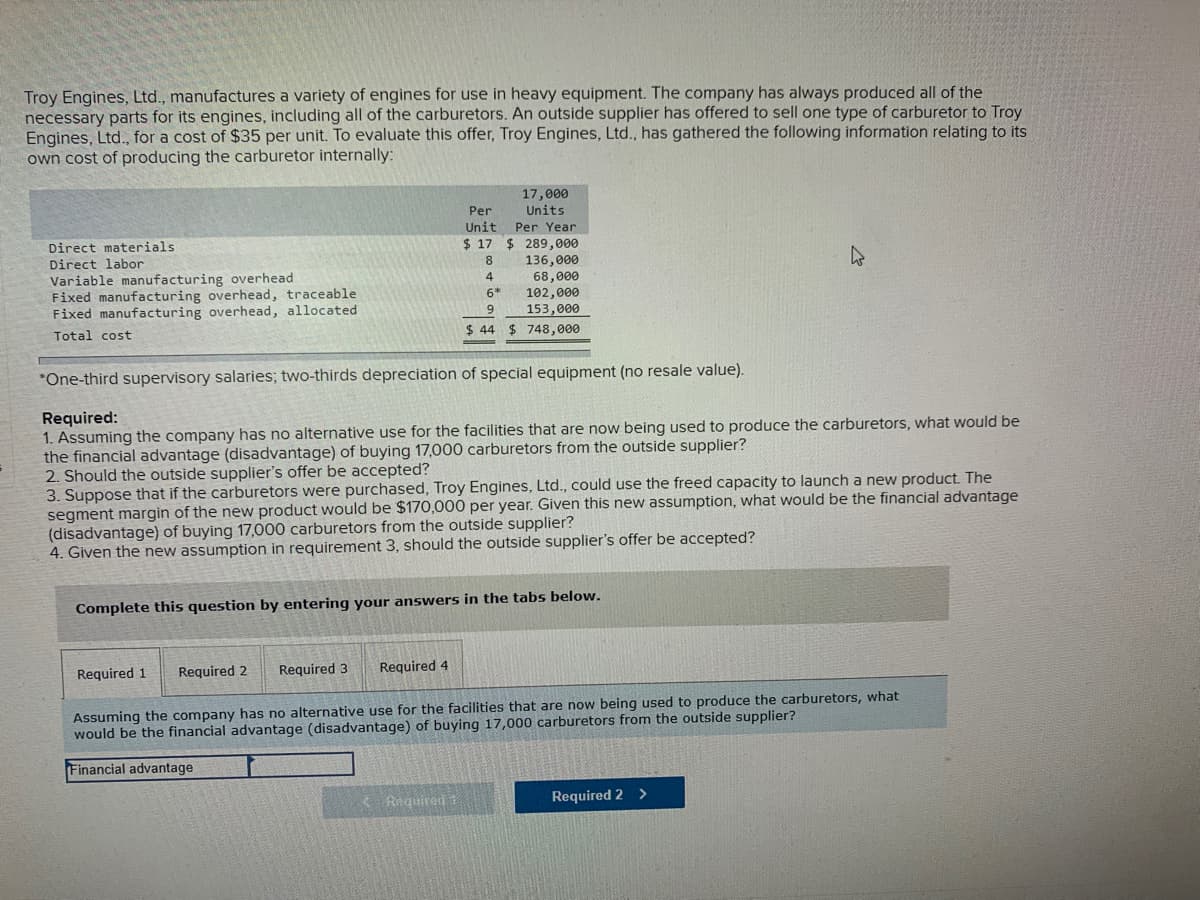

Troy Engines, Ltd., manufactures a variety of engines for use in heavy equipment. The company has always produced all of the necessary parts for its engines, including all of the carburetors. An outside supplier has offered to sell one type of carburetor to Troy Engines, Ltd., for a cost of $35 per unit. To evaluate this offer, Troy Engines, Ltd., has gathered the following information relating to its own cost of producing the carburetor internally: 17,000 Units Unit Per Year $ 17 $ 289,000 Per Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead, traceable Fixed manufacturing overhead, allocated 8 136,000 68,000 102,000 153,000 $ 44 $ 748,000 4 6* 9 Total cost

Troy Engines, Ltd., manufactures a variety of engines for use in heavy equipment. The company has always produced all of the necessary parts for its engines, including all of the carburetors. An outside supplier has offered to sell one type of carburetor to Troy Engines, Ltd., for a cost of $35 per unit. To evaluate this offer, Troy Engines, Ltd., has gathered the following information relating to its own cost of producing the carburetor internally: 17,000 Units Unit Per Year $ 17 $ 289,000 Per Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead, traceable Fixed manufacturing overhead, allocated 8 136,000 68,000 102,000 153,000 $ 44 $ 748,000 4 6* 9 Total cost

Chapter10: Short-term Decision Making

Section: Chapter Questions

Problem 7EB: Oat Treats manufactures various types of cereal bars featuring oats. Simmons Cereal Company has...

Related questions

Question

Answer 1 and 3

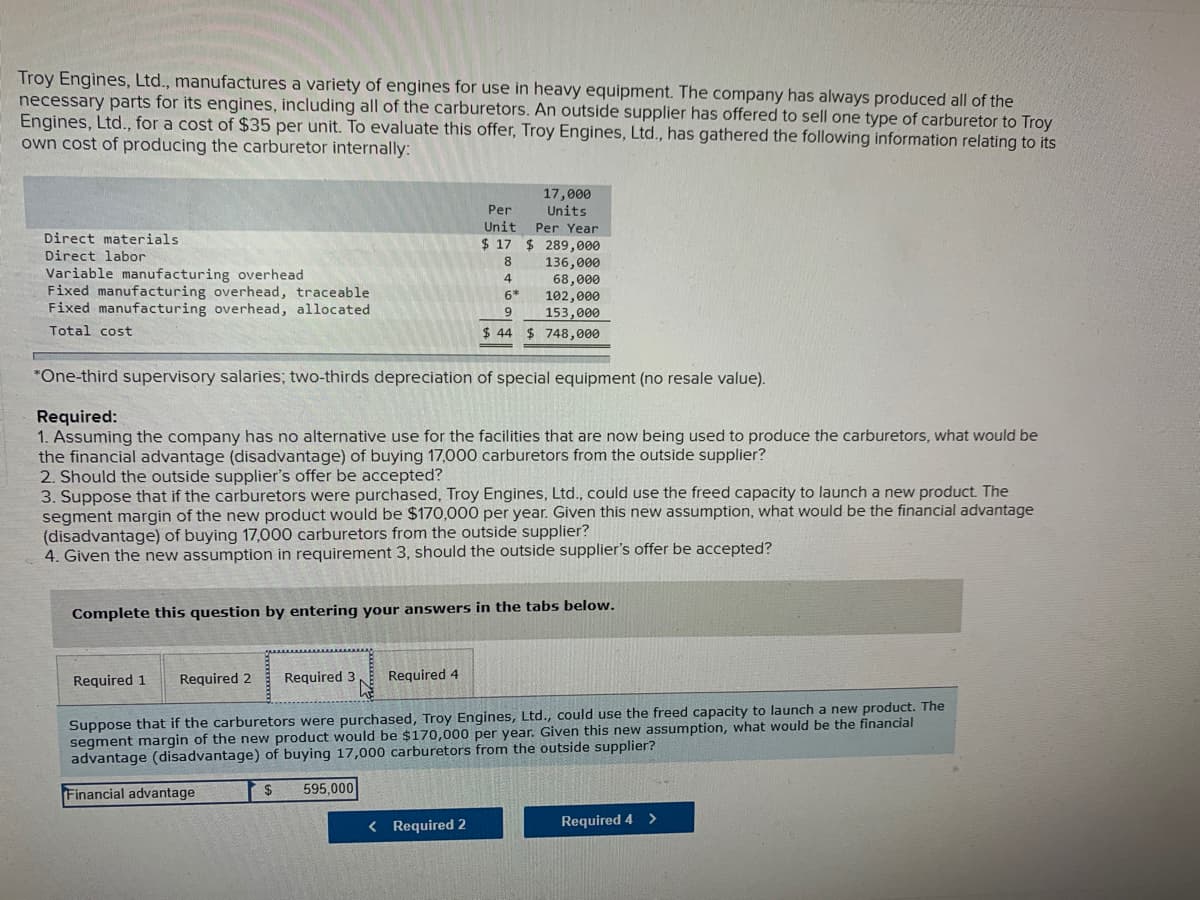

Transcribed Image Text:Troy Engines, Ltd., manufactures a variety of engines for use in heavy equipment. The company has always produced all of the

necessary parts for its engines, including all of the carburetors. An outside supplier has offered to sell one type of carburetor to Troy

Engines, Ltd., for a cost of $35 per unit. To evaluate this offer, Troy Engines, Ltd., has gathered the following information relating to its

own cost of producing the carburetor internally:

17,000

Units

Unit Per Year

$ 17 $ 289,000

Per

Direct materials

Direct labor

Variable manufacturing overhead

Fixed manufacturing overhead, traceable

Fixed manufacturing overhead, allocated

8.

136,000

68,000

102,000

153,000

4

6*

9.

Total cost

$ 44 $ 748,000

*One-third supervisory salaries; two-thirds depreciation of special equipment (no resale value).

Required:

1. Assuming the company has no alternative use for the facilities that are now being used to produce the carburetors, what would be

the financial advantage (disadvantage) of buying 17,000 carburetors from the outside supplier?

2. Should the outside supplier's offer be accepted?

3. Suppose that if the carburetors were purchased, Troy Engines, Ltd., could use the freed capacity to launch a new product. The

segment margin of the new product would be $170,000 per year. Given this new assumption, what would be the financial advantage

(disadvantage) of buying 17,000 carburetors from the outside supplier?

4. Given the new assumption in requirement 3, should the outside supplier's offer be accepted?

Complete this question by entering your answers in the tabs below.

Required 1

Required 2

Required 3

Required 4

Suppose that if the carburetors were purchased, Troy Engines, Ltd., could use the freed capacity to launch a new product. The

segment margin of the new product would be $170,000 per year. Given this new assumption, what would be the financial

advantage (disadvantage) of buying 17,000 carburetors from the outside supplier?

Financial advantage

$4

595,000

< Required 2

Required 4

<>

Transcribed Image Text:Troy Engines, Ltd., manufactures a variety of engines for use in heavy equipment. The company has always produced all of the

necessary parts for its engines, including all of the carburetors. An outside supplier has offered to sell one type of carburetor to Troy

Engines, Ltd., for a cost of $35 per unit. To evaluate this offer, Troy Engines, Ltd., has gathered the following information relating to its

own cost of producing the carburetor internally:

17,000

Units

Per Year

Per

Unit

$ 17 $ 289,000

136,000

68,000

102,000

153,000

Direct materials

Direct labor

8.

Variable manufacturing overhead

Fixed manufacturing overhead, traceable

Fixed manufacturing overhead, allocated

6*

$ 44 $ 748,000

Total cost

*One-third supervisory salaries; two-thirds depreciation of special equipment (no resale value).

Required:

1. Assuming the company has no alternative use for the facilities that are now being used to produce the carburetors, what would be

the financial advantage (disadvantage) of buying 17,000 carburetors from the outside supplier?

2. Should the outside supplier's offer be accepted?

3. Suppose that if the carburetors were purchased, Troy Engines, Ltd., could use the freed capacity to launch a new product. The

segment margin of the new product would be $170,000 per year. Given this new assumption, what would be the financial advantage

(disadvantage) of buying 17,000 carburetors from the outside supplier?

4. Given the new assumption in requirement 3, should the outside supplier's offer be accepted?

Complete this question by entering your answers in the tabs below.

Required 2

Required 3

Required 4

Required 1

Assuming the company has no alternative use for the facilities that are now being used to produce the carburetors, what

would be the financial advantage (disadvantage) of buying 17,000 carburetors from the outside supplier?

Financial advantage

< Required t

Required 2 >

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning