Trend Report, Non-Value-Added Costs Sanford, Inc., has developed value-added standards for four activities: purchasing parts, receiving parts, moving parts, and setting up equipment. The activities, the activity drivers, the standard and actual quantities, as the price standards for 20x1 are as follows: Activities Activity Driver SQ AQ SP Purchasing parts Purchase orders 2,600 3,640 $300 Receiving parts Receiving orders 5,200 7,800 195 Moving parts Number of moves 2,600 390 Setting up equipment Setup hours O 10,400 117 The actual prices paid per unit of each activity driver were equal to the standard prices. Suppose that for 20x2, Sanford, Inc., has chosen suppliers that provide higher-quality parts and redesigned its plant layout to reduce material movement. Additionally, Sanford implemented a new setup procedure and provided training for its purchasing agents. As a consequence, less setup time is required and fewer purchasing mistakes are made. At the end of 20x2, the following information is provided. Activities Activity Driver SQ AQ SP Purchasing parts Purchase orders 2,600 3,120 $300 Receiving parts Receiving orders 5,200 6,500 195 Moving parts Number of moves 840 395 Setting up equipment Setup hours O 2,600 117 Required: Prepare a report that compares the non-value-added costs for 20x2 with those of 20x1. Enter all your answers as positive amounts. Sanford, Inc. Non-Value-Added Cost Trend Report For the Year Ended December 31, 20x2 20x1 20x2 Change Purchasing parts 780,000 x $ Receiving parts 1,014,000 X Moving parts Setting up equipment Total * 1,794,000 x

Trend Report, Non-Value-Added Costs Sanford, Inc., has developed value-added standards for four activities: purchasing parts, receiving parts, moving parts, and setting up equipment. The activities, the activity drivers, the standard and actual quantities, as the price standards for 20x1 are as follows: Activities Activity Driver SQ AQ SP Purchasing parts Purchase orders 2,600 3,640 $300 Receiving parts Receiving orders 5,200 7,800 195 Moving parts Number of moves 2,600 390 Setting up equipment Setup hours O 10,400 117 The actual prices paid per unit of each activity driver were equal to the standard prices. Suppose that for 20x2, Sanford, Inc., has chosen suppliers that provide higher-quality parts and redesigned its plant layout to reduce material movement. Additionally, Sanford implemented a new setup procedure and provided training for its purchasing agents. As a consequence, less setup time is required and fewer purchasing mistakes are made. At the end of 20x2, the following information is provided. Activities Activity Driver SQ AQ SP Purchasing parts Purchase orders 2,600 3,120 $300 Receiving parts Receiving orders 5,200 6,500 195 Moving parts Number of moves 840 395 Setting up equipment Setup hours O 2,600 117 Required: Prepare a report that compares the non-value-added costs for 20x2 with those of 20x1. Enter all your answers as positive amounts. Sanford, Inc. Non-Value-Added Cost Trend Report For the Year Ended December 31, 20x2 20x1 20x2 Change Purchasing parts 780,000 x $ Receiving parts 1,014,000 X Moving parts Setting up equipment Total * 1,794,000 x

Cornerstones of Cost Management (Cornerstones Series)

4th Edition

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Don R. Hansen, Maryanne M. Mowen

Chapter12: Activity-based Management

Section: Chapter Questions

Problem 14E: Sanford, Inc., has developed value-added standards for four activities: purchasing parts, receiving...

Related questions

Question

100%

Please give answers clearly. thank you.

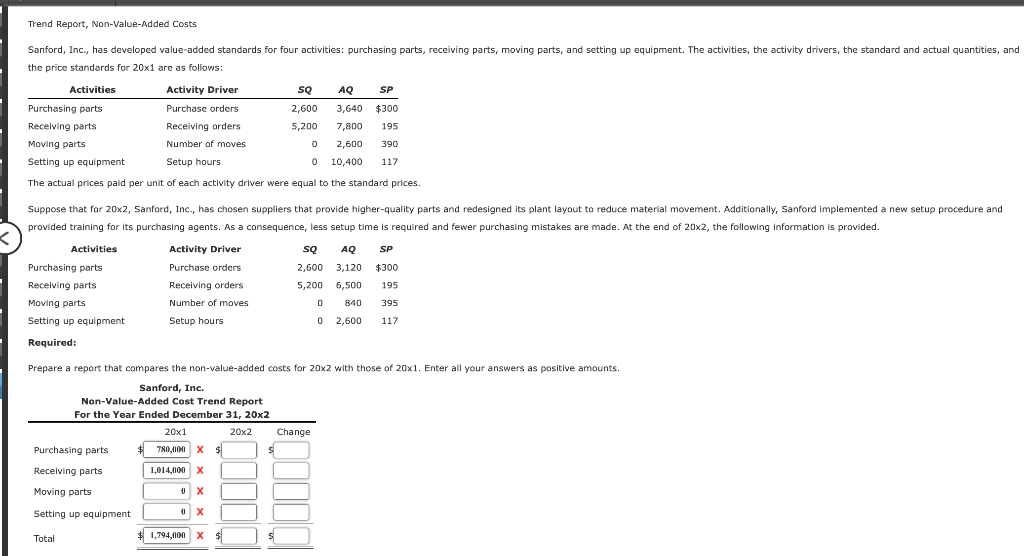

Transcribed Image Text:Trend Report, Non-Value-Added Costs

Sanford, Inc., has developed value-added standards for four activities: purchasing parts, receiving parts, moving parts, and setting up equipment. The activities, the activity drivers, the standard and actual quantities, and

the price standards for 20x1 are as follows:

Activities

Activity Driver

SQ

AQ

SP

Purchasing parts

Purchase orders

2,600

3,640

$300

Receiving parts

Receiving orders

5,200

7,800

195

Moving parts

Number of moves

2,600

390

Setting up equipment

Setup hours

10,400

117

The actual prices paid per unit of each activity driver were equal to the standard prices.

Suppose that for 20x2, Sanford, Inc., has chosen suppliers that provide higher-quality parts and redesigned its plant layout to reduce material movement. Additionally, Sanford implemented a new setup procedure and

provided training for its purchasing agents. As a consequence, less setup time is required and fewer purchasing mistakes are made. At the end of 20x2, the following information is provided.

Activities

Activity Driver

sQ

AQ

SP

Purchasing parts

Purchase orders

2,600 3,120

$300

Receiving parts

Receiving orders

5,200 6,500

195

Moving parts

Number of moves

840

395

Setting up equipment

Setup hours

2,600

117

Required:

Prepare a report that compares the non-value-added costs for 20x2 with those of 20x1. Enter all your answers as positive amounts.

Sanford, Inc.

Non-Value-Added Cost Trend Report

For the Year Ended December 31, 20x2

20x1

20x2

Change

Purchasing parts

780,000 x $

Receiving parts

1,014,000 X

Moving parts

Setting up equipment

$1,794,000

x

Total

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning