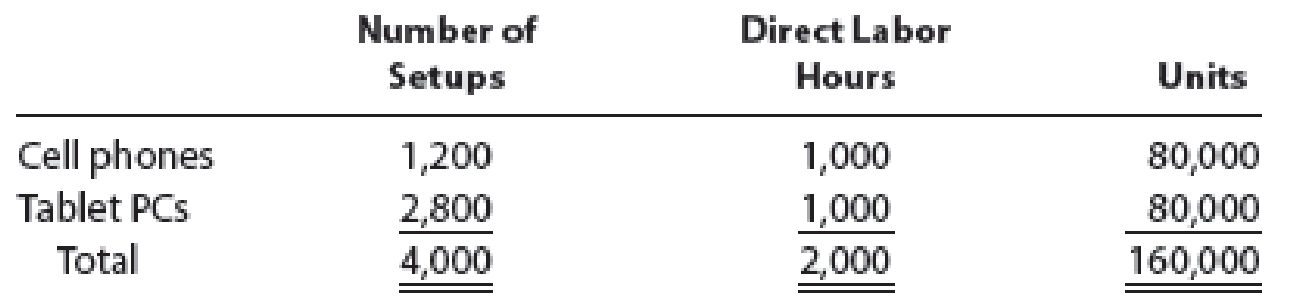

Handbrain Inc. is considering a change to activity-based product costing. The company produces two products, cell phones and tablet PCs, in a single production department. The production department is estimated to require 2,000 direct labor hours. The total indirect labor is budgeted to be $200,000.

Time records from indirect labor employees revealed that they spent 30% of their time setting up production runs and 70% of their time supporting actual production.

The following information about cell phones and tablet PCs was determined from the corporate records:

- a. Determine the indirect labor cost per unit allocated to cell phones and tablet PCs under a single plantwide factory

overhead rate system using the direct labor hours as the allocation base. - b. Determine the budgeted activity costs and activity rates for the indirect labor under activity-based costing. Assume two activities—one for setup and the other for production support.

- c. Determine the activity cost per unit for indirect labor allocated to each product under activity-based costing.

- d. Why are the per-unit allocated costs in (a) different from the per-unit activity cost assigned to the products in (c)?

a.

Compute the indirect labor cost per unit allocated to cell phones and tablet under a single plant wide factory overhead rate system.

Explanation of Solution

Single plant-wide factory overhead rate: The rate at which the factory or manufacturing overheads are allocated to products is referred to as single plant-wide factory overhead rate.

Formula to compute single plant-wide overhead rate:

Activity-based costing (ABC) method: The costing method which allocates overheads to the products based on factory overhead rate for each activity or cost object, according to the cost pooled for the cost drivers (allocation base).

Formula to compute activity-based overhead rate:

Compute the indirect labor cost per unit allocated to cell phones and tablet under a single plant wide factory overhead rate system.

| Types of Products |

Indirect labor cost (A) (2) |

Number of units (B) |

Indirect labor cost per unit |

| Cell phones | $100,000 | 80,000 | $1.25 |

| Tablets | $100,000 | 80,000 | $1.25 |

Table (1)

Working note (1):

Compute the single plant-wide overhead rate using direct labor hour (DLH) as the allocation base.

Working note (2):

Compute the total indirect labor cost for each product.

| Types of Products | Indirect labor hours | × | Single Plant-Wide Overhead Rate (1) | = | indirect labor cost |

| Cell phones | 1,000 | × | $100 per DLH | = | $100,000 |

| Tablets | 1,000 | × | $100 per DLH | = | $100,000 |

Table (2)

b.

Compute the activity-based overhead rate for each of the given activities.

Explanation of Solution

Compute the activity-based overhead rates for each activity.

| Computation of Activity-Based Overhead Rates | |||

| Activity |

Activity Cost (C) |

Total Activity-Base Usage (D) |

Activity-Based Overhead Rates |

| Setup | $60,000 (3) | 4,000 setups | $15 per setup |

| Production support |

140,000 (4) | 2,000 DLH | $70 per DLH |

Table (3)

Working note (3):

Compute the activity cost for setup activity.

