The SP Corporation makes 32,000 motors to be used in the production of ts sewing machines. The average cost per motor at this level of activity is: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead $9.10 $8.10 $3.25 $4.20 An outside supplier recently began producing a comparable motor that could be used in the sewing machine. The price offered to SP Corporation for this motor is $2275. If SP Corporation decides not to make the motors, there would be no other use for the production facilities and none of the fixed manufacturing overhead cost could avoided. Direct iabor is a variable cost in this company. The annual financial advantage (disadvantage) for the company as a result of making the motors rather than buying them from the outside suppler would be: Multiple Choice

The SP Corporation makes 32,000 motors to be used in the production of ts sewing machines. The average cost per motor at this level of activity is: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead $9.10 $8.10 $3.25 $4.20 An outside supplier recently began producing a comparable motor that could be used in the sewing machine. The price offered to SP Corporation for this motor is $2275. If SP Corporation decides not to make the motors, there would be no other use for the production facilities and none of the fixed manufacturing overhead cost could avoided. Direct iabor is a variable cost in this company. The annual financial advantage (disadvantage) for the company as a result of making the motors rather than buying them from the outside suppler would be: Multiple Choice

Chapter10: Short-term Decision Making

Section: Chapter Questions

Problem 7EB: Oat Treats manufactures various types of cereal bars featuring oats. Simmons Cereal Company has...

Related questions

Question

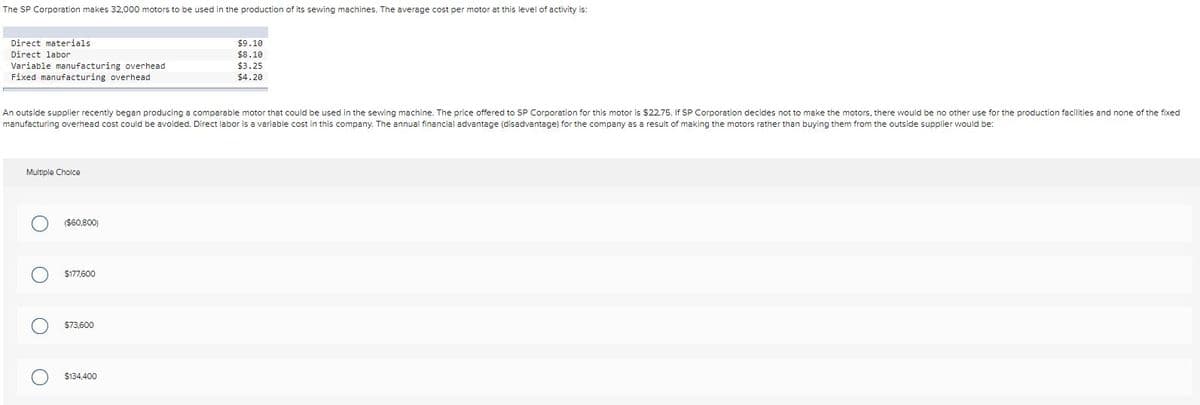

Transcribed Image Text:The SP Corporation makes 32,000 motors to be used in the production of its sewing machines. The average cost per motor at this level of activity is:

Direct materials

$9.10

$8.10

$3.25

$4.20

Direct labor

Variable manufacturing overhead

Fixed manufacturing overhead

An outside supplier recently began producing a comparable motor that could be used in the sewing machine. The price offered to SP Corporation for this motor is $22.75. If SP Corporation decides not to make the motors, there would be no other use for the production facilities and none of the fixed

manufacturing overhead cost could be avoided. Direct labor is a variable cost in this company. The annual financial advantage (disadvantage) for the company as a result of making the motors rather than buying them from the outside supplier would be:

Multiple Cholce

($60,800)

$177,600

$73,600

$134,400

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,