Working note (3):

Compute the activity cost for production support activity.

c.

Compute the activity-cost per unit of the each product.

Explanation of Solution

Compute the activity cost allocated per unit of cell phone.

| Activity | Activity-Based Overhead Rates | × | Actual Use of Activity-Base (Cost Driver) | = | Activity Cost Allocated |

| Setup | $15 per setup | × | 1,200 setups | = | $18,000 |

| Production support | $70 per DLH | × | 1,000 DLH | = | 70,000 |

| Total activity costs allocated to cell phones (E) | $88,000 | ||||

| Number of units of cell phone (F) | 80,000 units | ||||

| Activity-based overhead cost per unit of cell phone | $1.10 | ||||

Table (4)

Note: Refer to Table (2) for the value and computation of activity allocation rates.

Compute the activity cost allocated per unit of tablet.

| Activity | Activity-Based Overhead Rates | × | Actual Use of Activity-Base (Cost Driver) | = | Activity Cost Allocated |

| Setup | $15 per setup | × | 2,800 setups | = | $42,000 |

| Production support | $70 per DLH | × | 1,000 DLH | = | 70,000 |

| Total activity costs allocated to tablets (G) | $112,00 | ||||

| Number of units of tablet (H) | 80,000 units | ||||

| Activity-based overhead cost per unit of tablet | $1.40 | ||||

Table (5)

Note: Refer to Table (2) for the value and computation of activity allocation rates.

d.

Discuss the reason why the per unit allocated costs in single plant-wide overhead rate approach is different from the per unit allocated costs in the activity based costing.

Explanation of Solution

The product cost under single plant-wide overhead rate approach and ABC approach are different. The product cost is distorted in single plant-wide overhead rate approach because the time spent for setup production for cell phones and tablets is not in the same ratio as the direct labor hours used in support production for cell phones and tablets.

Want to see more full solutions like this?

Chapter 18 Solutions

Financial And Managerial Accounting

- Douglas Davis, controller for Marston, Inc., prepared the following budget for manufacturing costs at two different levels of activity for 20X1: During 20X1, Marston worked a total of 80,000 direct labor hours, used 250,000 machine hours, made 32,000 moves, and performed 120 batch inspections. The following actual costs were incurred: Marston applies overhead using rates based on direct labor hours, machine hours, number of moves, and number of batches. The second level of activity (the right column in the preceding table) is the practical level of activity (the available activity for resources acquired in advance of usage) and is used to compute predetermined overhead pool rates. Required: 1. Prepare a performance report for Marstons manufacturing costs in the current year. 2. Assume that one of the products produced by Marston is budgeted to use 10,000 direct labor hours, 15,000 machine hours, and 500 moves and will be produced in five batches. A total of 10,000 units will be produced during the year. Calculate the budgeted unit manufacturing cost. 3. One of Marstons managers said the following: Budgeting at the activity level makes a lot of sense. It really helps us manage costs better. But the previous budget really needs to provide more detailed information. For example, I know that the moving materials activity involves the use of forklifts and operators, and this information is lost when only the total cost of the activity for various levels of output is reported. We have four forklifts, each capable of providing 10,000 moves per year. We lease these forklifts for five years, at 10,000 per year. Furthermore, for our two shifts, we need up to eight operators if we run all four forklifts. Each operator is paid a salary of 30,000 per year. Also, I know that fuel costs about 0.25 per move. Assuming that these are the only three items, expand the detail of the flexible budget for moving materials to reveal the cost of these three resource items for 20,000 moves and 40,000 moves, respectively. Based on these comments, explain how this additional information can help Marston better manage its costs. (Especially consider how activity-based budgeting may provide useful information for non-value-added activities.)arrow_forwardBrees, Inc., a manufacturer of golf carts, has just received an offer from a supplier to provide 2,600 units of a component used in its main product. The component is a track assembly that is currently produced internally. The supplier has offered to sell the track assembly for 66 per unit. Brees is currently using a traditional, unit-based costing system that assigns overhead to jobs on the basis of direct labor hours. The estimated traditional full cost of producing the track assembly is as follows: Prior to making a decision, the companys CEO commissioned a special study to see whether there would be any decrease in the fixed overhead costs. The results of the study revealed the following: 3 setups1,160 each (The setups would be avoided, and total spending could be reduced by 1,160 per setup.) One half-time inspector is needed. The company already uses part-time inspectors hired through a temporary employment agency. The yearly cost of the part-time inspectors for the track assembly operation is 12,300 and could be totally avoided if the part were purchased. Engineering work: 470 hours, 45/hour. (Although the work decreases by 470 hours, the engineer assigned to the track assembly line also spends time on other products, and there would be no reduction in his salary.) 75 fewer material moves at 30 per move. Required: 1. Ignore the special study, and determine whether the track assembly should be produced internally or purchased from the supplier. 2. Now, using the special study data, repeat the analysis. 3. Discuss the qualitative factors that would affect the decision, including strategic implications. 4. After reviewing the special study, the controller made the following remark: This study ignores the additional activity demands that purchasing would cause. For example, although the demand for inspecting the part on the production floor decreases, we may need to inspect the incoming parts in the receiving area. Will we actually save any inspection costs? Is the controller right?arrow_forwardAdam Corporation manufactures computer tables and has the following budgeted indirect manufacturing cost information for the next year: If Adam uses the step-down (sequential) method, beginning with the Maintenance Department, to allocate support department costs to production departments, the total overhead (rounded to the nearest dollar) for the Machining Department to allocate to its products would be: a. 407,500. b. 422,750. c. 442,053. d. 445,000.arrow_forward

- Firenza Company manufactures specialty tools to customer order. Budgeted overhead for the coming year is: Previously, Sanjay Bhatt, Firenza Companys controller, had applied overhead on the basis of machine hours. Expected machine hours for the coming year are 50,000. Sanjay has been reading about activity-based costing, and he wonders whether or not it might offer some advantages to his company. He decided that appropriate drivers for overhead activities are purchase orders for purchasing, number of setups for setup cost, engineering hours for engineering cost, and machine hours for other. Budgeted amounts for these drivers are 5,000 purchase orders, 500 setups, and 2,500 engineering hours. Sanjay has been asked to prepare bids for two jobs with the following information: The typical bid price includes a 40 percent markup over full manufacturing cost. Required: 1. Calculate a plantwide rate for Firenza Company based on machine hours. What is the bid price of each job using this rate? 2. Calculate activity rates for the four overhead activities. What is the bid price of each job using these rates? 3. Which bids are more accurate? Why?arrow_forwardThe controller for Muir Companys Salem plant is analyzing overhead in order to determine appropriate drivers for use in flexible budgeting. She decided to concentrate on the past 12 months since that time period was one in which there was little important change in technology, product lines, and so on. Data on overhead costs, number of machine hours, number of setups, and number of purchase orders are in the following table. Required: 1. Calculate an overhead rate based on machine hours using the total overhead cost and total machine hours. (Round the overhead rate to the nearest cent and predicted overhead to the nearest dollar.) Use this rate to predict overhead for each of the 12 months. 2. Run a regression equation using only machine hours as the independent variable. Prepare a flexible budget for overhead for the 12 months using the results of this regression equation. (Round the intercept and x-coefficient to the nearest cent and predicted overhead to the nearest dollar.) Is this flexible budget better than the budget in Requirement 1? Why or why not?arrow_forwardYoung Company is beginning operations and is considering three alternatives to allocate manufacturing overhead to individual units produced. Young can use a plantwide rate, departmental rates, or activity-based costing. Young will produce many types of products in its single plant, and not all products will be processed through all departments. In which one of the following independent situations would reported net income for the first year be the same regardless of which overhead allocation method had been selected? a. All production costs approach those costs that were budgeted. b. The sales mix does not vary from the mix that was budgeted. c. All manufacturing overhead is a fixed cost. d. All ending inventory balances are zero.arrow_forward

- Anderson Company has the following departmental manufacturing structure for one of its products: After some study, the production manager of Anderson recommended the following revised cellular manufacturing approach: Required: 1. Calculate the total time it takes to produce a batch of 20 units using Andersons traditional departmental structure. 2. Using cellular manufacturing, how much time is saved producing the same batch of 20 units? Assuming the cell operates continuously, what is the production rate? Which process controls this production rate? 3. What if the processing times of molding, welding, and assembly are all reduced to six minutes each? What is the production rate now, and how long will it take to produce a batch of 20 units?arrow_forwardKelly Gray, production manager, was upset with the latest performance report, which indicated that she was 100,000 over budget. Given the efforts that she and her workers had made, she was confident that they had met or beat the budget. Now, she was not only upset but also genuinely puzzled over the results. Three itemsdirect labor, power, and setupswere over budget. The actual costs for these three items follow: Kelly knew that her operation had produced more units than originally had been budgeted, so more power and labor had naturally been used. She also knew that the uncertainty in scheduling had led to more setups than planned. When she pointed this out to John Huang, the controller, he assured her that the budgeted costs had been adjusted for the increase in productive activity. Curious, Kelly questioned John about the methods used to make the adjustment. JOHN: If the actual level of activity differs from the original planned level, we adjust the budget by using budget formulasformulas that allow us to predict what the costs will be for different levels of activity. KELLY: The approach sounds reasonable. However, Im sure something is wrong here. Tell me exactly how you adjusted the costs of labor, power, and setups. JOHN: First, we obtain formulas for the individual items in the budget by using the method of least squares. We assume that cost variations can be explained by variations in productive activity where activity is measured by direct labor hours. Here is a list of the cost formulas for the three items you mentioned. The variable X is the number of direct labor hours: Labor cost = 10X Power cost = 5,000 + 4X Setup cost = 100,000 KELLY: I think I see the problem. Power costs dont have a lot to do with direct labor hours. They have more to do with machine hours. As production increases, machine hours increase more rapidly than direct labor hours. Also, ... JOHN: You know, you have a point. The coefficient of determination for power cost is only about 50 percent. That leaves a lot of unexplained cost variation. The coefficient for labor, however, is much betterit explains about 96 percent of the cost variation. Setup costs, of course, are fixed. KELLY: Well, as I was about to say, setup costs also have very little to do with direct labor hours. And I might add that they certainly are not fixedat least not all of them. We had to do more setups than our original plan called for because of the scheduling changes. And we have to pay our people when they work extra hours. It seems as if we are always paying overtime. I wonder if we simply do not have enough people for the setup activity. Supplies are used for each setup, and these are not cheap. Did you build these extra costs of increased setup activity into your budget? JOHN: No, we assumed that setup costs were fixed. I see now that some of them could vary as the number of setups increases. Kelly, let me see if I can develop some cost formulas based on better explanatory variables. Ill get back with you in a few days. Assume that after a few days work, John developed the following cost formulas, all with a coefficient of determination greater than 90 percent: Labor cost = 10X; where X = Direct labor hours Power cost = 68,000 + 0.9Y; where Y = Machine hours Setup cost = 98,000 + 400Z; where Z = Number of setups The actual measures of each of the activity drivers are as follows: Required: 1. Prepare a performance report for direct labor, power, and setups using the direct-labor-based formulas. 2. Prepare a performance report for direct labor, power, and setups using the multiple cost driver formulas that John developed. 3. Of the two approaches, which provides the most accurate picture of Kellys performance? Why? 4. After reviewing the approach to performance measurement, a consultant remarked that non-value-added cost trend reports would be a much better performance measurement approach than comparing actual costs with budgeted costseven if activity flexible budgets were used. Do you agree or disagree? Explain.arrow_forwardPinter Company had the following environmental activities and product information: 1. Environmental activity costs 2. Driver data 3. Other production data Required: 1. Calculate the activity rates that will be used to assign environmental costs to products. 2. Determine the unit environmental and unit costs of each product using ABC. 3. What if the design costs increased to 360,000 and the cost of toxic waste decreased to 750,000? Assume that Solvent Y uses 6,000 out of 12,000 design hours. Also assume that waste is cut by 50 percent and that Solvent Y is responsible for 14,250 of 15,000 pounds of toxic waste. What is the new environmental cost for Solvent Y?arrow_forward

- Flaherty, Inc., has just completed its first year of operations. The unit costs on a normal costing basis are as follows: During the year, the company had the following activity: Actual fixed overhead was 12,000 less than budgeted fixed overhead. Budgeted variable overhead was 5,000 less than the actual variable overhead. The company used an expected actual activity level of 12,000 direct labor hours to compute the predetermined overhead rates. Any overhead variances are closed to Cost of Goods Sold. Required: 1. Compute the unit cost using (a) absorption costing and (b) variable costing. 2. Prepare an absorption-costing income statement. 3. Prepare a variable-costing income statement. 4. Reconcile the difference between the two income statements.arrow_forwardSalley is developing material and labor standards for her company. She finds that it costs $0.55 per pound of material per widget. Each widget requires 6 pounds of material per widget. Salley is also working with the operations manager to determine what the standard labor cost is for a widget. Upon observation, Salley notes that it takes 3 hours in the assembly department and 1 hour in the finishing department to complete one widget. All employees are paid $10.50 per hour. A. What is the standard materials cost per unit for a widget? 8. What is the standard labor cost per unit for a widget?arrow_forwardMott Company recently implemented a JIT manufacturing system. After one year of operation, Heidi Burrows, president of the company, wanted to compare product cost under the JIT system with product cost under the old system. Motts two products are weed eaters and lawn edgers. The unit prime costs under the old system are as follows: Under the old manufacturing system, the company operated three service centers and two production departments. Overhead was applied using departmental overhead rates. The direct overhead costs associated with each department for the year preceding the installation of JIT are as follows: Under the old system, the overhead costs of the service departments were allocated directly to the producing departments and then to the products passing through them. (Both products passed through each producing department.) The overhead rate for the Machining Department was based on machine hours, and the overhead rate for assembly was based on direct labor hours. During the last year of operations for the old system, the Machining Department used 80,000 machine hours, and the Assembly Department used 20,000 direct labor hours. Each weed eater required 1.0 machine hour in Machining and 0.25 direct labor hour in Assembly. Each lawn edger required 2.0 machine hours in Machining and 0.5 hour in Assembly. Bases for allocation of the service costs are as follows: Upon implementing JIT, a manufacturing cell for each product was created to replace the departmental structure. Each cell occupied 40,000 square feet. Maintenance and materials handling were both decentralized to the cell level. Essentially, cell workers were trained to operate the machines in each cell, assemble the components, maintain the machines, and move the partially completed units from one point to the next within the cell. During the first year of the JIT system, the company produced and sold 20,000 weed eaters and 30,000 lawn edgers. This output was identical to that for the last year of operations under the old system. The following costs have been assigned to the manufacturing cells: Required: 1. Compute the unit cost for each product under the old manufacturing system. 2. Compute the unit cost for each product under the JIT system. 3. Which of the unit costs is more accurate? Explain. Include in your explanation a discussion of how the computational approaches differ. 4. Calculate the decrease in overhead costs under JIT, and provide some possible reasons that explain the decrease.arrow_forward

- Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning  Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning